Structure

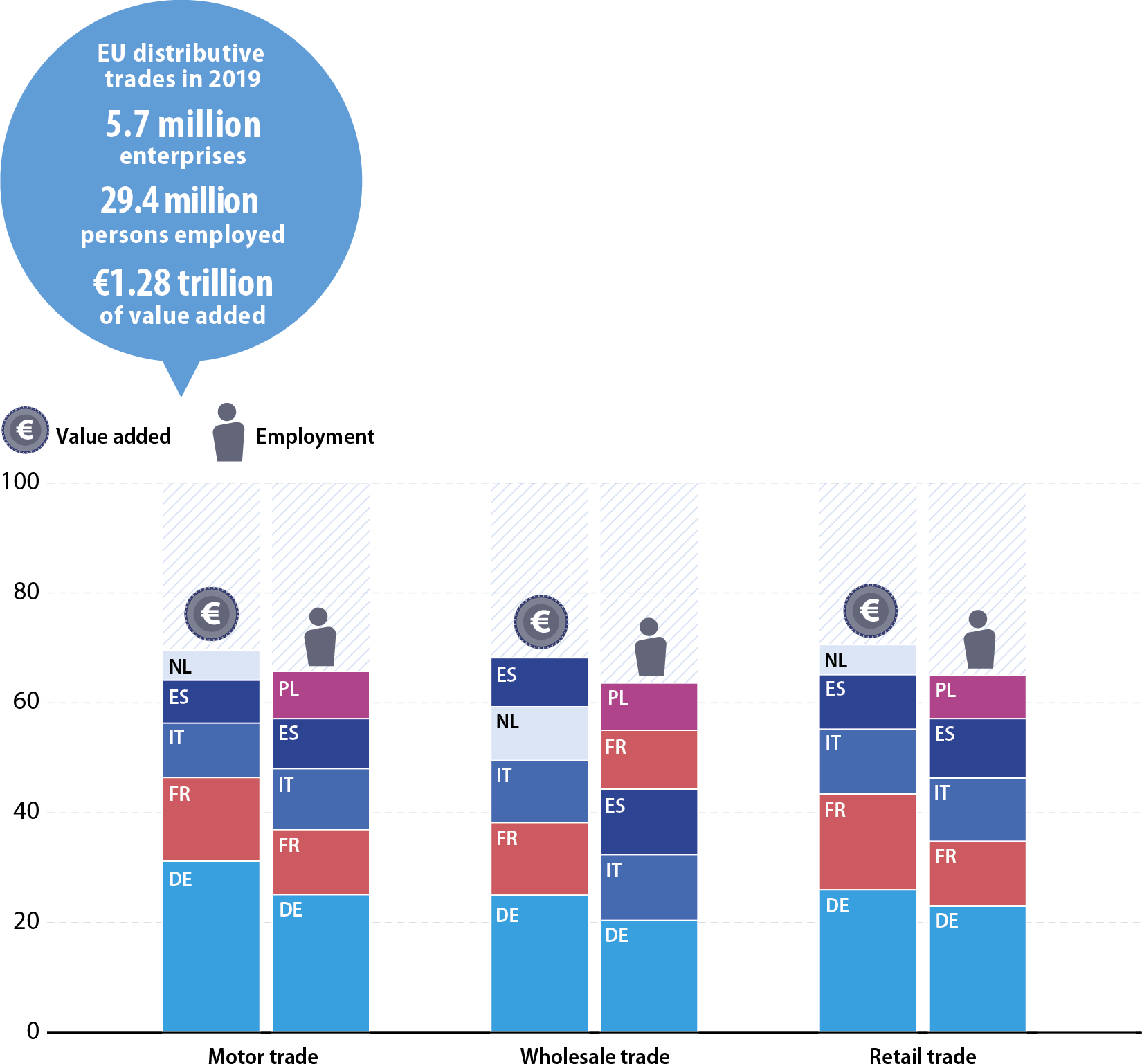

Distributive trades cover motor, wholesale and retail trades. Wholesale trade was the largest of these three divisions in value added terms, with 49.7 % of the distributive trades total in 2019 compared with 38.1 % for retail trade. In employment terms, the situation was reversed, with retail trade contributing 55.3 % compared with 32.6 % for wholesale trade.

