Interview with William Wright

Related topics

Capital Markets Uniondate: 26/05/2015

Finance Newsletter spoke to William Wright, Managing director of New Financial, about Capital Markets Union.

Mr. Wright, the European Commission has recently launched its Capital Markets Union project. What is your take on the Commission's plans in this area?

By helping to break down unnecessary and artificial barriers, Capital Markets Union could have a hugely positive effect in encouraging the more efficient flow of capital across Europe. It could simplify access to a wider range of funding for companies, reduce costs for investors, and help increase much-needed longer term investment.

In a broader context, how do you see the Capital Markets Union benefitting the economy as a whole?

It could have a transformative impact. Capital Markets Union could unlock hundreds of billions of euros of much needed investment in Europe. And, it can help bridge the artificial divide between finance and the ‘real economy’ by showcasing what finance should be about: channelling savings into productive investment.

New Financial has recently carried out a study on the Capital Markets Union. Could you tell us something about the key findings?

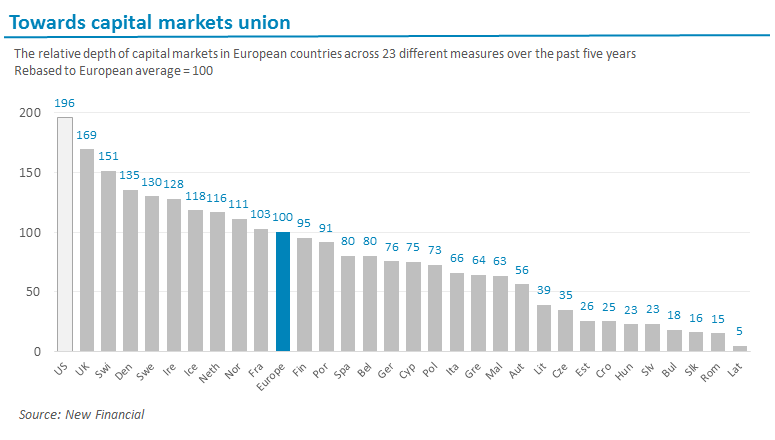

Our research measured the relative depth and development of capital markets in each of the 28 EU member states across 23 different measures – ranging from the size of the pensions industry to levels of venture capital investment in each country. We came up with three main findings:

First, there is a far bigger difference in the depth and development of capital markets between different countries within Europe than there is between Europe and the US, which is often held up as a model for developed capital markets. On average, European capital markets are just over half as developed as in the US, but that hides a huge range. Capital markets in a small number of countries such as Denmark, the Netherlands or the UK are nearly as developed as in the US (and sometimes more developed). But a large number of smaller countries – particularly those member states who joined the EU in 2004 and 2007 – have very nascent capital markets.

Second, from a political and economic perspective, Capital Markets Union should focus on how it can help increase investment in smaller economies with less developed capital markets, instead of how it can help boost the City of London as a financial centre or the capital markets industry. It is unrealistic to expect that capital markets in, for example, Latvia or Croatia are going to be as deep as in the US tomorrow. But if Capital Markets Union can help capital markets develop in these countries to the average level across Europe it could increase investment by more than €100bn a year.

… and what can governments do?

Yes, this is my third point. Capital Markets Union will not deliver its full potential unless it can encourage national governments to help create bigger pools of long-term capital in the form of pension funds, insurance assets, a retail investment culture, or even some form of sovereign wealth funds. Our research showed clearly that countries with bigger pools of capital have deeper capital markets, which means their economies are less reliant on the banking system for funding and their citizens have access to more savings and investment options to help secure their future prosperity.

Thank you for talking to us Mr. Wright. We are sure our readers will be interested in reading the full report, which they can find here.