4. A Digital Europe

4.2 The changing 'DNA' of innovation

Digitalisation is transforming every aspect of daily life, including innovation. The new changing dynamics of innovation can be defined by ‘5Cs’: celerity, complexity, concentration, costs and consumers.

Digitalisation is transforming every aspect of our world, including the ‘DNA’ of innovation.

The five main characteristics of the changing dynamics of innovation in the age of digital transformation are celerity, complexity, concentration, costs and consumers.

Celerity - the speed of technology adoption

Technology, and notably consumer-driven innovation, is spreading faster than ever due to the transition from physical to digital goods combined with strong social network effects in the age of digital transformation.

It took longer for potentially all households to have a telephone at home, own a car and a dishwasher, or have electricity than to use the internet and even less time to use a smartphone or engage on social media channels.

This is in contrast to the apparent lack of diffusion of productivity-enhancing technologies across sectors and firms.

Quantum computing has the potential to solve highly complex problems in less time than classical computers, which could speed up scientific discoveries and predictions in the future.

Complexity - the rise of deep-tech, science-based innovations

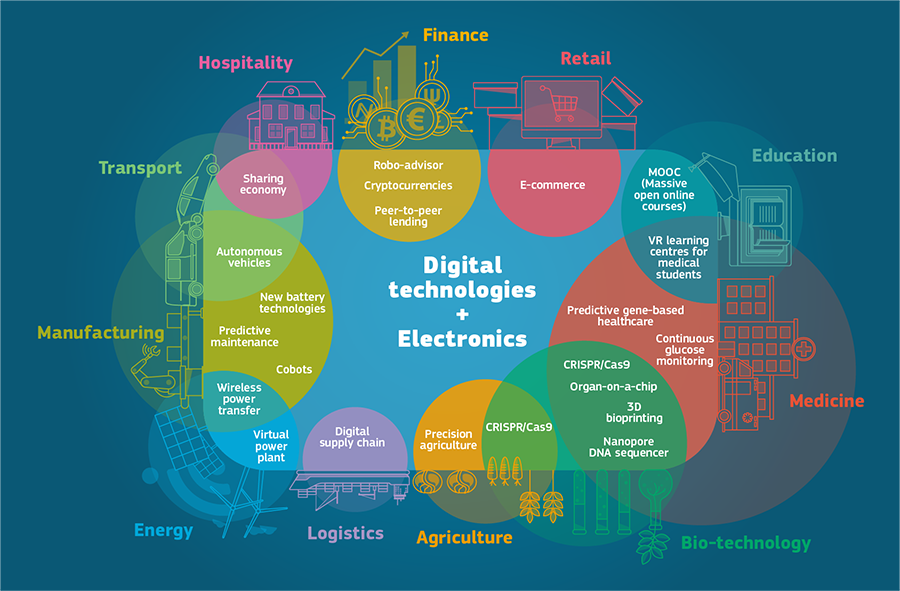

Innovations are increasingly the result of the convergence between digital technologies and scientific fields leading to ‘deep-tech innovations’. These include digital supply chains, precision agriculture, 3D bioprinting, and autonomous vehicles, among many others across sectors.

To reap the full benefits of these deep-tech innovations, companies must have an organisational structure that enables the agility and flexibility required by teams to master different technologies and new business models, strategic management, staff training, and branding.

Deep-tech, science-driven innovations require ‘patient capital’ to overcome the greater uncertainty and the longer time span necessary to make them commercially viable.

Concentration – in industry, R&D and scientific outputs

Industry concentration is a rising phenomenon in North America and to a less extent in Europe, not confined exclusively to digital-intensive sectors. This can also be observed by the rise in average mark-ups over time.

Concentration can also be observed when it comes to scientific publications and innovation outputs by the top R&D investors, both at the global and EU level.

Companies with greater access to data have a competitive advantage in the digital era to gain market shares, especially at a time when innovation is more and more ‘customer-centric’ and enabling product differentiation. However, access to data should respect privacy and the ethical use of data. The EU’s General Data Protection Regulation (GDPR) provides guidance on its fair use.

