CHAPTER 20

THE GOVERNMENT ACCOUNTS

INTRODUCTION

- to provide goods and services to the community, either for collective consumption such as public administration, defence, and law enforcement, or individual consumption such as education, health, recreation and cultural services, and to finance their provision out of taxation or other incomes;

- to redistribute income and wealth by means of transfer payments such as taxes and social benefits;

- to engage in other types of non-market production.

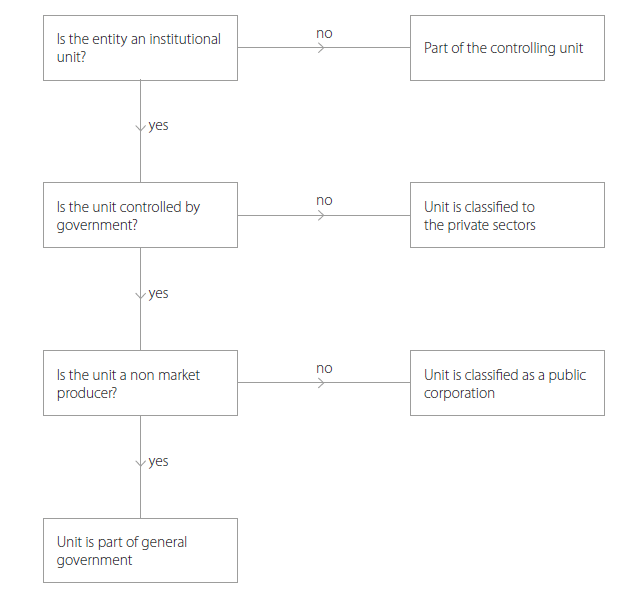

DEFINING THE GENERAL GOVERNMENT SECTOR

Identification of units in the government

Government units

NPIs classified to the general government sector

- the appointment of officers;

- other provisions of the enabling instrument, such as the obligations in the statute of the NPI;

- contractual agreements;

- degree of financing;

- risk exposure.

Other units of general government

Public control

Market/non-market delineation

Notion of economically significant prices

Criteria of the purchaser of the output of a public producer

The output is sold primarily to corporations and households

- the producer has an incentive to adjust supply either with the goal of making a profit in the long run or, at a minimum, covering capital and other production costs, including consumption of fixed capital, by sales; and

- consumers are free to choose on the basis of the prices charged.

The output is sold only to government

The output is sold to government and others

The market/non-market test

- the producer is an institutional unit (a necessary condition; see also the decision tree in paragraph 20.17);

- the producer is not a dedicated provider of ancillary services;

- the producer is not the only supplier of goods and services to government, or, where that producer is, it has competitors; and

- the producer has an incentive to adjust supply to undertake a viable profit-making activity, to be able to operate in market conditions and to meet its financial obligations.

Financial intermediation and the government boundary

Borderline cases

Public head offices

- To the extent that the public head office is an institutional unit and is engaged in the management of market producers, it is classified according to the main activity of the group, in sector S.11 if the main activity is to produce goods and non-financial services, or in sector S.12 if it produces mainly financial services (see also paragraphs 2.23 and 2.59).

- If the public head office is not an institutional unit, and so sometimes known as a 'shell', or acts as a government agent for public policy purposes, such as channelling funds amongst subsidiaries, and organising privatisation or defeasance, it is classified to the general government sector.

Pension funds

Quasi-corporations

- it charges prices for its outputs that are economically significant;

- it is deemed to have autonomy of decision; and

- a complete set of accounts exists that enables its operating balances, savings, assets and liabilities to be separately identified and measured, or it is possible to construct such a complete set of accounts.

Restructuring agencies

Privatisation agencies

- The restructuring unit, whatever its legal status, acts as a direct agent of the government or has a limited lifespan. Its main function is to redistribute national income and wealth, channelling funds from one unit to the other. The restructuring unit is classified in the general government sector.

- The restructuring unit is a holding company controlling and managing a group of subsidiaries, and only a minor part of its activity is dedicated to conducting privatisation and channelling funds from one subsidiary to the other on behalf of the government and for public policy purposes. The unit is classified as a corporation, and any transactions made on behalf of the government should be rerouted through the general government.

Defeasances structures

Special purpose entities

Joint ventures

Market regulatory agencies

- either to buy, hold and sell agricultural and other food products on the market; or

- to be exclusively or principally a distributor of subsidies or other transfers to producers.

Supranational authorities

The subsectors of general government

Central government

State government

Local government

Social security funds

THE GOVERNMENT FINANCE PRESENTATION OF STATISTICS

Framework

|

Government finance statistics presentation |

|

|

less |

Revenue Taxes Social contributions Sales of goods and services Other current revenue Capital transfer revenue Expenditure Intermediate consumption Compensation of employees Interest Subsidies Social benefits Other current expenditure Capital transfer expenditure Investment expenditure |

|

equals |

Net lending/net borrowing |

|

equals |

Net financial transactions |

| N.A. |

opening balance sheet |

|

plus |

transactions |

|

plus |

revaluations |

|

plus |

other changes in volume |

|

equals |

closing balance sheet |

Revenue

|

Total revenue |

= |

total taxes |

D.2 + D.5 + D.91 |

|

| N.A. |

+ |

total social contributions |

D.61 |

|

|

+ |

total sales of goods and services |

P.11 + P.12 + P.131 |

||

|

+ |

other current revenue |

D.39 + D.4 + D.7 |

||

|

+ |

other capital revenue |

D.92 + D.99 |

||

Taxes and social contributions

Sales

- the market output of market establishments included in government, such as a weapons factory that is part of the ministry of defence, or canteens set up by government units for their employees, that charge economically significant prices;

