Foreign Direct Investment (FDI) encompasses all kind of cross-border investment made by an entity resident in one economy (direct investor) to acquire a lasting interest in an enterprise operating in another economy (direct investment enterprise). FDI is one of the five main functional categories of investment used in international accounts to classify either the International Investment Positions (IIP) or the Balance of Payments (BOP) statements of a given economy (vis-à-vis the rest of the world).

Foreign Direct Investment positions at a point in time (generally, end of a reference year) show the value of financial direct investment assets of residents of an economy on non-residents, and financial direct investment liabilities of residents of an economy to non-residents. The net FDI position is the difference between assets and liabilities, which is also equivalent (under the directional principle presentation) to the difference between FDI positions abroad and in the reporting economy. The net FDI position represents either a net FDI claim or a net FDI liability to the rest of the world.

Foreign direct investment transactions summarize all economic direct investment interactions between the residents and the non-residents during a given period. Two types of FDI transactions can be identified (within the BOP framework) according to the economic meaning they convey:

- FDI income is a distributive transaction showing amounts payable and receivable between resident and non-resident entities in return for providing financial direct investment assets to the rest of the world or incurring direct investment liabilities vis-à-vis the rest of the world.

- FDI flows refer to financial transactions showing the net acquisition or disposal of financial assets and liabilities involved in direct investment relationships.

FDI positions, FDI income, and FDI flows are disseminated by Eurostat together with estimated EU FDI aggregates (directly produced by Eurostat). Other FDI changes that are not transaction changes, such as volume, value or prices changes, are not treated by Eurostat under the scope of annual FDI statistics.

Annual FDI data are disseminated by Eurostat according to the directional principle (see subsection 3.4 below).

The geographical allocation is made according to the economic residence of the immediate direct investor or immediate direct investment company (immediate counterparts). FDI data classified according to the ultimate investor are also available (see 12.1).

International Guides recommend the classification of FDI data both according to the activity of the direct investor and the activity of the direct investment enterprise. In practice, it is very difficult for national compilers to have both classifications. In that case, the recommended classification by activity is that of the direct investment enterprise. On the outward side, national compilers are not always able to classify their FDI data according to the activity of the direct investment enterprise. In that case, the classification used as a proxy is the activity of the direct investor.

Alongside International Trade in Services Statistics (ITSS) and Foreign Affiliates Statistics (FATS), FDI data are relevant to monitor the overall effectiveness and competitiveness of different economies in the globalised world.

11 November 2025

(Main definitions and concepts derived from either IMF BPM6 or OECD BD4 Manuals )

Direct Investment arises when an investor resident in one economy makes an investment that gives control or a significant degree of influence over the management of an enterprise resident in another economy. Direct Investment is one of the five main functional categories of investment used in international accounts to classify financial transactions, positions and primary income. Therefore, this category encompasses all kinds of cross-border investment made by an entity resident in one economy (direct investor) to acquire a lasting interest in an enterprise operating in another economy (direct investment enterprise). In practice, the lasting interest is deemed to exist through either immediate or indirect relationships. Once a direct investment relationship is established, most flows and positions between the entities, including loans and trade credit, are classified as direct investment. The only financial flows and positions excluded from FDI statistics are:

- Debt between selected affiliated financial corporations.

- Financial derivatives.

Immediate direct investment relationship arises when a direct investor directly owns at least 10% of the voting power in a direct investment enterprise.

Indirect relationships arise when a direct investor indirectly owns a direct investment enterprise, either through a chain of control (i.e. ownership > 50% at each stage) or a chain of control ending with an influence of at least 10% of the voting power of the direct investment enterprise.

A direct investor (DI) is an entity or group of related entities able to exercise control or a significant degree of influence over another entity resident in a different economy. A direct investor can be an individual, a group of related individuals, an enterprise (incorporated or unincorporated, private or public), a group of related enterprises, a government body, an estate, a trust or other societal organisation, or any combination of the above.

A direct investment enterprise (DIE) is an entity subject to control or a significant degree of influence by a direct investor. A direct investment enterprise may be an incorporated enterprise (subsidiary or associate) or an unincorporated enterprise (branch).

