Non-performing loans

Related topics

Bankingdate: 28/02/2018

On 18 January 2018, the European Commission presented its first progress report on the EU's ongoing work to reduce non-performing loans (NPLs) in the European banking sector. The report follows on from an action plan to tackle NPLs that was agreed by EU economic and finance ministers in July 2017. It shows that NPLs have continued to fall in nearly all EU countries, although the situation differs significantly across Member States. The next step for the Commission is a package of measures to tackle NPLs, which is based on the action plan. It will be adopted in March.

Legacy of the crisis

NPLs are loans where the borrower – either a person or a company – is unable to make the scheduled interest or repayments for 90 days or more. NPLs can weigh heavily on banks' short- and long-term performance. This is because they generate less income than performing loans, which reduces a bank's profitability and may cause losses that diminish its capital. In extreme cases, this can threaten the viability of the bank, which has potential negative implications for financial stability in the EU as a whole. Furthermore, NPLs tie up significant amounts of a bank's resources, which reduces their ability to lend. This especially affects small and medium-sized companies (SMEs), which rely on bank lending much more than larger firms.

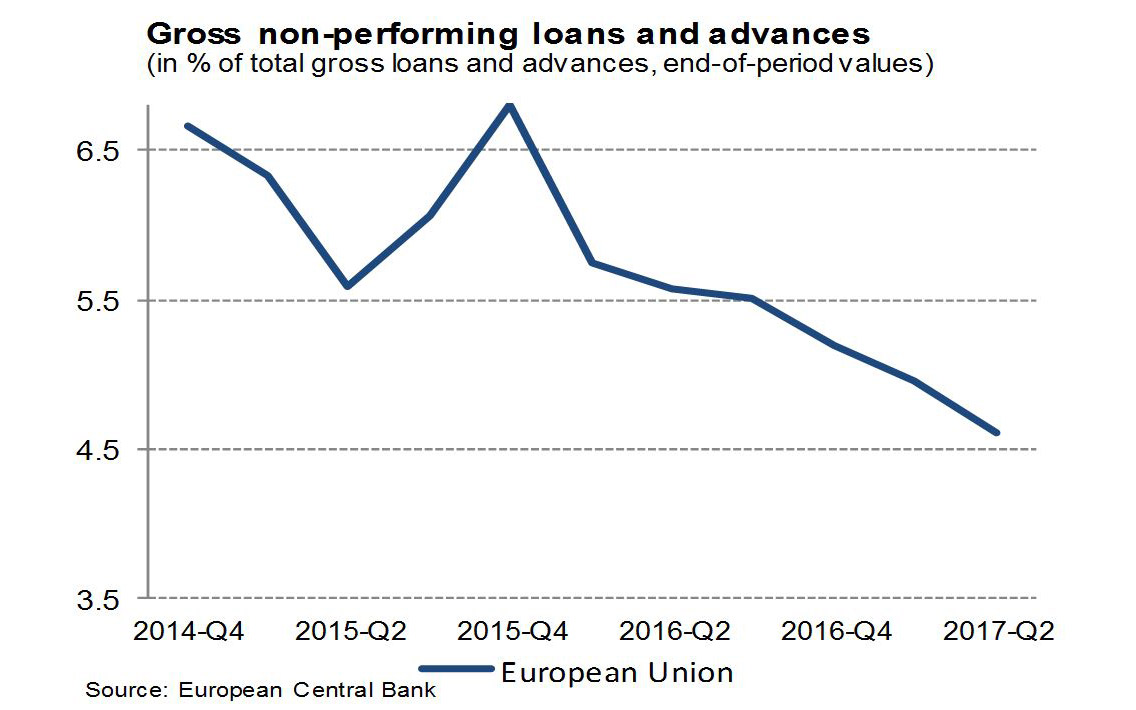

In the aftermath of the financial crisis and subsequent recessions, many banks experienced a serious build-up of NPLs on their books. Now, however, the EU's banking sector is in a much better state than it was a few years ago. This is also due to a gradual decline in NPL ratios over recent years. According to figures from the European Central Bank (ECB), the NPL ratio fell to 4.6% at the end of the second quarter of 2017, down by roughly 1 percentage point year-on-year (see figure 1).