Source: Eurostat (online data code: sbs_na_dt_r2)

Germany had the largest share of EU value added in all three distributive trades divisions in 2019, followed by France and Italy. For motor trade and for retail trade, Spain had the fourth largest share followed by the Netherlands, while this order was reversed for wholesale trade. In employment terms, the main difference was that Poland was the fifth largest EU Member State (whereas the Netherlands was not in the top five). In addition, the ranking was somewhat different for wholesale trade, as France’s level of employment in this activity was smaller than the employment levels of Italy and of Spain.

Value added specialisation – top five EU Member States (%, share of distributive trades value added, 2019)

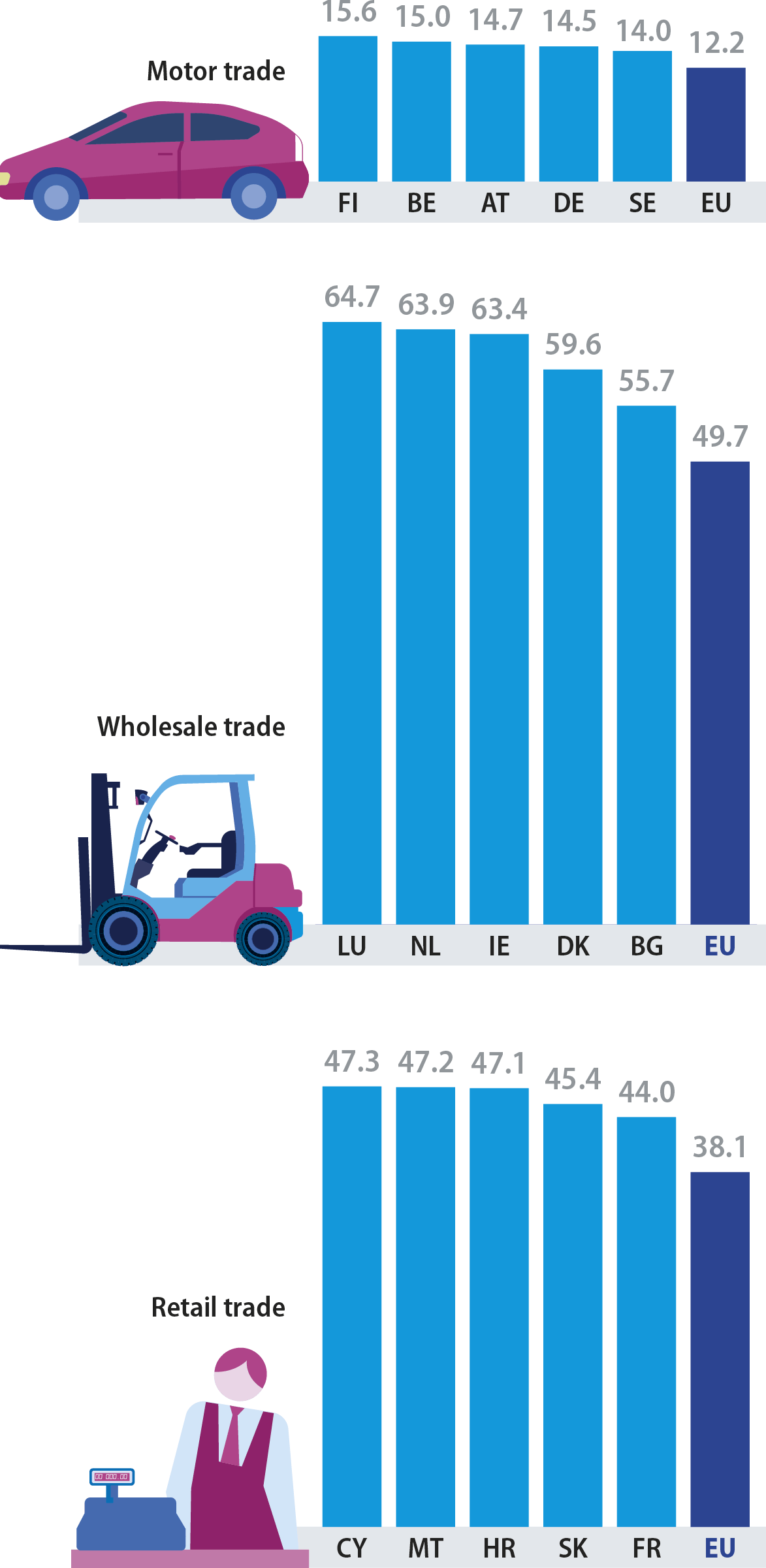

Given the essential, local nature of many distributive trade activities, there tends to be less geographical specialisation than observed for many industrial or other service activities. For example, 15.6 % of distributive trades value added in Finland was recorded in motor trades in 2019, more than in any other EU Member State, but this was not much higher than the EU average (12.2 %).