A subsidiary is a direct investment enterprise over which the direct investor is able to exercise control (ownership > 50%).

An associate is a direct investment enterprise over which the direct investor is able to exercise a significant degree of influence (ownership > 10%) but not control (ownership ≤ 50%).

Fellow enterprises are enterprises that do not have sufficient or any voting power in each other to establish a significant degree of influence but have a common parent. An enterprise is a fellow enterprise of another if both have the same immediate or indirect direct investor, but neither is an immediate or indirect direct investor in the other.

The Framework for Direct Investment Relationships (FDIR) reflects the general approach (as suggested by international guidelines) for identifying and determining the direct investment relationships and, therefore, allows compilers to determine the population of direct investors and direct investment enterprises to be included in their FDI statistics.

Affiliates of an enterprise consist of its immediate or indirect direct investor(s), its immediate or indirect direct investment enterprise(s) (subsidiaries, associates, subsidiaries of associates) and its fellow enterprise(s).

Reverse investment arises when a direct investment enterprise acquires equity in its immediate or indirect direct investor, provided that it does not own more than 10% of the voting power in the direct investor (otherwise the direct investment enterprise wouldalso become a direct investor), or when a direct investment enterprise lends funds to its immediate or indirect direct investor. Under the directional principle presentation (see below), a reverse investment relates either to a liability under direct investment abroad or an asset under direct investment in the reporting economy and is thus always seen as a withdrawal of the FDI capital initially invested by the direct investor in its direct investment enterprise.

(Two different presentations of FDI statistics: asset / liability versus directional principle)

As a reminder, direct investment statistics encompass three distinct statistical accounts, namely FDI positions recorded in the International Investment Positions (IIP) statements, FDI flows recorded in the financial section of the Balance of Payments accounts, and FDI income, which is part of the primary income of the Balance of Payments accounts. Direct investment flows and positions data can be presented according to either the asset/liability or the directional principle.

Asset/liability principle: Allocates the BOP/IIP data according to whether the investment relates to an asset or a liability. This is the official standard presentation recommended by the IMF for all Balance of Payments (BOP) and International Investment Position (IIP) financial account statements, as well as by both IMF BPM6 and OECD BD4 manuals regarding the specific compilation of FDI statistics. This presentation is appropriate for macroeconomic analyses combining the five functional categories of investment used in the international accounts to classify international investment (direct investment, portfolio investment, other investment, financial derivatives and reserve assets).

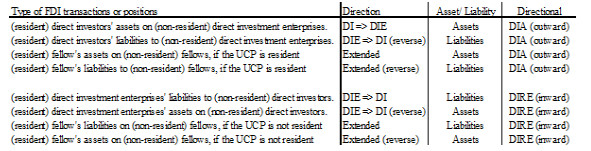

Directional principle: Organises the FDI data according to the direction of the direct investment relationship (or according to the status of the resident entity), either abroad or in the reporting economy. FDI data are classified under:

- Direct investment abroad (DIA) when the resident entity is the direct investor and the non-resident entity is the direct investment enterprise.

- Direct investment in the reporting economy (DIRE) when the resident entity is the direct investment enterprise and the non-resident entity is the direct investor.

The directional principle has been extended to FDI data between fellows depending on whether the residence of the Ultimate Controlling Parent (UCP) is located in the compiling economy. FDI data between two resident/non-resident fellow enterprises are classified under DIA if the UCP is also resident in the compiling economy, and under DIRE if the UCP is not resident in the compiling economy. In cases where the UCP is unknown, the IMF recommends classifying the FDI assets between fellows under DIA and the FDI liabilities between fellows under DIRE.

The directional principle is more appropriate for studying the nature and motivations of foreign direct investment, for identifying the "origin" of direct investment made in a specific country, or for assessing the access of FDI capital to specific markets. The specific treatment of reverse transactions (see below) avoids overestimation of FDI totals and therefore provides a more realistic view of the intensity of the DI-DIE links between two economies. For this reason, the directional principle is widely used for analytical purposes and international comparison. Both the IMF and OECD recommend this presentation when compiling detailed FDI statistics by country or by activity.

