- European Commission

- Employment, Social Affairs and Equal Opportunities

- Employment in Europe 2010

The EU is now recovering from recession, but the recovery is proving to be fragile. The economic recession came to an end in the third quarter of last year, in large part thanks to the exceptional crisis measures put in place under the European Economic Recovery Plan. Beyond the initial rebound, however, the recovery is proving more tentative than in past upturns, which is not surprising given the extent and nature of this crisis.

Nevertheless, economic sentiment in the EU is improving and recently returned to around its long-term average. At the same time, consumers’ unemployment expectations continue to ease, and firms across all main sectors are increasingly less pessimistic about the outlook for employment. As a result, demand for labour has started to show a relative improvement, although generally remaining at levels well below those before the crisis erupted, while workplace activity through temporary work agencies, a leading indicator of a recovery in the labour market, has improved strongly. However, stronger than expected global growth and improved business and consumer confidence indicators have yet to be reflected in hard data for the labour market. Indeed, although the EU is on the path to economic recovery, it appears too early for improvements in economic activity to have had any major impact on the labour market.

Furthermore, while the aggregated impact of the crisis on the labour market may be less in Europe, given the extent to which jobs have been protected, the labour market recovery may lag as a consequence. Indeed, reduced working hours in Europe have led to widespread under-employment, with the existing workforce likely to absorb increased demand through a rise in working hours before any major increase in staff levels takes place. Consequently, it may take some time before there is a clear upswing in the labour market.

The European Commission spring 2010 economic forecasts, the last with detailed forecasts for the labour market, reported that the fragile economic recovery underway in the EU continues to face headwinds from several directions. On the positive side the EU economy is likely to benefit from a stronger-than-expected turnaround in the global economy, most notably in emerging Asia, but opposing this are incomplete balance-sheet adjustments in several sectors/countries, weakness in the labour market which is likely to restrain domestic demand for years to come, and a continued high level of uncertainty regarding global imbalances and financial markets.

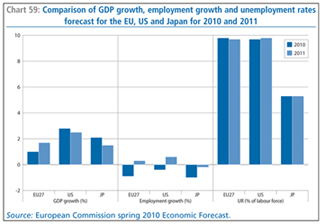

As a consequence, EU GDP growth was expected to remain rather subdued during the first three quarters of 2010, on average, and to regain ground only by the end of the year. This follows from, in particular, the fading impact of the temporary support that kick-started the recovery. Moreover, the pace of recovery was likely to vary considerably across Member States, with some countries (Cyprus, Greece, Ireland, Latvia, Lithuania and Spain) expected to remain in recession in 2010 while others were forecast to post growth in excess of 2% (Luxembourg, Poland and Slovakia). An annual growth rate of about 1.0% was forecast for the EU for 2010, considerably below that expected for the US and Japan (around 2.8% and 2.1% respectively), while for 2011, EU GDP growth was expected to accelerate to 1.7% (Chart 59). By 2011, all EU countries, with the exception of Greece, were expected to have returned to positive economic growth.

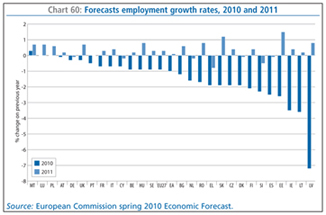

Despite apparent signs of stabilisation, the labour-market situation was forecast to remain weak for some time to come, while the mounting need for firms to improve productivity and profitability suggests that further adjustments in the labour market will weigh more heavily on headcount than hours. Employment was expected to contract by 0.9% this year, leading to a further rise in the unemployment rate which was set to average 9.8% for the year as a whole. This compares with weaker employment contraction of 0.4% forecast for the US, and a similar 1.0% contraction in Japan, while the unemployment rate in the US was expected to remain very similar to that in the EU. Among EU Member States, all were expected to see further employment contraction in 2010 apart from Luxembourg and Poland, and Malta where it was forecast to expand slightly. The largest contractions were again expected in the Baltic States, Ireland and Spain (Chart 60).

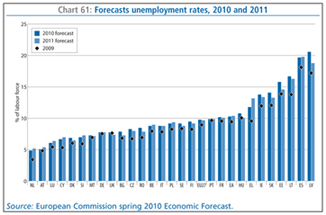

The relatively limited overall labour-market adjustment in the EU during the crisis, reflecting a higher degree of labour hoarding during this recession which helped stem the rise in unemployment, suggests a rather jobless recovery ahead and (potentially persistent) high levels of unemployment. For 2011, job growth of only 0.3% was forecast for the EU, lower than that for the US (0.6%), although on the positive side the vast majority of Member States were likely to see a return to employment expansion (albeit limited). The unemployment rate was expected to remain at 9.7%, only marginally down on 2010, while in the US and Japan the rates were also forecast to remain at their present, relatively high, levels. Among EU Member States, unemployment was expected to remain high compared to pre-crisis levels for some time, especially in the Baltic States, Greece, Ireland, Slovakia and Spain (Chart 61).

However, the more recent interim European Commission forecast released in September 2010 reports that the EU economy, while still fragile, is recovering at a faster pace than envisaged in early 2010 (GDP growth for the EU in 2010 is now forecast at 1.8%, a sizeable upward revision). As a result, the labour market may perform somewhat better this year than expected at the time of the spring forecast. Nonetheless, conditions are set to remain weak, reflecting, inter alia, the partial unwinding of support measures and ongoing structural adjustment across sectors and firms.