Luxembourg (64.7 %) and the Netherlands (63.9 %) were the top two EU Member States in terms of the contribution made by wholesale trade to distributive trades’ value added in 2019, underlying their specialisation in distribution, transport and logistics; they were closely followed by Ireland (63.4 %). Cyprus (47.3 %), Malta (47.2 %) and Croatia (47.1 %) – three Member States that host large numbers of tourists each year – recorded the highest contributions of retail trade to distributive trades’ value added.

Note: data are shown for the three NACE Rev. 2 distributive trades divisions.

Source: Eurostat (online data code: sbs_na_dt_r2)

Note: IS, 2018.

Source: Eurostat (online data code: sbs_na_dt_r2)

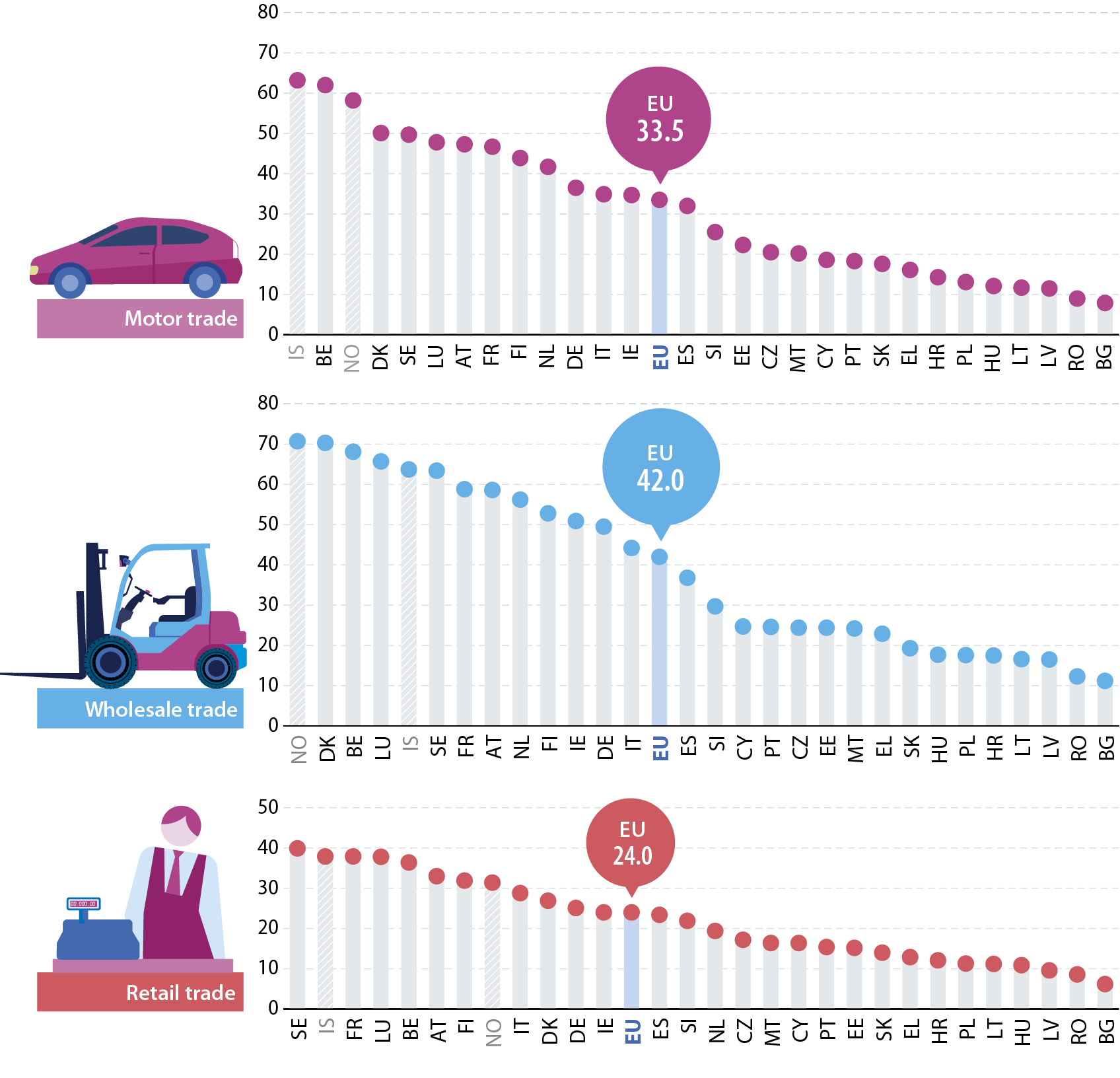

Typically, the lowest average personnel costs can often be observed in sectors with a high incidence of part-time and seasonal work, such as retail trade. Across the EU’s distributive trades’ sector, average personnel costs in 2019 ranged from a high of €42 000 per employee for wholesale trade down to a low of €24 000 per employee for retail trade.

In 2019, Denmark recorded the highest average personnel costs among EU Member States for wholesale trade (€70 300 per employee). Belgium had the highest average personnel costs for motor trade (€62 000 per employee), while Sweden had the highest average personnel costs for retail trade (€39 900 per employee). At the other end of the scale, the lowest average personnel costs for all three distributive trades divisions were recorded in Bulgaria, Romania and Latvia.

