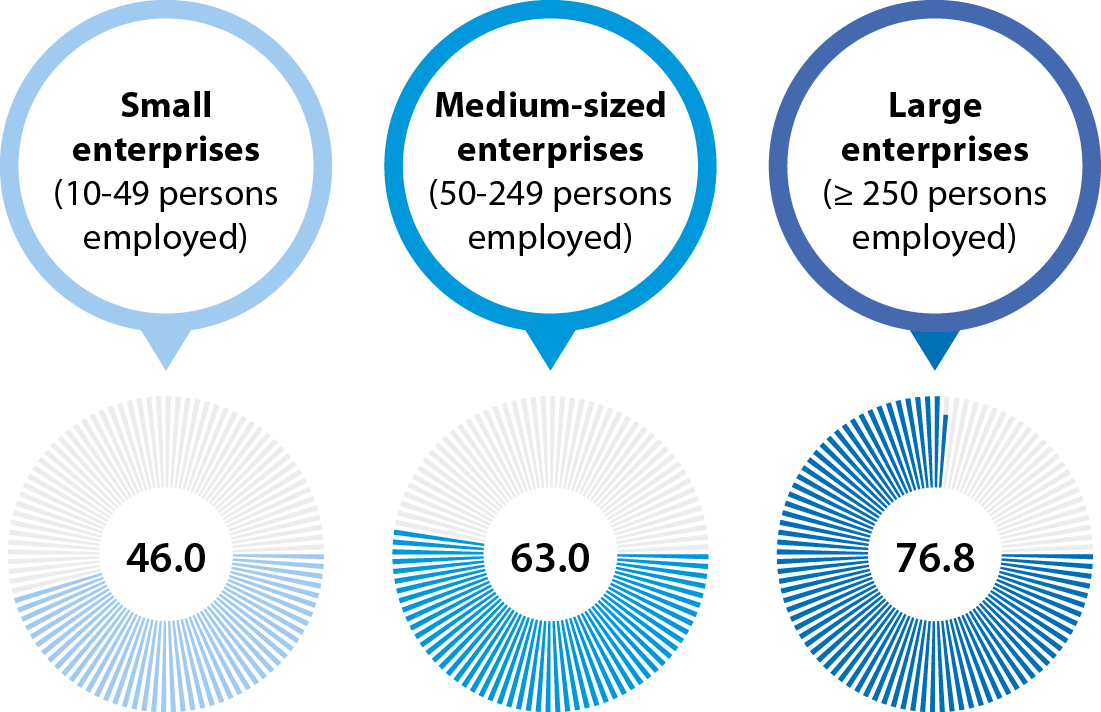

Size of businesses

Business statistics cover industry, construction, distributive trades and most other services. It is important to underline that they exclude a range of economic activities, such as: agriculture, forestry and fishing; public administration; education; health and social work; arts, entertainment and recreation. Alongside these, financial and insurance activities are also frequently excluded, given their specific nature and the limited availability of statistics in this area.

