Methodology

Euro area accounts link financial and non-financial statistics, allowing for an integrated analysis of non-financial economic activities, such as gross fixed capital formation, and financial transactions, such as the issuance of debt.

The euro area accounts also include consistent financial balance sheets. This means that quarterly changes in the financial wealth of each euro area sector can be integrated into business cycle analysis.

The institutional sectors combine institutional units that broadly have similar characteristics and behaviour. They include households and non-profit institutions serving households (NPISHs), non-financial corporations, financial corporations, and the government. Transactions with non-residents and the financial claims of residents on non-residents, or vice versa, are recorded in the 'rest of the world' account.

The households sector comprises all households and includes household firms. These cover sole proprietorships and most partnerships that do not have an independent legal status. Therefore, in addition to consumption, the sector also generates output and entrepreneurial income. In the European accounts, non-profit institutions serving households (NPISHs), such as charities and trade unions, are grouped with households. Their economic weight is relatively.

The non-financial corporations sector comprises all private and public corporate enterprises that produce goods or provide non-financial services to the market.

The government sector excludes public enterprises and comprises central, state (regional) and local government, and social security funds.

The financial corporations sector comprises all private and public entities engaged in financial intermediation, such as monetary financial institutions (broadly equivalent to banks), investment funds, insurance corporations, and pension funds. It is further subdivided to monetary financial institutions, non-MMF investment funds, other financial intermediaries, insurance corporations and pension funds.

The rest of the world is also included in sector accounts. It consists of non-resident units insofar as they are engaged in transactions with resident institutional units, or have other economic links with resident units. The rest of the world is not an institutional sector per se, for which complete sets of accounts have to be kept, but it is convenient to treat the rest of the world as a sector.

The comparison between annual and quarterly financial sector accounts is not straightforward. This is due to the way in which they are compiled:

- annual financial sector accounts are compiled based on the European system of accounts (ESA 2010)

- quarterly financial sector accounts are compiled based on guidelines for the Monetary union financial accounts (MUFA).

Their requirements differ, for example with regard to the coverage of series and the starting periods. There is constant effort to align the annual and quarterly data, but this is not always achieved in practice.