Eurostat uses the directional principle for the compilation and dissemination of EU FDI aggregates. Differences between the two presentations arise from differences in the treatment of reverse investments and fellow enterprises. Under the directional principle:

- Reverse investments are treated as withdrawals of capital initially invested, therefore deducted from the net outward or net inward totals.

- Transactions or positions involving fellow enterprises are classified according to the location of their common UCP.

The following table shows the classification of the different types of FDI data for each presentation:

Regardless of the selected presentation, the "net assets – net liabilities" total equals the "net outward – net inward" one.

Special Purpose Entities (SPEs) relate to flexible corporate structures with little or no physical presence and impact in the resident (host) economy. There is no internationally standard definition for these legal structures created by their (non-resident) parent enterprises but also acting as direct investors. The OECD Benchmark Definition (Box 6.2 p 102) offers five general criteria to assist national compilers in identifying SPEs: A SPE is a 1) a legal entity, 2) ultimately controlled by a non-resident parent, 3) having no or few employees, little or no production in the host economy and little or no physical presence, 4) managing mainly external assets or liabilities and 5) acting mainly as a group financing, a conduit or a holding company. SPEs, holding companies or financial institutions serving other non-financial affiliates are particularly involved with the so-called "Funds in transit". The incorporation of SPEs is often associated with off-shore financial centres but they may also be found in other jurisdictions. Eurostat publishes also separate FDI data for SPEs.

Funds in transit (or pass-through funds) relate to funds that pass-through an enterprise resident in one economy to an affiliate in another economy without staying in the economy of that enterprise. Even if they do not correspond to debt between selected affiliated financial corporations and if they have little impact on the resident economy, they must be included in direct investment statistics (to promote symmetry and consistency among economies and keep coherence between FDI flows and positions aggregates). Compilers in economies that have large values of pass-through funds are encouraged to compile supplementary data.

(FDI positions components)

FDI positions provide information on the total stock of investment (abroad and in the reporting economy) for a given reference date which is generally the end of the year. FDI positions data are useful for structural analysis of investment in the host economy, or investment in the investing (home) country, especially to establish the relative FDI importance or presence of one economy in another one. FDI positions data can be broken down by type of instrument: either equity or debt.

Equity positions cover all components of shareholders' funds, proportionate to the percentage of shares held. They include equity, contributed surplus, reinvestment of earnings, revaluations as well as any reserve accounts. Reinvestment of earnings applies only between a direct investor and a direct investment enterprise, therefore fellow enterprises are not concerned by this type of instrument. The recommended principle for the valuation of equity positions is market valuation. Listed equity provides a good basis for the valuation of equity positions at market prices. For unlisted equity an approximation to market prices is necessary and the international guidelines (OECD BD4 and IMF BPM6) offer some flexibility for national compilers in choosing the valuation method, the most widespread ones being the "Own fund at book value", "Recent transaction price" or "Net asset value" methods. The latter is recommended especially for the valuation of equity in branches (unincorporated DIEs).

Debt positions cover all payables and receivables between enterprises in a direct investment relationship arising from loans, deposits, debt securities, trade credits, financial leases and non-participating preferred shares. As a reminder, It should be pointed out that:

- Financial derivatives are excluded from direct investment statistics.

- All debts between selected types of affiliated financial corporations are excluded from direct investment statistics.

FDI positions between the beginning and the end of a given year (n) may change either due to transactions that occurred during year n, or due to other valuation changes (exchange rate changes or price valuation changes occurring when trying to value at market prices), or due to other volume changes. A common issue affecting the latter is, for a given economic entity, the reclassification of its portfolio positions (ownership < 10%) to direct investment statistics if, during the year, this entity acquires additional shares "pushing" its ownership above the 10% threshold.

The reconciliation exercise on annual FDI data is not operated (and not asked) by Eurostat, therefore FDI financial transactions and FDI positions are shown separately without the other valuation changes components.

