- European Commission

- Employment, Social Affairs and Equal Opportunities

- Employment in Europe 2010

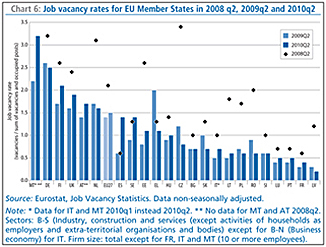

Demand for new workers declined strongly over 2008 and most of 2009 in line with the economic downturn. The EU job vacancy rate (i.e. the number of vacancies relative to the sum of vacancies and occupied posts) started to drop continuously from the second quarter of 2008, falling from a level of 2.2% in the first quarter down to 1.3% in the third quarter of 2009, when it bottomed out. In total the rate fell by 0.9 percentage points (or around 40%) over this period, although underlying this development is significant variation in the size of the decline in demand across individual Member States. Driven by an improvement in Germany, the vacancy rate finally started to rise again in the fourth quarter of last year, when it increased moderately to 1.4 %, and then rose again in the first quarter of 2010 to reach 1.5% where it stabilised. Although this indicates a relative improvement in demand for new workers, the rate remains well down on the levels observed at the start of 2008.

Among the larger Member States, vacancy rates in the second quarter of 2010 remained well down on the levels recorded in spring 2008 (Chart 6). The decline in the vacancy rate relative to the second quarter of 2008 has been most pronounced in Poland (down by 1.1 percentage points, or by two-thirds), reflecting the cooling-off in employment expansion over 2008 and subsequent slight contraction in 2009. Rates were down by a more moderate amount compared to the spring of 2008 in France (by 0.2 percentage points), Germany (down 0.7 percentage points), Italy (down 0.3 percentage points) and the UK (by 0.5 percentage points). In contrast, the rate had risen substantially in Spain to well beyond the already low levels two years earlier, reflecting a sharp improvement over the last year. While the falls for France and Italy still represent relative declines of around a third on the second quarter of 2008, those for Germany and the UK are more limited (at around a fifth).

By the second quarter of 2010, the rate stood at 0.6–0.7% in Italy and Poland, and at only 0.4% in France, the second lowest rate in the EU. However, it remained relatively high in Germany (2.5%, the second highest rate in the EU) and the UK (1.9%), reflecting persisting labour/skill shortages and continued substantial job opportunities despite the crisis and increased unemployment. Official sources in Germany and the UK confirm that, although by early 2010 registered job vacancies were still markedly down on pre-crisis levels, overall vacancy levels remained reasonably high at around 500 thousand in each country.

Other than Sweden, all the other Member States for which vacancy data is available still recorded rates for spring 2010 substantially down relative to those in spring 2008, although many have seen an improvement over the last year. The sharpest falls (of around 1.5 percentage points or more) were registered in the Czech Republic, Estonia, the Netherlands and Romania while in relative terms the declines have also been substantial in Latvia and Lithuania. Apart from Germany and the UK, demand for new workers remained relatively strong in Austria, Finland, Malta, and the Netherlands (all with rates in excess of 1.5%) in the second quarter of 2010, despite the strong declines relative to early 2008. At 0.5% or under, in addition to France, labour demand remained weakest in Latvia, Luxembourg and Portugal.

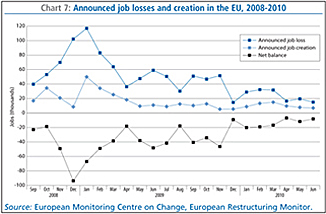

The evolution in firms’ labour demand during the crisis is also reflected in the European Restructuring Monitor (ERM) data collected by the European Monitoring Centre on Change (Chart 7). This clearly shows that from September 2008 onwards, when the crisis heightened, job losses announced by firms strongly outnumbered announced job gains, and that announced job creation has fallen to very low levels over most of 2009 and the first half of 2010. Indeed, there have been almost three times as many announced job losses as job gains in ERM restructuring cases since September 2008. However, since the end of last year there has been a sharp fall in announced job losses, although they still continue to outnumber job gains. In each month since April 2010, total announced job losses have been around a seventh of the peak level reached in January 2009.

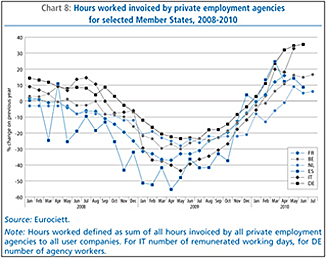

Focusing on particular types of employment, temporary agency work has been hit particularly hard by the downturn, as reflected in data from Eurociett (Chart 8). This shows a sharp year-on-year contraction in the number of hours invoiced by private employment agencies between autumn 2008 and spring 2009. By April 2009 the size of this year-on-year contraction ranged from the order of 20-30% in Belgium, Germany and the Netherlands, around 40% in France and Italy, to over 50% in Spain. Nevertheless, post mid-2009 there has been a strong recovery in workplace activity through temporary work agencies, a leading indicator of a recovery in the labour market. By early 2010 the number of hours invoiced by private employment agencies was returning to levels above those observed a year earlier in most countries, and this strong recovery has generally continued into the first half of 2010.

Despite the clear downward adjustment in the demand for new workers during the crisis, it appears that many firms were reluctant to reduce the number of existing employees even when the demand for their output fell. Manpower Employment Outlook Surveys(7) consistently indicated that the majority of employers reported they intended to make no changes in their staffing levels, which was a reflection of employers’ concern of losing skilled workers who would be hard to replace. The Manpower Employment Outlook Survey for the second quarter of 2010 reported that, while firms’ expectations of firings had decreased, intentions to take on more staff remained broadly flat across EU countries. This stagnation in hiring in part reflects the fact that reduced working hours in Europe have led to widespread underemployment, with the existing workforce likely to absorb increased demand through a rise in working hours before any major increase in staff levels takes place.

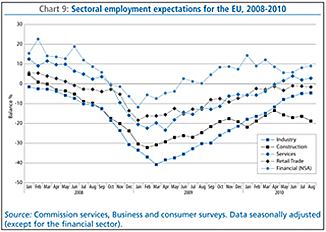

The still weak situation on the demand side is confirmed by

European Commission business and consumer surveys, and is expected to

continue

for some time. Although firms’ employment expectations have

shown a substantial improvement across all main sectors since the lows

recorded in early 2009, they still remain negative on balance other

than in the case of services and the financial sector

(Chart 9).

Employment expectations have shown the greatest relative improvement in

manufacturing, and along with those in the retail sector are now

approaching a zero net balance, although more recently progress has

been sluggish. Furthermore, although expectations in services have been

positive since May, the balance remains subdued, while the jobs outlook

in the construction sector still remains decidedly pessimistic.

| (7) | For more information see the website: www.manpower.com/press/meos.cfm |