EU equity markets

date: 30/11/2020

Europe’s public equity markets have fallen behind in global terms. Its markets are much smaller than those in the United States, despite having a similar-sized economy. And they are smaller than Asia’s markets when measured by market capitalisation relative to gross domestic product (GDP). In light of this relative decline of public equity markets in the European Union, the European Commission commissioned economics consultancy Oxera Consulting LPP to study the functioning of primary and secondary equity markets in the EU and identify policies to help advance the development of a capital markets union (CMU).

Primary markets

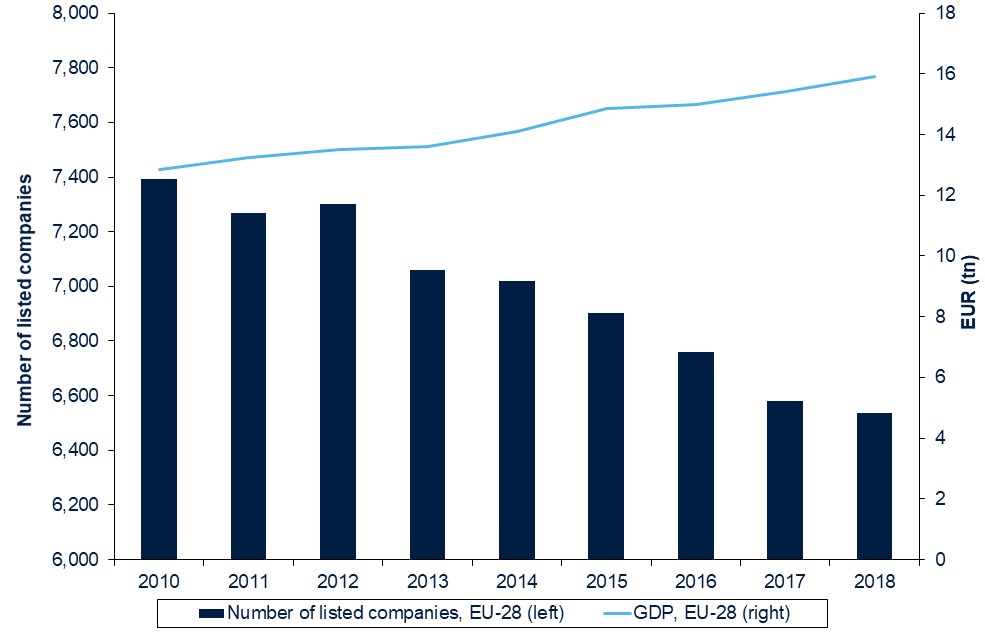

Oxera’s analysis shows that the number of listings in the EU-28 declined by 12%, from 7,392 in 2010 to 6,538 in 2018, while GDP grew by 24% over the same period (Figure 1). Some 8,000−17,000 large companies in 14 EU Member States are eligible to list but are not seeking to do so.

Source: Oxera analysis of stock exchange data; Eurostat

The decision to list depends on the benefits of going public outweighing any negative impacts. Feedback from market participants indicates that the initial and ongoing costs of becoming a public company have risen considerably in recent decades, and widened the gap between public and private companies. The study estimates the total financial cost to currently be in the region of 5–15% of gross proceeds, and typically more for those raising smaller sums.

The decline in number of listed companies has also been affected by firms exiting public markets. Data from the major EU exchanges indicates that delistings have predominantly been driven by increased M&A activity. Based on a survey of European listed companies, Oxera found that the main reasons for companies voluntarily choosing to delist include the challenges associated with meeting regular financial reporting requirements; the time and cost associated with compliance and administration; annual fees paid to advisers, brokers and exchanges; and requirements to disclose sensitive information.

Even though regulation is not the primary driver of the decline in listings, there is room for future modernisation and streamlining of the listing rules. The regulatory costs associated with listing are particularly relevant for smaller issuers, for which alternative private funding options may be more readily available.

Secondary markets

Over the past decade, there has been a fundamental change in how equity is traded in Europe. This has been driven by technological development and entry by new players, and supported by regulatory change. Oxera carried out a comprehensive analysis of trading activity in EU equity markets. The study finds that:

- The volume of equity trading in the EU (including the UK) has been fairly stable

- There is significant home bias in equity trading

- Cross-border trading is mostly concentrated among stocks in large financial centres. Insurers and pension funds account for 30% of domestic investment in large and mid-size financial centres, compared to 9% in small financial centres

- Consolidation of some exchanges and the growth of alternative trading platforms has mostly occurred in Western Europe and has not yet had an impact on equity trading in Central and Eastern Europe, with the exception of the Baltic exchanges

Oxera’s analysis indicates that increased competitive pressure has led to lower trading fees and more choice for traders and investors. Furthermore, despite an increase in trading fragmentation, the implicit costs of trading (e.g. including the spreads and price impacts of executing trades) have not increased. This is because traders have access to the necessary technology to search for the best available option to execute their trade.

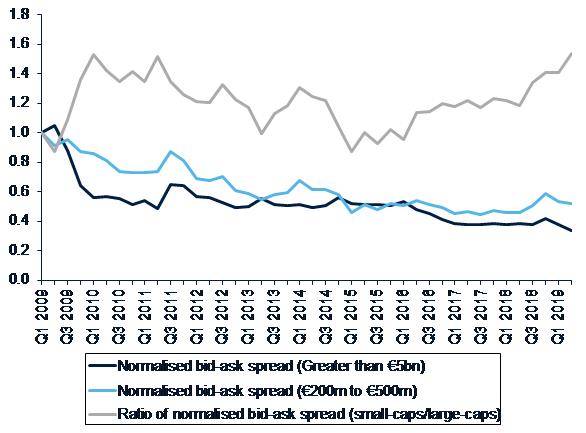

While there has been an improvement at the aggregate EU level, liquidity is still a major concern for SMEs and small financial centres. The liquidity of SME shares has been further challenged by rules around unbundling of trade execution and research fees, as well as the increased popularity of passive investment. Oxera found that the improvement in bid-ask spreads at the EU level is more significant for large- than for small-cap stocks (Figure 2).

Source: Oxera’s analysis of Virtu data

Based on a comprehensive analysis of primary and secondary markets, the study identifies key areas for policy focus (summarised in Figure 3) and a number of more specific policy proposals (set out in more detail in the main report) to provide a better environment for listings and specifically aimed at improving liquidity for SMEs and local capital markets.

What can the Commission do?

The action plan on capital markets union, which the Commission adopted on 24 September 2020, stresses that in particular SMEs need more equity to recover from the economic shock and become more resilient. The new measures put forward by this action – such as, for example, the planned establishment of an EU-wide platform to provide investors with seamless access to financial and sustainability related company information, and the simplification of listing rules on SME growth markets – aim to make companies more visible and thereby facilitate their access to all available funding sources. The study carried out by Oxera will inform any Commission action to further facilitate the use of market funding.

Primary markets:

- Revisit approach to disclosure

- Encourage flexibility in the use of dual-class shares

- Promote institutional investor participation in IPOs

- Improve corporate governance standards to keep down agency costs

- Attract retail investors to invest in public equity markets

Secondary markets:

- Investigate role of EIF and/or EBRD to act as an anchor investor

- Attract more institutional investment into local capital markets

- Promote open access and interoperability links between CCPs, or facilitate cross-border mergers at market infrastructure level

- Encourage more investment in SMEs

- Strengthen corporate governance to avoid scandals and build public trust in equity markets.