Ultimate investing economy (UIE) is a geographical allocation that determines the location of the ultimate source of control of the stocks of inward FDI for a reporting economy. BD5 manual recommends to compile, on a supplemental basis, inward FDI positions according to the UIE. Data on FDI positions by UIE are reported on voluntary basis and are published on the Eurostat database.

Ultimate controlling parent (UCP) is an entity that ultimately controls an enterprise, identified by proceeding up the ownership chain from the enterprise through the controlling links (ownership of more than 50% of the voting power) until an individual, household, or company that is not controlled by another company is reached. If there is no company, individual, or household that controls the resident company, then the resident company may be considered to be its own ultimate controlling parent.

(FDI flows - financial transactions components)

FDI flows are recorded in the financial account section of the Balance of Payments and relate to direct investment transactions made during the period in the form of equity capital acquisitions, debt transactions (in most cases loans or trade credits between affiliated enterprises) or reinvestment of earnings.

Equity capital comprises equity in branches, all shares in subsidiaries and associates (except non-participating, preferred shares, which are treated as debt securities and included under other FDI capital).

Reinvestment of earnings consists of the direct investor's share (in proportion to equity participation) of earnings not distributed by the direct investment enterprise. Reinvestment of earnings is an imputed transaction of the financial account of the Balance of Payments recorded simultaneously (for the same amount) with the reinvested earnings transaction recorded in the primary income section of the Balance of Payments (see below). The logic underlying this simultaneous recording of two fictive transactions is that one describes the allocation of the company's profits to reserves (reinvestment of earnings in the equity capital of the direct investment enterprise), while the other represents the portion of profits not distributed to shareholders as dividends, and which stays in the accounts of the direct investment enterprise.

Debt transactions cover all transactions between enterprises in a direct investment relationship arising from loans, deposits, debt securities, trade credits, financial leases and non-participating preferred shares. As a reminder, financial derivatives and all debts between selected types of affiliated financial corporations are excluded from direct investment statistics, as are transactions between affiliates in financial assets issued by unrelated parties. The official expression covering all debt transactions between enterprises in a direct investment relationship is "inter-company lending".

(FDI income components)

FDI income are recorded in the primary income section of the Balance of Payments and represents the return accruing to direct investors, during a reference year, for the provision of financial assets. FDI income categories are linked to the breakdown of FDI flows and stocks by type of instrument. It consists of dividends and withdrawals from income of quasi-corporations, reinvested earnings, and interest. Investment income on reverse investment – income receivable from claims on direct investors and income payable on liabilities to direct investment enterprises – is, in principle, shown on a gross basis.

Dividends and withdrawals from income of quasi-corporations

Dividends include dividends payable or receivable in the period gross of any withholding taxes. Dividends cover payments due on common and preferred shares. The BPM6 methodology introduced the concept of superdividends which relates to exceptional payments by corporations to their shareholders made out of accumulated reserves, disproportionately large compared to recent level of dividends and earnings. Superdividends are excluded from FDI income statistics because they are considered as withdrawals of equity. Liquidating dividends, which arise mainly at the time of company termination are also excluded from the income statistics, therefore also treated as withdrawals of equity. In practice, three dates can be associated with dividends: the date when they are declared, the date when they are excluded from the market price of shares (known as the ex-dividend date) and the date when they are paid. Dividends must be recorded at the time the shares go ex-dividend.

Withdrawals from income of quasi-corporations mainly relate to distributed branch profits. In legal terms, quasi-corporations cannot distribute income in the form of dividends but, in practice, the owner(s) of a quasi-corporation may formally distribute part or all of their earnings. From an economic point of view, the withdrawal of such income is equivalent to the distribution of corporate income through dividends and is treated in the same way. Withdrawals from income of quasi-corporations are recorded when they actually take place.

(Transfer pricing) If a direct investment enterprise is over-invoiced for a good or service provided by the direct investor, or if a direct investor is under-invoiced for a good or service provided by the direct investment enterprise, then the transfer pricing acts as a hidden dividend, and an adjustment to increase the dividends (up to market value) should be made in cases of excessive overcharging or under-invoicing. In the opposite situation, the transfer pricing does not act as a dividend but as a hidden investment and, if significant, the equity capital acquisitions component should be increased (up to market value).