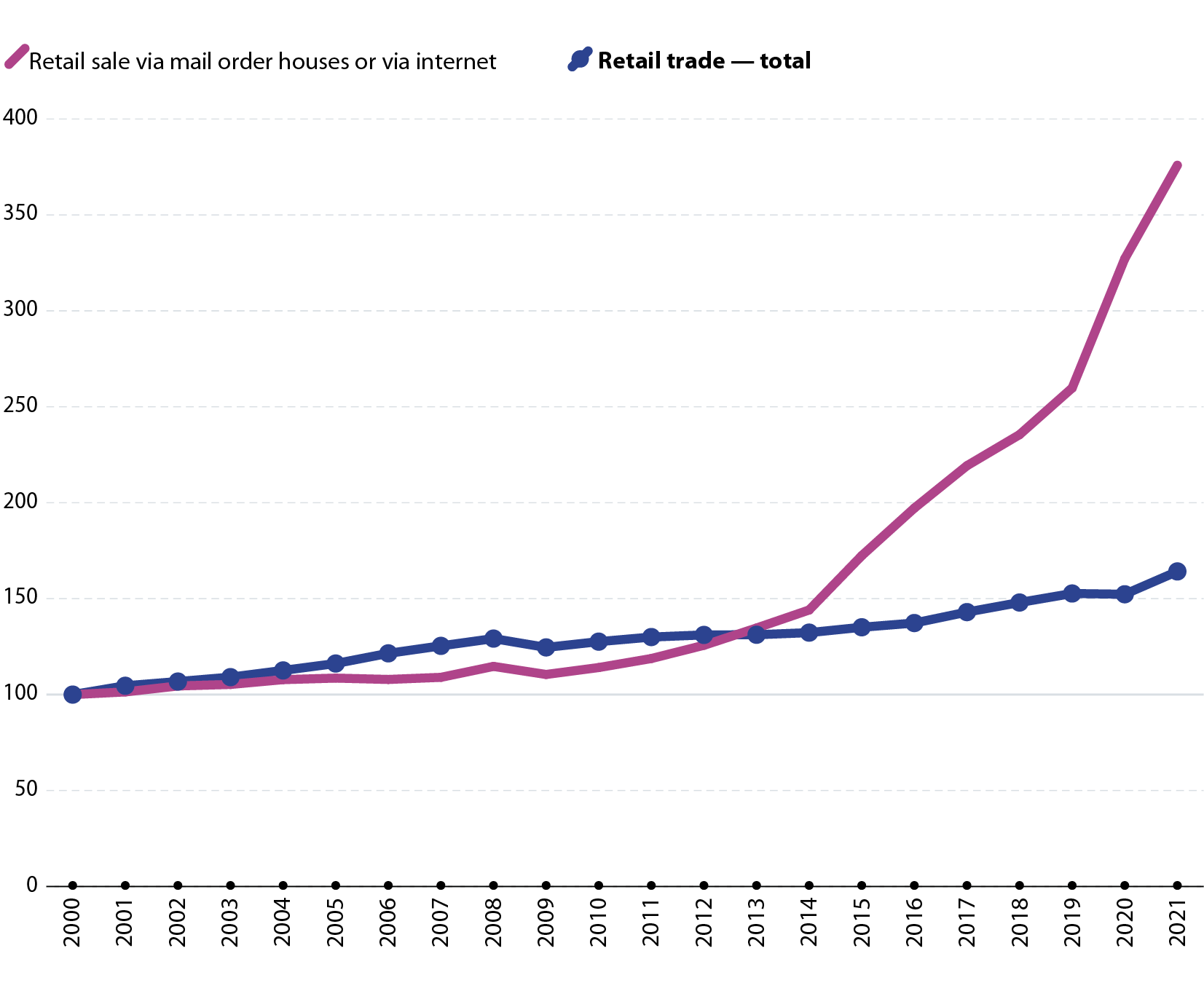

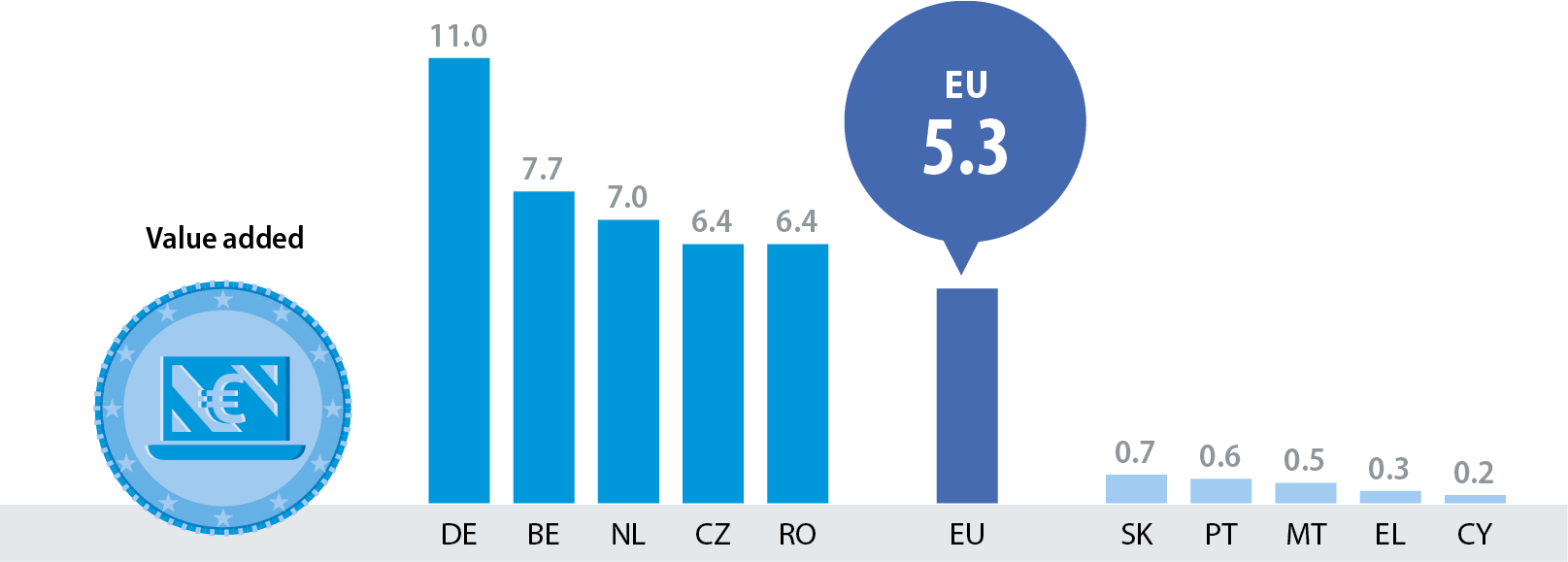

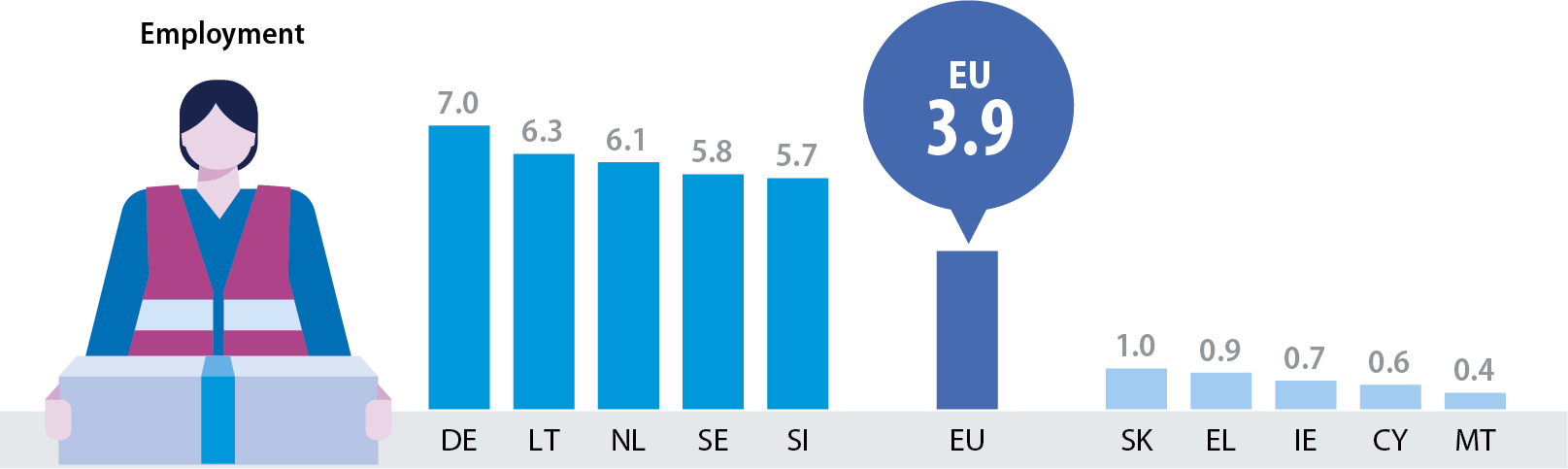

Note: retail trade covers NACE Rev. 2 Division 47 and retail sale via mail order houses or via internet covers NACE Rev. 2 Class 47.91. LU: not available.

Source: Eurostat (online data code: sbs_na_dt_r2)