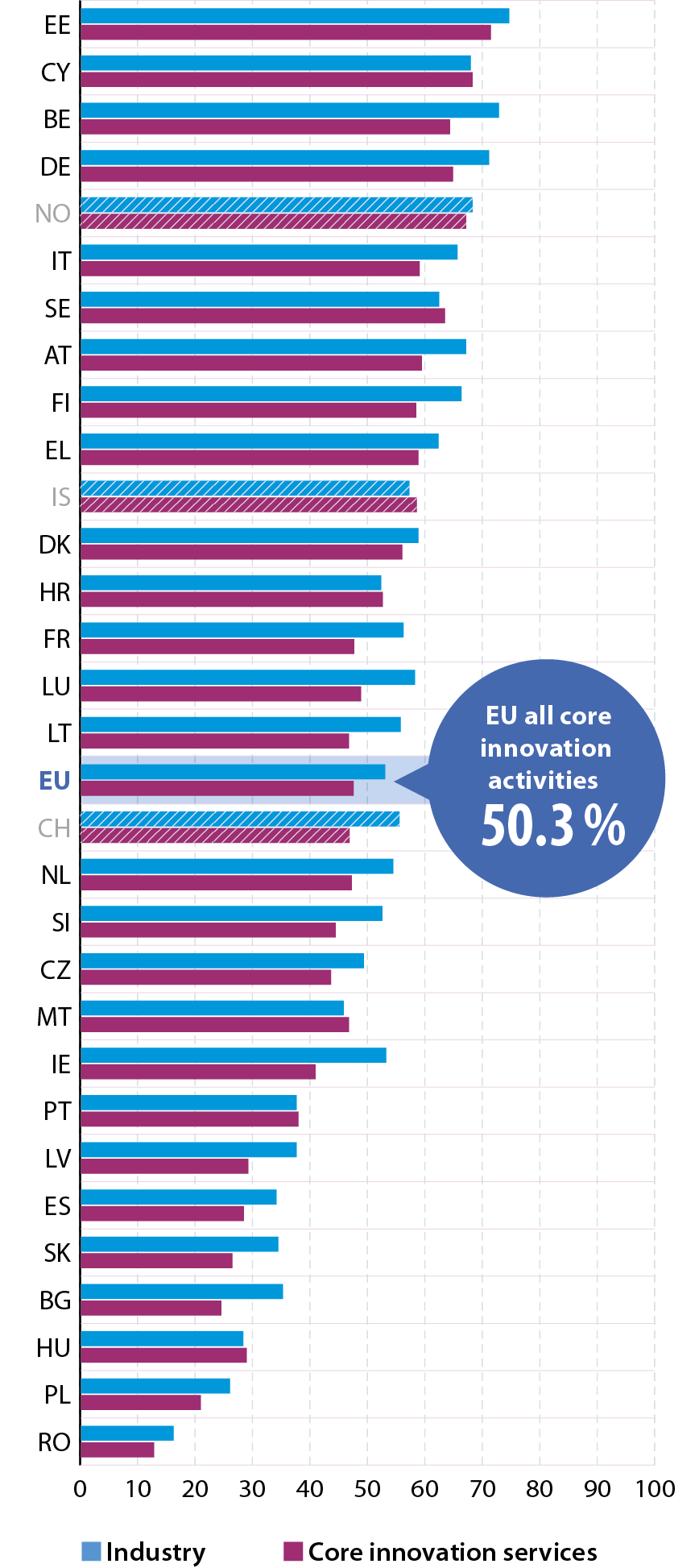

Note: the non-financial business economy covers industry, construction, distributive trades and most other market services outside of financial services.

Source: Eurostat (online data code: sbs_na_sca_r2)