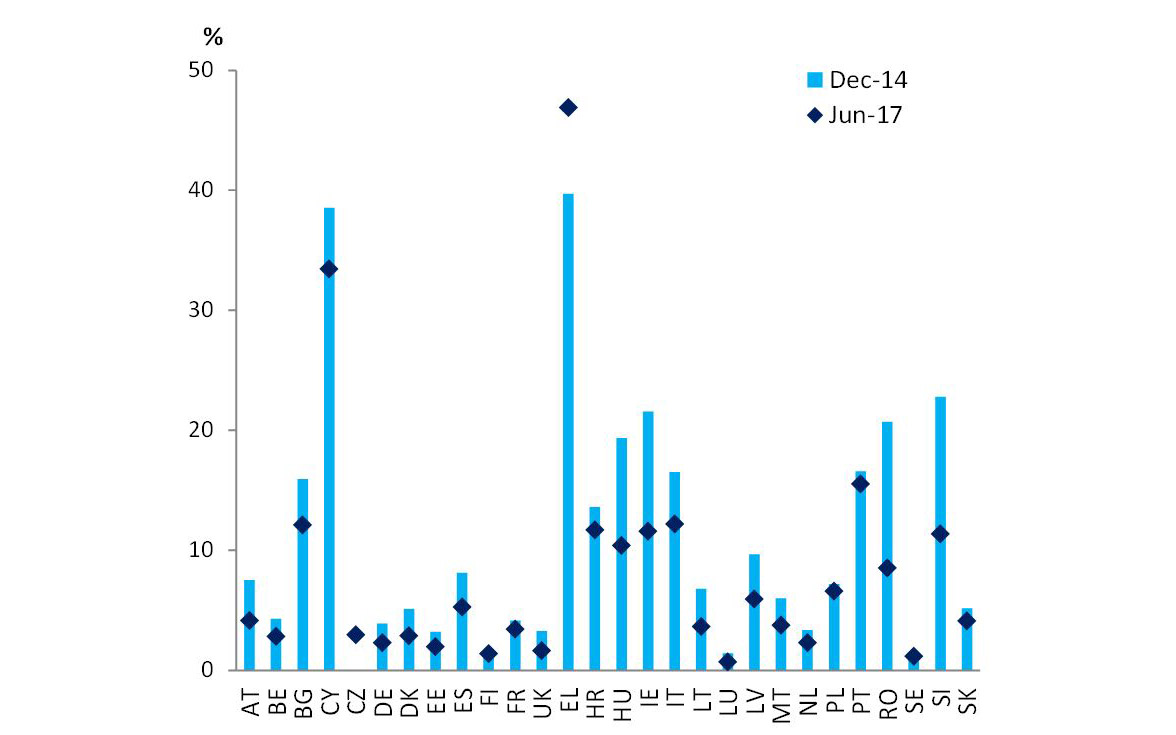

But despite the downward trend, at €950 billion, the total volume of gross NPLs across the EU remains high, particularly when compared to other parts of the world. Both the US and Japan, for instance, had NPL ratios of approximately 1.5% end 2016. And the situation differs significantly from one Member State to another (see figure 2), although policy action and a stronger macroeconomic environment have led to some improvement in the most affected countries.

Note: Dec-2014 not available for CZ

An EU dimension

While tackling NPLs is primarily the responsibility of the affected banks and Member States, there is also a clear EU dimension. As the economies of Member States are in many ways interlinked, especially within the euro area, the potential for spill-over is great. So a solid, comprehensive European strategy to address the problem of NPLs is essential to create a strong EU banking sector and restore investor confidence. Consequently, the Commission, along with the Member States concerned, has been working hard to tackle the issue for some time already. The next step is a package of new legislative as well as non-legislative measures, which the Commission will put forward in March. The measures will aim to reduce the level of existing NPLs and prevent the build-up of excessive levels of new ones in the future.

The package will include a blueprint establishing common principles to help Member States that choose to set up national asset management companies (AMCs) to help banks clean up their balance sheets. Transferring bad loans from banks to an AMC allows viable banks to improve their stability and focus on their core task of lending and offering services to households and firms.

The package will also include measures to further develop the secondary market for NPLs. Other measures will offer greater protection to secured creditors, such as banks, by allowing them (under certain conditions) more efficient ways to recover value from NPLs through accelerated extrajudicial collateral enforcement (AECE). The package will also introduce statutory prudential backstops, covering newly granted loans by banks that later turn non-performing. This would prevent the build-up and potential under-provisioning of future NPL stocks through time-bound prudential deductions from banks' capital positions. Finally, the Commission is exploring, together with the ECB and the European Banking Authority (EBA), ways to improve transparency, for example by making data on NPLs more readily available and easier to compare.

Tackling NPLs is a joint effort. The July action plan combines measures to be carried out by national governments, bank supervisors and EU institutions. The goal is that these measures will help create incentives to successfully address the problem of NPLs – and the tools and support needed to do so.

Read more about the progress report on the reduction of non-performing loans