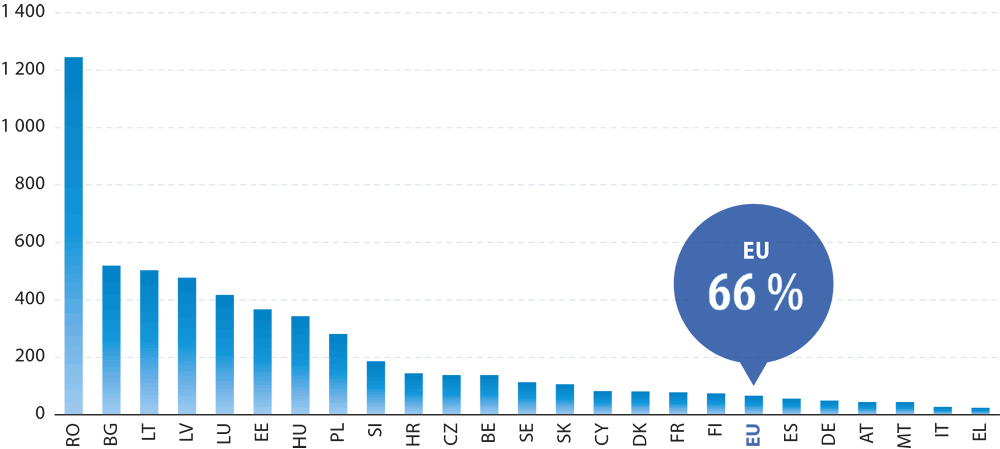

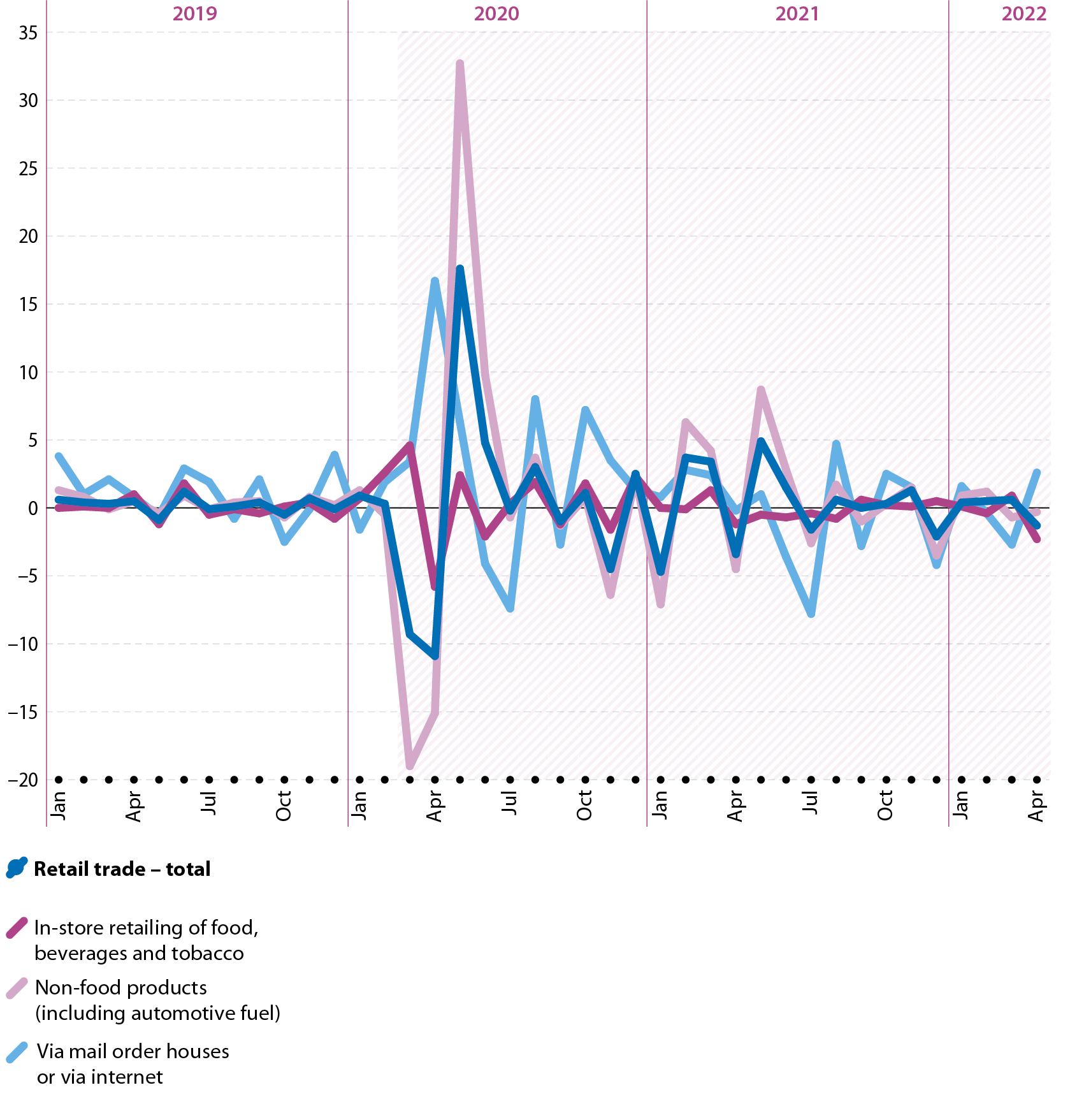

Internet retailing has gained in significance over many years. In 2019, the subsector covering retail sale via mail order houses or via internet accounted for 5.3 % of retailing value added and 3.9 % of retailing employment within the EU. In value added terms, Germany, Belgium and the Netherlands were the most specialised EU Member States in these forms of remote trading, while Greece and Cyprus were the least specialised.