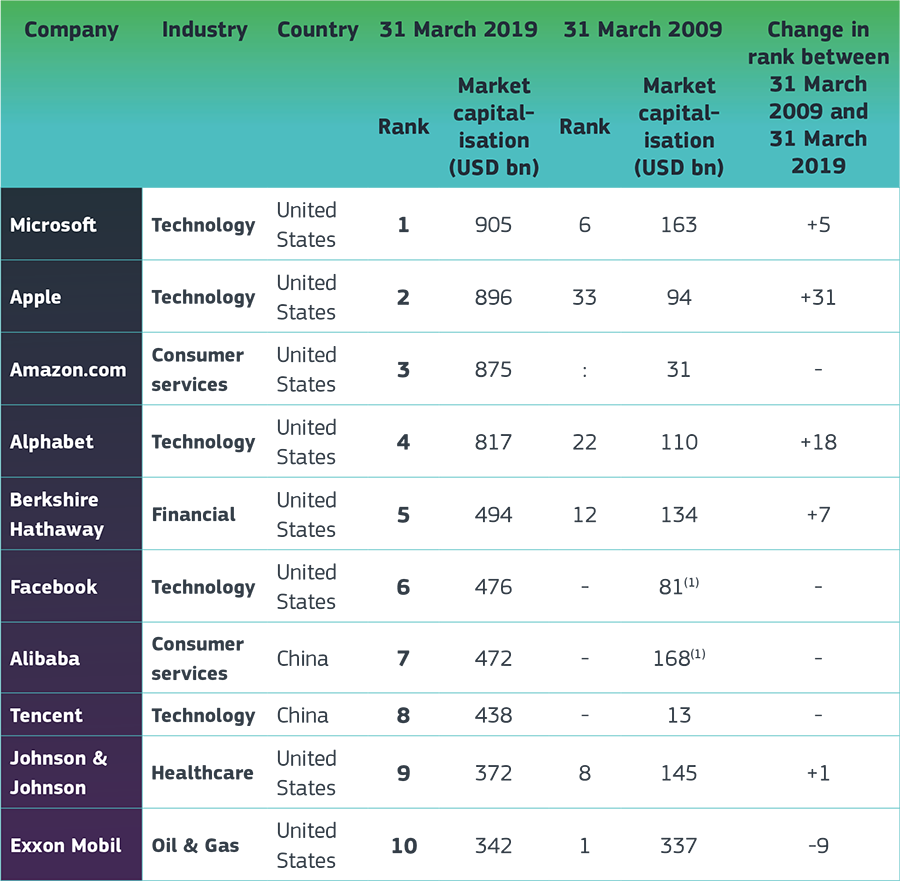

The dominance of US tech giants is not only visible in terms of market capitalisation and R&D investment, but also when it comes to some of the pillars underpinning digitalisation, such as search engines, operating systems and cloud infrastructure.

Costs – towards a paradigm of ‘zero marginal costs’ in the digital age

The biggest transformation created by digitalisation concerns the ‘move from atoms to bytes’.

While the R&D investments required to produce deep-tech innovations can prove costly, companies that sell digital products can manage to operate under close to zero marginal costs. This mirrors the diminishing importance of tangible capital in the digital age.

Digital products and services have the inherent economic properties of non-rivalry and of being infinitely expandable — they can be accessed simultaneously by different users an infinite number of times, at no cost.

Consumers – driving innovation and change in organisations

Consumers are no longer mere users of new technologies; they are driving innovations. They are also increasingly putting pressure on companies to become more environmentally friendly, with younger generations leading this push for change in organisations.Corporate responsibility should include four areas — social, economic, technological, and environmental.

Business-model innovation contributes to capturing greater value from new goods and services. In particular, various digital business models have emerged to benefit from the new opportunities created by the digital age.

The widespread use of smartphones and other tech gadgets has enabled the availability of free digital goods in a single device while making many physical (and paid) goods obsolete.

Note: iTunes: number of accounts; WhatsApp: active users; Instagram: monthly users; Candy Crush Saga; Pokémon GO: number of downloads; Twitter: active users.

The rise of deep-tech science-based innovations

Note: The countries for Europe include BE, DE, DK, EE, ES, FI, FR, GB, GR, HU, IE, IT, LV, NL, NO, PL, PT, SI, SE, and for North America include CA and US. Included industries cover 2-digit manufacturing and non-financial market services. Concentration metrics reflect the share of the top 8 firms in each industry (CR8). The graphs can be interpreted as the cumulated absolute changes in levels of sales concentration for the mean 2-digit sector within each region. For instance, in 2014, the mean European services industry’s sales concentration was 4 percentage points higher than in 2000.

Notes: Data refers to the top 1 000 R&D investors in the EU28. There are a few missing values for companies regarding employment and net sales.

Top 10 global companies by market capitalisation, 2009 and 2019

Note: (1)Market capitalisation at IPO date.