Post-crisis reforms

date: 21/12/2017

The European Commission has published a report on policy actions taken by EU countries in the financial sector between 2008 and 2015. These measures were taken as a response to the global financial crisis and in the context of the evolving EU framework of country surveillance. The report looks at reforms at both EU and national level and shows that post-crisis reforms have paid off.

The importance of country surveillance

The major trigger for the financial crisis was the sub-prime mortgage crisis in the US, the repercussions of which spilled over into Europe in 2007. In the years that followed, what had initially been a financial crisis turned into a banking crisis and a crisis of sovereign debt, soon affecting the real economy. The result was that the EU economy entered the steepest downturn on record since the 1930s.

The financial crisis highlighted the need for better regulation and supervision of the European financial sector. The EU responded most notably through the creation of the Single Supervisory Mechanism and the Single Resolution Mechanism under the Banking Union and by strengthening its "single rulebook" for the financial sector. In parallel, the new European Stability Mechanism provided financial assistance for the banking sector, and the Commission adapted its state aid rules for banks. Actions taken at Member State level have complemented these European initiatives – and this is the focus of the recent report.

In a major step forward, country monitoring has become an important feature of the EU's economic and financial governance. It makes it easier to detect a build-up of financial imbalances in a particular Member State early. It also facilitates pre-emptive action to avoid, or at least help contain, a crisis. Economic and financial conditions differed greatly among Member States at the onset of the crisis, and certain warning signals were not sufficiently heeded. Rapid credit growth and rising house prices; a banking sector increasingly reliant on borrowed funds; insufficient 'equity buffers' (i.e. adequate margins of value in assets over liabilities) and non-performing loans: these are just some of the variables which are now better monitored for each EU country.

The report also highlights the importance of cooperation between the Member States and the EU institutions through, for instance, the exchange of best practices and peer pressure. EU policy guidance, meanwhile, takes into account the great diversity of Member States' financial situations and is tailored to specific challenges, while ensuring that there is a clear and consistent approach across countries. This is reflected in the European Semester and the Economic Assistance Programmes under which the Commission and the EU Council cooperate with the Member States in identifying and tackling emerging risks to the economy and promoting economic and social reforms.

