Update on steps in building the EU-Bond market infrastructure

date: 25/06/2024

Since 2020, EU Bond issuances have mobilized more than €480 billion for key EU priorities. Demands will remain high in the foreseeable future as NGEU funding is supplemented by additional needs under the Ukraine facility, the new Reform and Growth Facility for the Western Balkans and additional Macro-Financial Assistance (MFA) loan programmes.

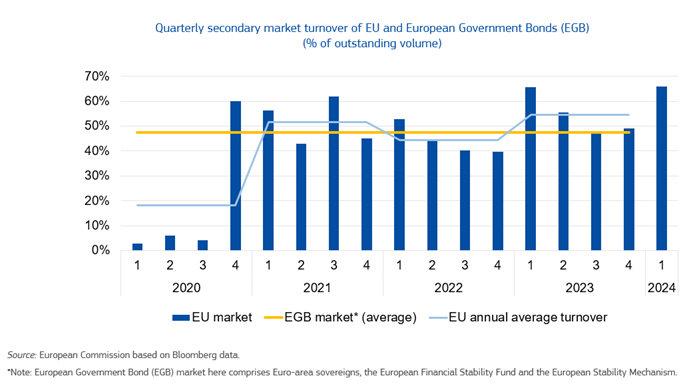

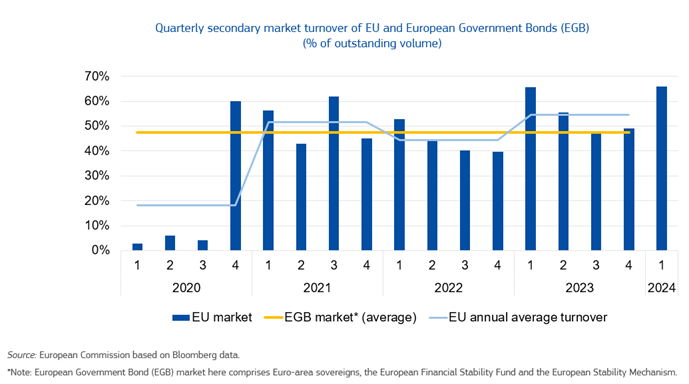

The development of the EU debt capacity infrastructure and of the liquidity of EU Bonds in the secondary market remains a Commission priority. The liquidity of EU Bonds was already bolstered by the move in January 2023 to issue single branded “EU-Bonds”, rather than separately denominated bonds for individual programmes such as NGEU and MFA. A further lift has been the introduction of the quoting arrangements in November 2023. With 25 EU primary dealers posting reliable EU-Bond prices on the leading electronic bond trading platforms, daily turnover volumes average €810 million, with a maximum of €2.6 billion traded on a single day. As a result, the average secondary market liquidity of EU bonds exceeds since early 2023 the average liquidity of EGB issuers.

Work is also advancing on the introduction of a repo facility early in the autumn, with more details to come in our next quarterly update. Through the repo facility, the Commission will make its securities available on a temporary basis to Primary Dealers who cannot source specific EU-Bonds in order to meet commitments to counterparties. This will help Primary Dealers to continue to support the programme by posting prices in EU-Bonds under our new quoting arrangements.

However, despite the strides already made, some market conventions and practices have not kept pace with the sudden transformation in the new status of EU’s issuance. Amongst these are the changes needed to internal investment policies, risk policies and agreements to recognise EU-Bonds as eligible collateral; and the continued classification of the EU as a Supranational Agency for the purposes of bond index classification.

The Commission continues to monitor closely these developments, with the aim of enhancing the market for EU bonds in order to obtain the most advantageous financial conditions in the medium to long run for the benefit of the EU.