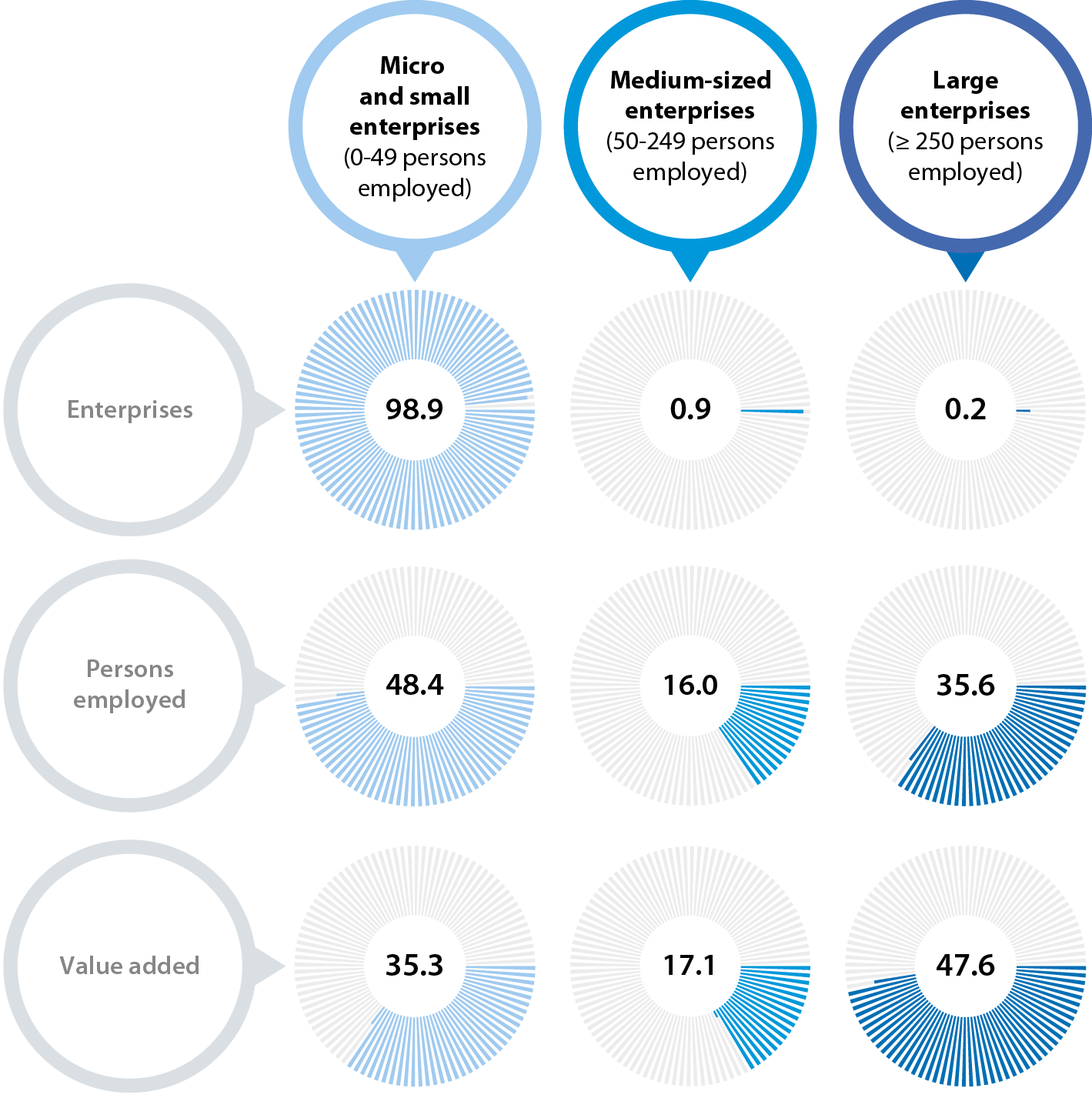

In 2019, there were 23.2 million enterprises in the EU’s non-financial business economy. Collectively they employed 131.5 million people and created €6 852 billion of wealth as measured by value added at factor cost.

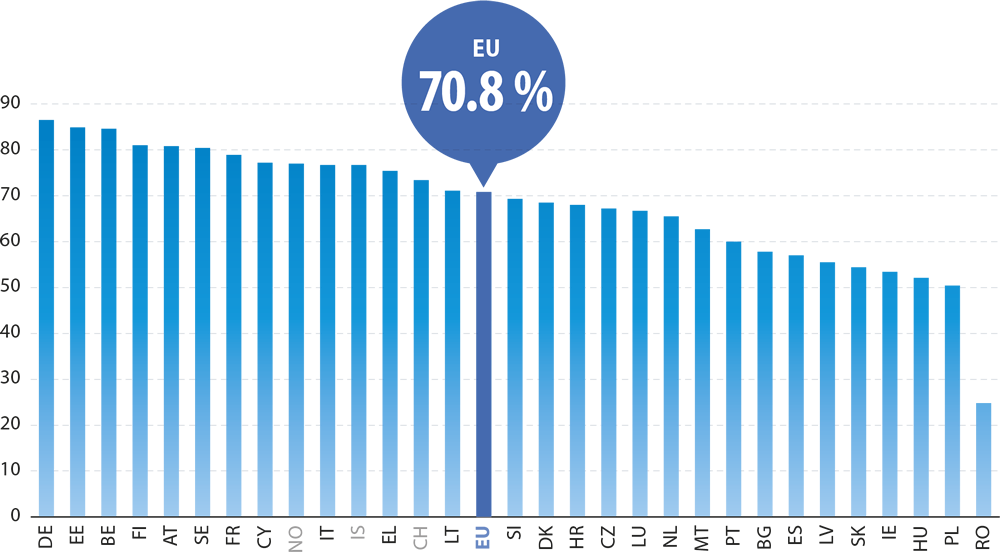

Note: estimates made for the purpose of this publication.