Reinvested earnings (See also additional comments in the FDI flows section above). Reinvested earnings are the direct investor's share of the retained earnings of the direct investment enterprises and are attributed to direct investors who are in an immediate direct investment relationship with the direct investment enterprise (i.e. with at least 10% participation). The undistributed earnings of branches are also considered to be reinvested earnings. Formally, the retained earnings (or net saving) of a resident direct investment enterprise (DIE) are equal to:

Net operating surplus

+ Dividends receivable + Interest receivable + Rent receivable

+ Enterprise's share of reinvested earnings coming from any other (non-resident) DIE(s)

+ Current transfer receivable

- Dividends payable - Interest payable - Rent payable

- Taxes and other current transfer payable

Reinvested earnings do not include any realised or unrealised holding gains or losses, therefore adjustments to business accounting records may be necessary prior to calculation.

Reinvested earnings can also be negative (i.e. recorded with a negative sign) when a DIE incurs a loss on its operations or when the dividends declared in a period exceed the net income generated during the same period.

Within a chain of direct investment relationships, reinvested earnings need only be recorded between the direct investor and directly owned direct investment enterprises, therefore there are no reinvested earnings between fellows and indirectly owned direct investment enterprises.

Interest

Interest (income on debt) is a form of investment income that is receivable by the owners of deposits, debt securities, loans, non-preferred shares and other accounts receivable. Direct investment interest payables on liabilities, and receivables on assets, are recorded separately. Interest is recorded as accruing continuously over time to the creditor on the amount outstanding. Interest on debt accrues continually over the life of the debt and adds to the principal. Thus, actual payments of the debt (as opposed to accruals) are investment transactions, not income and should be recorded in the FDI transactions account. No direct investment interest is recorded when both parties are related financial intermediaries. In principle, interest receivables or payables on reverse loans are shown separately on a gross basis.

For entities acting as direct investors, all institutional units are included - that is, enterprises (incorporated or unincorporated, public or private), individuals or households, investment funds, governments, international organisations, non-profit institutions in an enterprise that operates for profit, estates, or trusts, etc.

A direct investment (or fellow) enterprise is always an incorporated (subsidiary or associate) or an unincorporated enterprise (branch, trust, etc.). Households or governments cannot be direct investment enterprises because they cannot be owned by another entity.

The Framework for Direct Investment Relationships (FDIR) provides criteria for determining whether cross-border ownership results in a direct investment relationship based on control (≥ 50%) or a significant degree of influence (≥ 10%). Control or influence may be achieved directly or indirectly. The principles for indirect transmission of control and influence through a chain of ownership are as follows:

- Control can be passed down a chain of ownership as long as control exists at each stage.

- Influence can be generated at any point down a chain of control.

- Influence can be passed only through a chain of control but not beyond.

Under the FDIR, the statistical population is defined as composed of all direct investors, all direct investment enterprises and all fellow enterprises.

Reporters to Eurostat are the individual EU27 Member States, Iceland, Norway, Switzerland, North Macedonia, Montenegro, Serbia, Turkey, Albania and Kosovo*.

The EU27 aggregate, as a whole reporting entity, is directly estimated by Eurostat on the basis of FDI data received from the 27 Member States.

US FDI data are extracted from the Organisation for Economic Cooperation and Development (OECD) online database. A few adjustments are made by Eurostat both on geographical and activity breakdowns, to align with Eurostat’s requirements for EU countries - mostly filtering only the required codes. The data are then converted into millions of euros. Caution should be taken, as the direct investment data with geographical and activity breakdowns published by the US Bureau of Economic Analysis (BEA) are valued at historical cost, without current-cost adjustment. This differs from the recommended market value.

JP FDI data are extracted from the Organisation for Economic Cooperation and Development (OECD) online database. A few adjustments are made by Eurostat both on geographical and activity breakdowns to align with Eurostat’s requirements for EU countries - mostly filtering only the required codes. The data are then converted into millions of euros.

