In 2019, the highest rates of government guarantees in the EU were recorded in Finland

The most common form of contingent liabilities in the EU Member States is government guarantees on liabilities and occasionally on assets of third parties.

The highest rate of government guarantees was recorded in Finland (33.4% of GDP), ahead of Denmark (18.2%), Austria (16.1%), Germany (13.2%) and France (11.6%). Data in Finland include as well guarantees provided by a specialised financial public corporation classified outside of government. The lowest shares (close to 0%) were observed in Ireland and Slovakia. Rates of less than 1% of GDP were also recorded in Bulgaria, Czechia and Lithuania.

In most EU Member States, the central government is the predominant guarantor. A high level of local government guarantees can also be seen in Finland, Denmark, France and Sweden. In several countries - Belgium, Spain, France, Cyprus, Luxembourg, Portugal and Finland - a major part of the guarantees is towards financial institutions, often granted in the context of the 2008-2009 financial crisis.

Slovakia and Portugal with largest liabilities related to off-balance PPPs

In all EU Member States, liabilities related to off-balance public-private partnerships (PPPs, long-term construction contracts where assets are recorded outside government accounts) were below 2.5% of GDP in 2019. Slovakia had the highest share (2.4% of GDP), followed by Portugal (2.3%) and Hungary (1.1%). In both Slovakia and Portugal, the liabilities relate mainly to motorway projects.

In many EU Member States, off-balance PPPs were observed at the central government level, whereas in Spain, Belgium and Austria they were notably related also to state and local governments.