Source: Eurostat (online data code: sbs_sc_sca_r2)

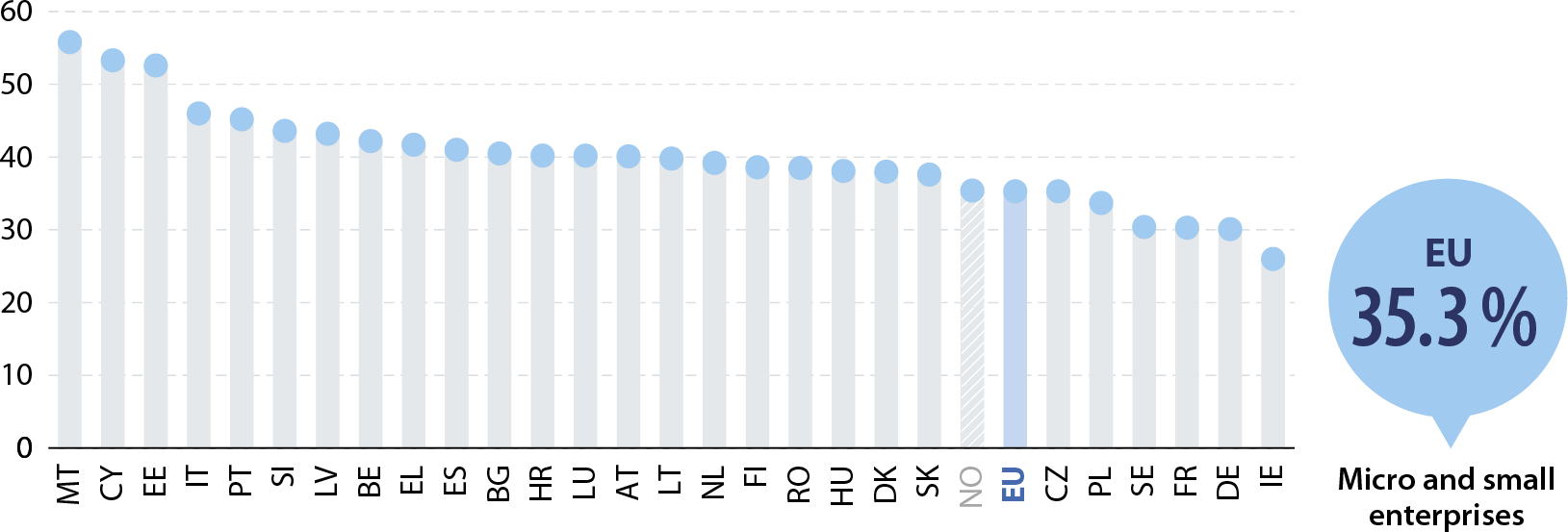

Data relating to enterprises that are active within the non-financial business economy can be presented according to enterprise size and measured in terms of the number of persons they employ. In 2019, the overwhelming majority (98.9 %) of EU businesses were micro or small enterprises employing fewer than 50 persons. Their economic weight was lower in terms of their contribution to employment or value added: micro and small enterprises employed just under half (48.4 %) of the EU’s non-financial business economy workforce, while they contributed just over one third (35.3 %) of the value added.