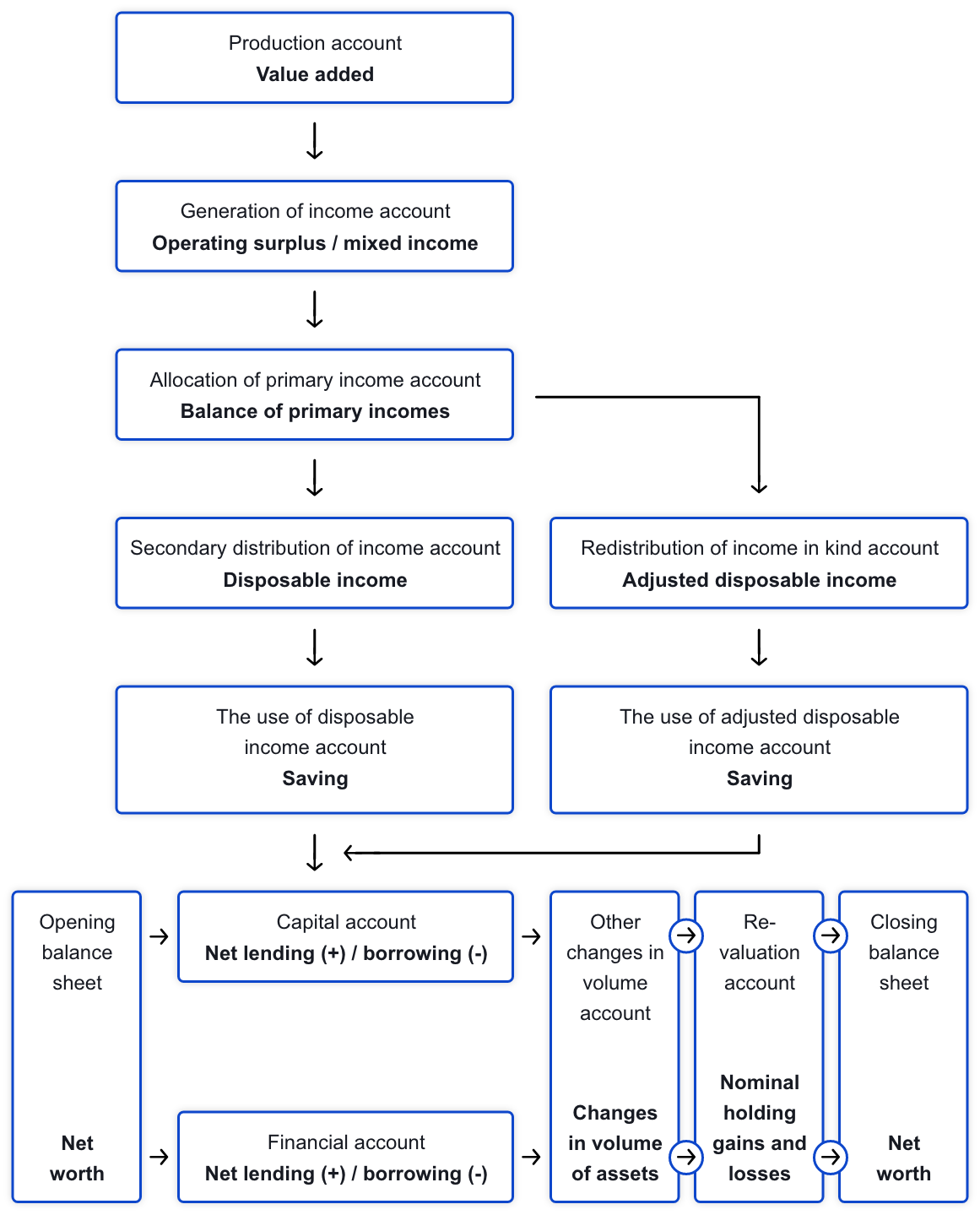

European sector accounts record, in principle, every transaction between economic subjects during a given period and show the opening and closing stocks of financial assets and liabilities in financial balance sheets. The transactions are grouped into various categories, each with a distinct economic meaning. For example, ‘compensation of employees’, which comprises wages and salaries before taxes and social contributions are deducted, and social contributions paid by the employers.

In turn, these categories of transactions are shown in a sequence of accounts, each of which covers a specific economic process. This ranges from production, income generation and income distribution (or redistribution), using income for consumption and saving and investment (as shown in the capital account) to financial transactions, such as borrowing and lending.

Each non-financial transaction is recorded as an increase in the ‘resources’ of a certain sector and an increase in the ‘uses’ of another sector. For instance, the resources side of the ‘interest’ transaction category records the amounts of interest receivable by the different sectors of the economy, whereas the uses side shows interest payable.

For each type of transaction, the total resources of all sectors and the ‘rest of the world’ equal total uses. Each account leads to a meaningful balancing item, the value of which equals total resources minus total uses. Typically, such balancing items as GDP or net saving are important economic indicators. They are carried over to the next account.

Current accounts, accumulation accounts, and balance sheets

Transactions are classified in 2 categories of accounts: current accounts and accumulation accounts.

- Current accounts record transactions that do not involve the purchase or sale of financial or non-financial assets. The final balancing item of this set of accounts is saving. This refers to the part of disposable income that is not spent for consumption purposes, but used – besides any capital transfers – to buy assets or reduce liabilities;

- Accumulation accounts that show transactions – the capital and financial accounts – record the net acquisition of non-financial and financial assets and the net incurrence of liabilities. The remaining accumulation accounts show other changes in balance sheets, such as revaluations and write-offs of bad debts. Thus, the accumulation accounts explain all the changes in the non-financial and financial balance sheets.

- Balance sheets record the value of assets and liabilities at a particular point in time.

Further reading

- Manual on sources and methods for the compilation of ESA95 financial accounts

- Report on developing a common approach to improve vertical consistency

- Vertical reconciliation - Summary table of statistical practice

- Information note on self-employment

- Guideline of the European Central Bank on the statistical reporting requirements