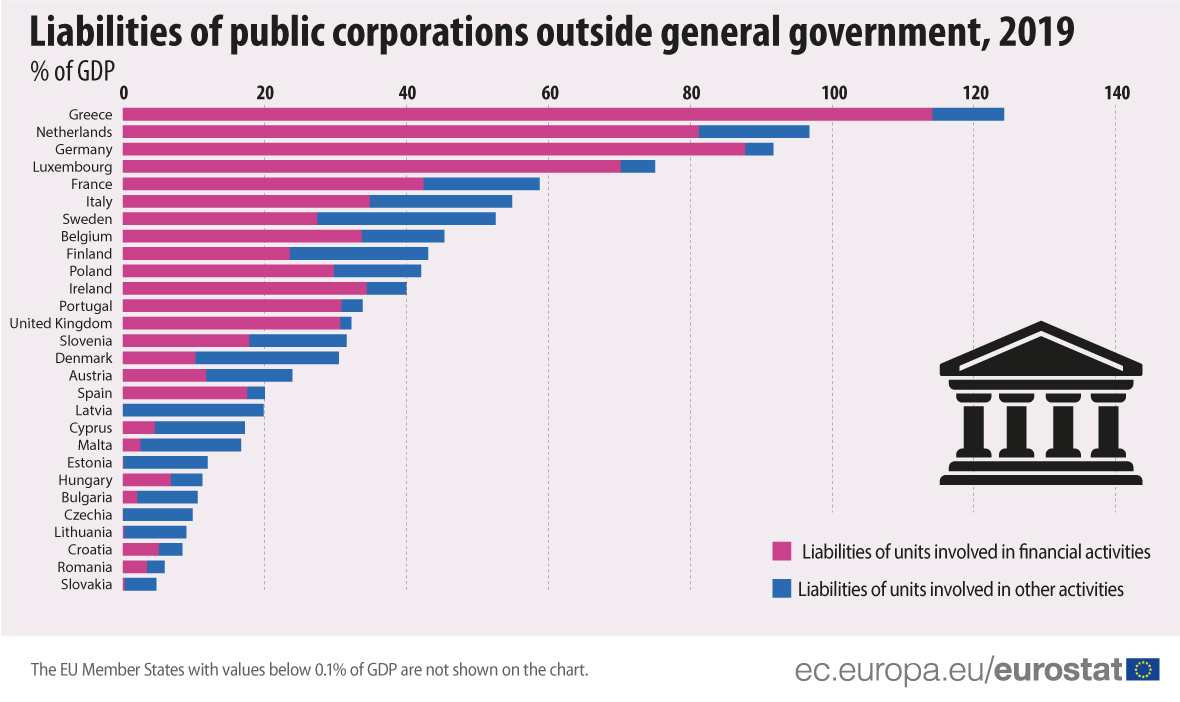

Liabilities of public corporations the highest in Greece

The level of liabilities of public corporations classified outside general government in 2019 differs widely in the EU Member States. Significant amounts of liabilities were recorded in Greece (124.3% of GDP), ahead of the Netherlands (96.8%), Germany (91.7%), Luxembourg (75.1%) and France (58.7%).

In contrast, small amounts of public corporation liabilities were recorded in Slovakia (4.7%) followed by Romania (5.9%), Croatia (8.4%), Lithuania (8.9%) and Czechia (9.8%).

The main reason for the high level of these liabilities in certain Member States is that the data include government controlled financial institutions, in particular public banks. Most of these liabilities consist of deposits held in the public banks by households or by other kinds of private or public entities. In general, financial institutions report high amounts of debt liabilities and have, at the same time, significant level of assets, which are not captured in this data collection.

Cyprus remained the country with the highest level of non-performing loans

In 2019, Cyprus remained the country with the highest stock of non-performing loans (assets) of general government, at 28.8% of GDP, a far larger share compared with the other EU Member States, despite a year-on-year decrease of more than 3 percentage points. This was due to a large transaction in 2018, whereby non-performing loans from a Cypriot public financial corporation (classified outside government) were transferred to a government unit.

Three other EU Member States recorded a share higher than 1% of GDP: Slovenia (2.5%), Portugal (1.4%) and Croatia (1.2%). For Cyprus, Slovenia and Portugal, the majority of non-performing loans refer to loans of public financial defeasance structures. In the case of Croatia, the figure mainly refers to the loans of a national development bank (also classified inside general government). Data on non-performing loans are not yet available for France.

This article includes data on government guarantees, liabilities related to public-private partnerships (PPPs) recorded off-government-balance-sheet and liabilities of government-controlled entities (public corporations) classified outside general government. Contingent liabilities are only potential liabilities. They may become actual government liabilities if specific conditions prevail. Similarly, the publication also includes data on government non-performing loans (NPLs, assets), which could imply a loss for government if these loans were not repaid. These data add further transparency to the public finances in the European Union by providing a more comprehensive picture of potential impacts on Member States’ financial positions.

The majority of the data in this release refer to 31 December 2019. These data therefore do not include any COVID-19 related guarantees or other contingent liabilities, as these were enacted only after March 2020. According to the Decision of Eurostat from 2013, contingent liability data are reported by the European Union (EU) Member States annually each December, with a typical time lag of T+12 months.

For more information, you can read the Statistics Explained article on Contingent liabilities and non-performing loans.

Source datasets: gov_cl_guar (government guarantees), gov_cl_ppp (liabilities related to off-balance PPPs), gov_cl_liab (liabilities of public corporations outside general government) and gov_cl_npl (non-performing loans).

Detailed breakdowns and time series for years prior to 2019 are available in Eurostat database as well as the related metadata and country specific footnotes.

Notes

- Data on contingent liabilities and potential obligations of government are provided by the EU Member States in the context of the Enhanced Economic Governance package (the "six-pack") adopted in 2011. In particular, Council Directive 2011/85 on requirements for budgetary frameworks of the Member States requires the Member States to publish relevant information on contingent liabilities with potentially large impacts on public budgets, including government guarantees, non-performing loans, and liabilities stemming from the operation of public corporations, including the extent thereof.

- Contingent liabilities are not part of the general government (Maastricht) debt, as defined in the Council Regulation (EC) No 479/2009 of 25 May 2009 on the application of the Protocol on the excessive deficit procedure annexed to the Treaty establishing the European Community.

To contact us, please visit our User Support page.

For press queries, please contact our Media Support.