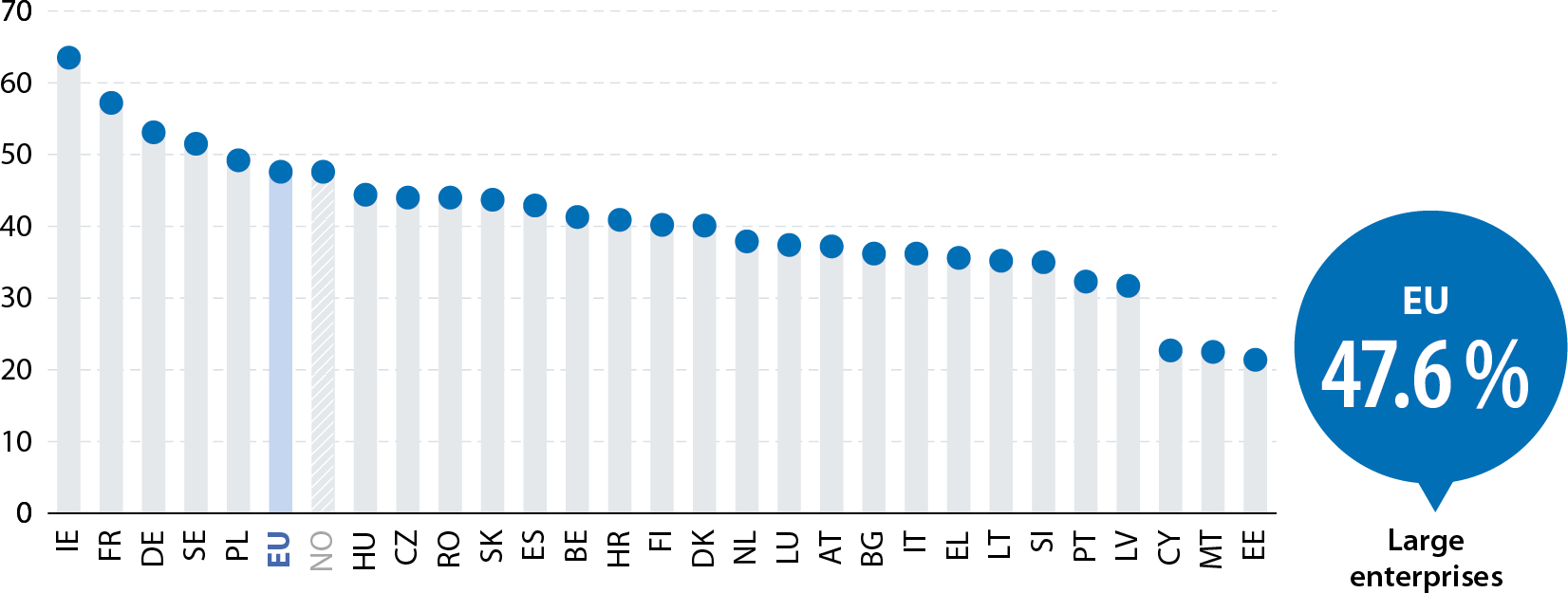

In 2019, there were 43 000 large enterprises (with 250 or more persons employed) in the EU’s non-financial business economy. These large enterprises represented just 0.2 % of the total number of enterprises. However, their economic weight was considerably greater: large enterprises employed more than one third (35.6 %) of the EU’s non-financial business economy workforce and generated an even higher share of its wealth (47.6 % of value added).

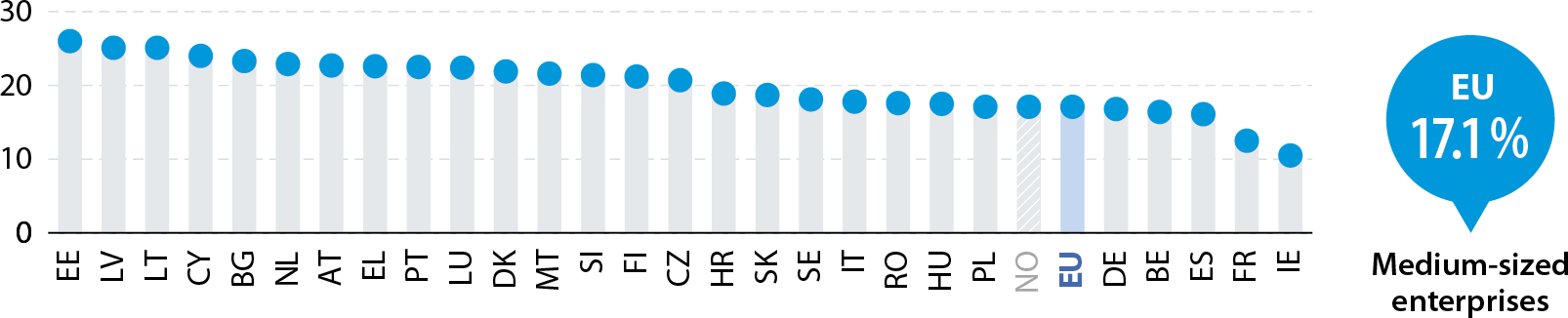

Note: data for the EU are estimates made for the purpose of this publication. PT: excluding real estate activities. CY: excluding mining and quarrying, electricity, gas, steam and air conditioning supply, real estate activities, and repair of computers and personal and household goods. AT: 2016.