Post-crisis reforms bear fruit

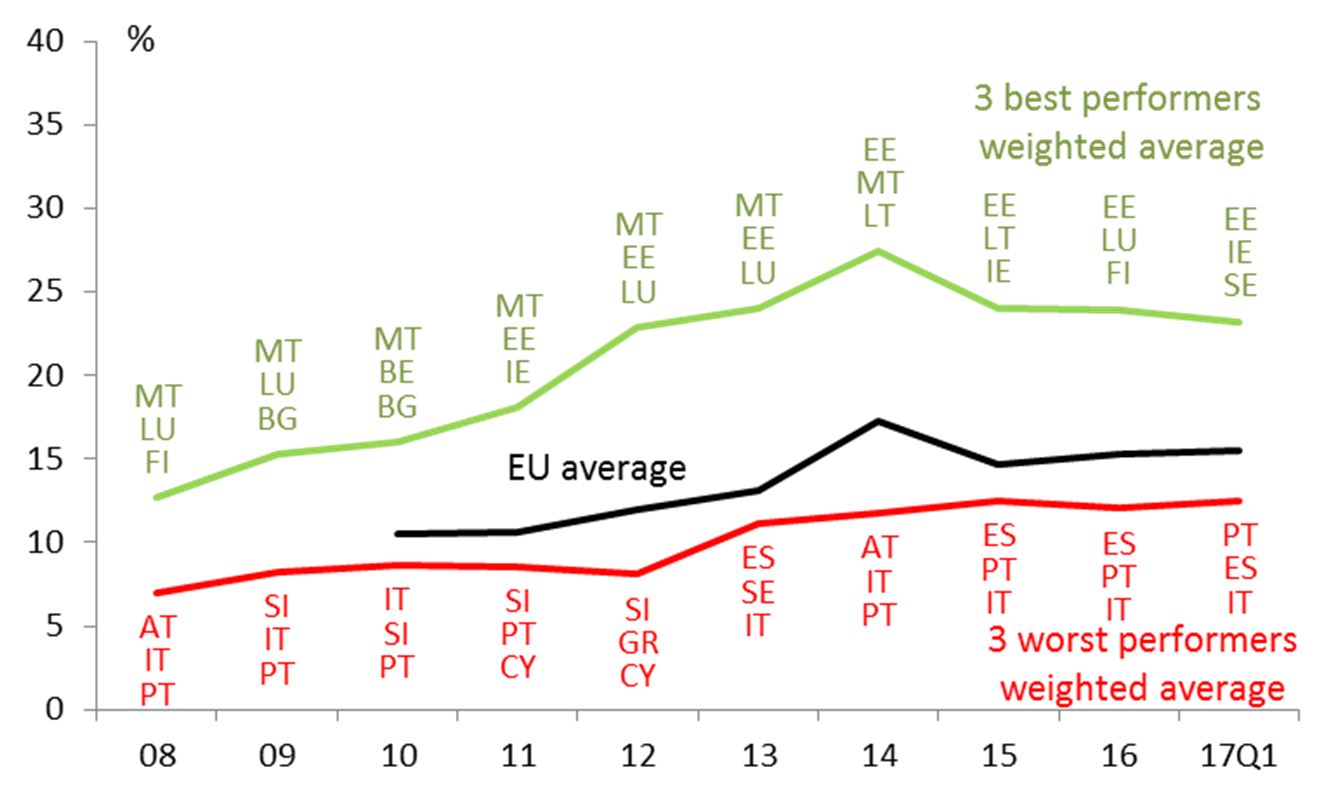

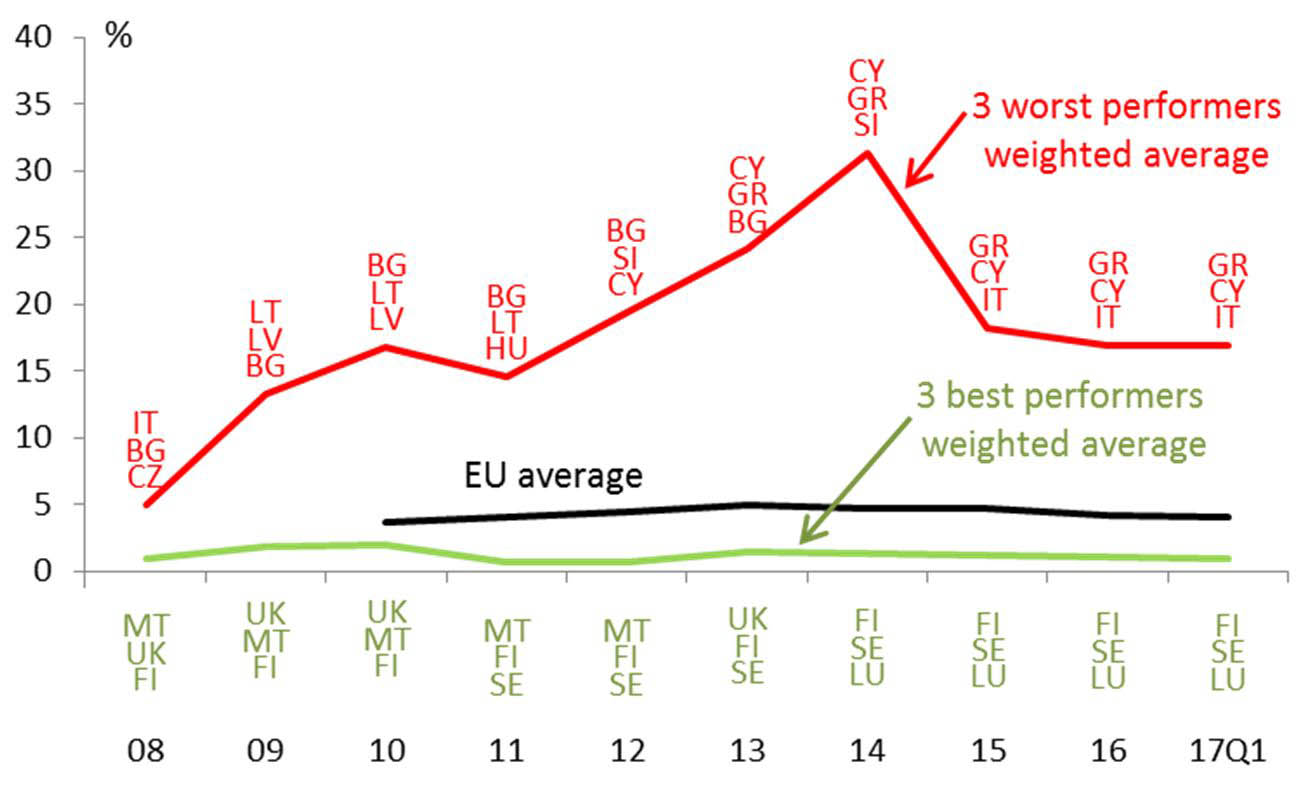

Thanks to measures taken both at Member State and EU level, considerable progress was made towards stabilising the economy. But the situation remains uneven among different EU countries. This holds, for instance, for the development of banks' capital levels and for non-performing loans in banks' balance sheets (see charts below illustrating the evolving positions of Member States).

Note: Gross total non-performing debt instruments (% of total debt instruments)

Source: ECB statistical data warehouse

The report shows that there is a renewed confidence in the EU financial sector, which is now much less reliant on central bank borrowing. Banks are stronger thanks to higher capital buffers. Meanwhile, interest rates on both loans and deposits are declining and credit ratings are improving. Still, the analysis in the report highlights that weaknesses remain. Low interest rates, for instance, as well as a high level of non-performing loans, hamper some EU banks' profitability. In addition, the sovereign-bank nexus – i.e. the exposure of banks towards governments and vice-versa – increased as a result of the crisis, as banks generally hold a large share of government debt. However, this has been partially mitigated by European Central Bank asset purchases.

Bank lending to households and companies in the euro area stopped contracting in early 2015. Nonetheless it is still below pre-crisis levels, due to over-indebted households and firms, weak demand and the fact that some banks have repaired their balance sheets by according fewer loans rather than boosting capital.

The report recognises that stabilisation measures and financial regulations may weigh on growth in the short term. However, it stresses that their impact is contained and temporary. Furthermore, a key message of the report is that, in the long term, financial stability is essential for sustainable growth.

Read the report