Prior any dissemination:

- FDI flows and income datasets (year n) that are not transmitted to Eurostat in euros are converted using the yearly average exchange rates (year n) between the euro and corresponding national currencies.

- FDI positions datasets at end of year n that are not transmitted to Eurostat in euros are converted using the exchange rates between the euro and corresponding national currencies observed at end of year n.

* This designation is without prejudice to positions on status, and is in line with UNSCR 1244/1999 and the ICJ Opinion on the Kosovo declaration of independence.

FDI stocks refer to the end of the recording period; flows and income refer to the recording period. All FDI data are annual.

FDI data transmitted to Eurostat are checked for their consistency and plausibility. If any problems (e.g. inconsistencies or omissions) are detected, Eurostat contacts the relevant national compiler to re-validate the figures and/or confirm correction/updates implemented by Eurostat. This is made through the validation procedure established by Eurostat vis-à-vis all individual countries to ensure the quality of the data reported.

Within this procedure integrity rules defined in the FDI section of the Vademecum are applied on all original datasets. Furthermore, consistency with historical data and consistency with values reported at national level are also scrutinised by Eurostat together with the availability of revised information reported to Eurostat.

EU mirror analysis is another way of assessing the accuracy of FDI statistics: values (outward/inward) reported by Member States are compared with those of their partners (inward/outward) within the EU. Theoretically, taking the EU as a whole reporting entity, the sum of intra-EU outward financial flows (or income or positions) should match with the sum of intra-EU inward financial flows (income or positions). In practise, such a situation occurs very rarely, and the resulting differences are evaluated in asymmetry analysis. Intra-EU asymmetries are more important on transactions (flows and income) due to their high volatility, by nature, when compared to positions.

There are several reasons that might explain intra-EU asymmetries, for example, wrong geographical data allocation by one or both counterparts, different amounts recorded on both sides, misclassification by functional financial category (direct versus portfolio investment), different accounting support and/or method(s), different framework for direct investment relationship (FDIR), different methods for the valuation of unlisted equities etc.

Eurostat, together with other International Organisations (mainly OECD, ECB and IMF) is actively participating to international working group aiming at reducing the intra-EU and bilateral asymmetries through reinforcing the harmonisation of FDI compilation methods. To this aim, Eurostat is also handling a FDI Network to allow bilateral microdata exchanges both on FDI positions and transactions.

FDI flows, income and position data are presented in millions of Euro.

The table showing impact indicators, rate of return on FDI and FDI as share of GDP is in percentage.

Aggregate data for the European Union are in general obtained as the sum of the respective Member States data. Member States data are in some cases confidential and therefore are not shown in datasets or tables published on Eurostat website.

EU FDI data are collected by Member States Balance of Payments compilers through a variety of sources. The main types of sources used are direct surveys addressed to resident statistical units and reports by the central banking systems on international transactions.

Annual FDI data shall be transmitted by Member States to Eurostat at T+9 months for detailed partner country breakdown (i.e. end September), and T+21 months for detailed partner country and activity breakdowns (as required by the EC Regulation 184/2005).

The current Eurostat's practice is to compile the EU aggregates based on the official FDI annual datasets provided by national compilers, and to disseminate both EU aggregates and Member States annual figures between T+11 and T+12 months (by mid-December). Processing time is required for validation of the data transmitted and tasks to compile the aggregates including the work to secure the confidential data in the data release.

Annual FDI data are released in 11-12 months after the end of the reference period (by mid-December).

The underlying methodological framework, which is defined in BPM6, ensures a high degree of comparability across countries. Regulation (EU) No 555/2012 contains the data requirements, the details on the coding system, the format of the data and the deadlines for transmission. Each country compiles their FDI statistics using the data coming from several surveys and administrative sources.

The data comparability over time is restricted. Eurostat began its new FDI annual time series collection from 2013 reference year therefore introducing a break in the data prior and from 2013. For extra EU FDI totals, however, FDI data according to the new methodology and the directional principle presentation can be estimated for reference years prior to 2013 using the quarterly FDI series.