Source: Eurostat (online data code: sbs_sc_sca_r2)

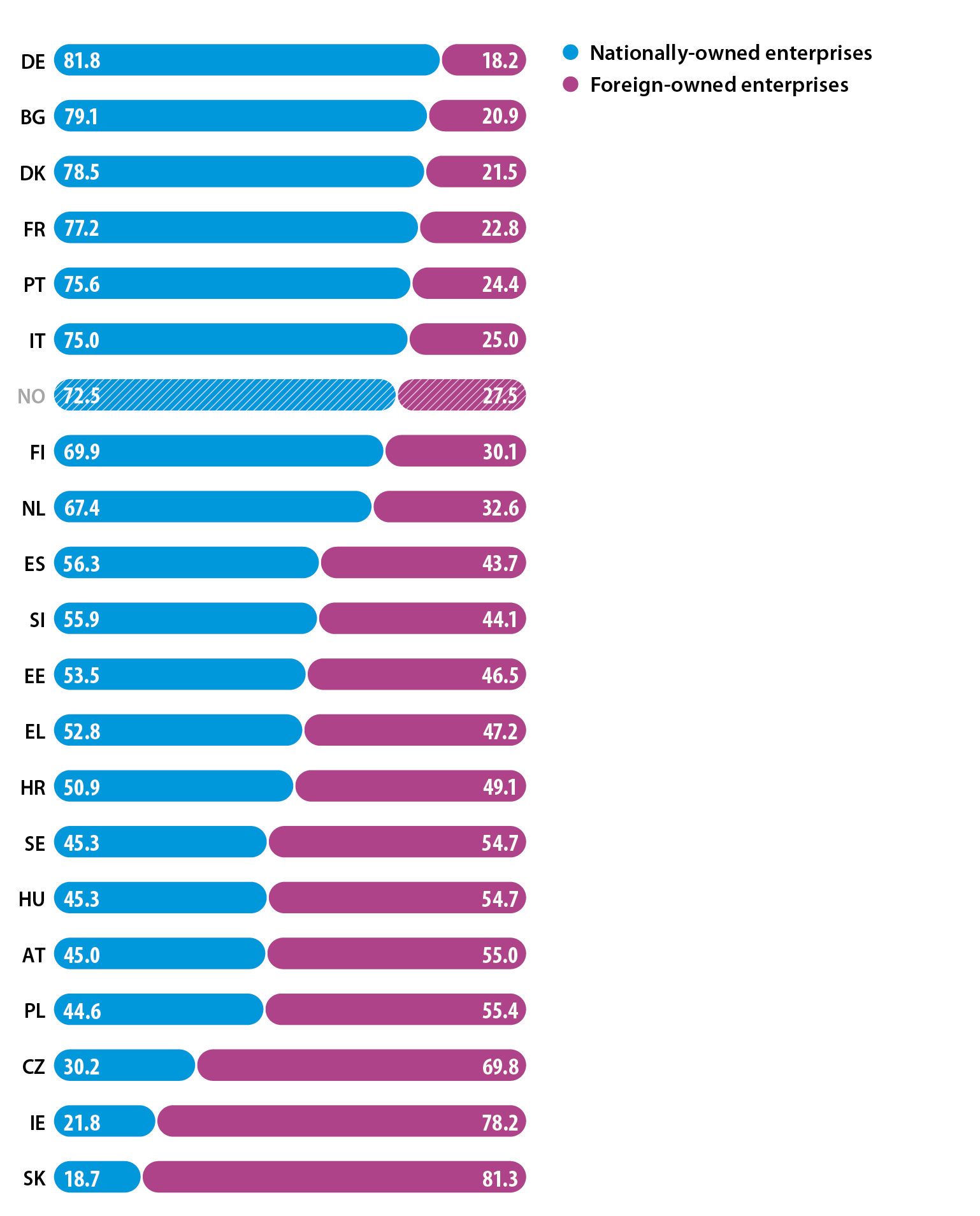

In 2019, micro and small enterprises contributed a relatively high share of the value added in the non-financial business economies of most of the southern EU Member States and Estonia. By contrast, large enterprises were responsible for approximately half of value added in the non-financial business economies of Poland and Sweden, 53.1 % in Germany and 57.2 % in France; this share peaked at 63.5 % in Ireland.