- secondary market products sold by non-market establishments, sometimes referred to as 'incidental sales', such as those arising from research and development contracts between public universities and corporations, or publications sold by government units at economically significant prices.

| N.A. |

ESA resources |

ESA GFS revenue |

|---|---|---|

|

P.1 |

Output, of which |

N.A. |

| N.A. |

Market output (P.11) |

Sales of goods and services |

| N.A. |

Output for own final use (P.12) |

Sales of goods and services |

| N.A. |

Non-market output (P.13), of which: |

N.A. |

| N.A. |

- Payments for non-market output (P.131) |

Sales of goods and services |

| N.A. |

- Non-market output, other (P.132) |

Not accounted for in Total revenue |

|

D.2 |

Taxes on production and imports (receivable) |

Total taxes |

|

D.3 |

Subsidies (receivable) |

Other current revenue |

|

D.4 |

Property income |

Other current revenue |

|

D.5 |

Current taxes on income and wealth |

Total taxes |

|

D.61 |

Social contributions |

Total social contributions |

|

D.7 |

Other current transfers |

Other current revenue |

|

D.91r |

Capital taxes (receivable) |

Total taxes |

|

D.92r |

Investment grants (receivable) |

Other capital revenue |

|

D.99r |

Other capital transfers (receivable) |

Other capital revenue |

| N.A. | ||

| N.A. |

ESA uses and capital transactions |

ESA GFS expenditure |

|

P.2 |

Intermediate consumption |

Intermediate consumption |

|

D.1 |

Compensation of employees |

Compensation of employees |

|

D.2 |

Taxes on production and imports (payable) |

Other current expenditure |

|

D.3 |

Subsidies (payable) |

Subsidies |

|

D.41 |

Interest |

Interest |

|

D.4 |

Property income (excluding D.41) |

Other current expenditure |

|

D.5 |

Current taxes on income |

Other current expenditure |

|

D.62 |

Social benefits other than social transfers in kind |

Social benefits other than ST in kind |

|

D.632 |

Social transfers in kind via market producers |

Social transfers in kind via market producers |

|

D.7 |

Other current transfers |

Other current expenditure |

|

D.8 |

Adjustment for the change in pension entitlements |

Other current expenditure |

|

P.31 |

Individual consumption expenditure on market output |

Social transfers in kind via market producers |

|

P.31 |

Individual consumption expenditure on non-market output |

Not accounted for in Total expenditure |

|

P.32 |

Collective consumption expenditure |

Not accounted for in Total expenditure |

|

P.5 |

Gross capital formation |

Capital expenditure |

|

NP |

Acquisition less disposal of non-produced assets |

Capital expenditure |

|

D.92p |

Investment grant (payable) |

Capital expenditure |

|

D.99p |

Other capital transfers (payable) |

Capital expenditure |

- on the resources side, the non-market output, other (P.132) recorded in the production account;

- on the uses side, the actual final consumption (P.4) and the social transfers in kind - non-market production (D.631). They are recorded in the redistribution of income in kind account, and in the use of adjusted disposable income account.

Other revenue

Expenditure

|

Total expenditure |

= |

intermediate consumption |

P.2 |

|

| N.A. |

+ |

compensation of employees |

D.1 |

|

|

+ |

interest |

D.41 |

||

|

+ |

social benefits other than social transfers in kind |

D.62 |

||

|

+ |

social transfers in kind via market producers |

D.632 |

||

|

+ |

subsidies |

D.3 |

||

|

+ |

other current expenditure |

D.29 + (D.4 - D.41) + D.5 + D.7 + D.8 |

||

|

+ |

capital expenditure |

P.5 + NP + D.92 + D.99 |

||

Compensation of employees and intermediate consumption

Social benefits expenditure

Interest

Other current expenditure

Capital expenditure

Link with government final consumption expenditure (P.3)

|

|

compensation of employees (D.1) |

|

plus |

intermediate consumption (P.2) |

|

plus |

consumption of fixed capital(P.51c1) |

|

plus |

other taxes on production, payable (D.29 U) |

|

less |

other subsidies on production, receivable (D.39 R) |

|

plus |

operating surplus, net (B.2n) |

|

equals |

output (P.1) |

|

|

output |

|

less |

sales of goods and services (P.11+P.12+P.131) |

|

plus |

social transfers in kind via market producers (D.632) |

|

equals |

final consumption expenditure (P.3) |

Government expenditure by function (COFOG)

|

Code |

Function |

Type of service |

|---|---|---|

|

01 |

General public services |

Collective |

|

02 |

Defence |

Collective |

|

03 |

Public order and safety |

Collective |

|

04 |

Economic affairs |

Collective |

|

05 |

Environmental protection |

Collective |

|

06 |

Housing and community amenities |

Collective |

|

07 |

Health |

Mainly individual |

|

08 |

Recreation, culture and religion |

Mainly collective |

|

09 |

Education |

Mainly individual |

|

10 |

Social protection |

Mainly individual |

Balancing items

The net lending/net borrowing (B.9)

Changes in net worth due to saving and capital transfers (B.101)

|

|

Net saving plus capital transfers (B.101) |

|

less |

acquisitions less disposals of non-financial assets (P.5+NP) |

|

plus |

consumption of fixed capital(P.51c1) |

|

equals |

net lending/net borrowing (B.9) |

|

equals |

transactions in financial assets less liabilities (financing) |

Financing

Transactions in assets

- equity injections (generally in the form of cash) to specific public corporations where government is acting as an investor with the expectation of a return on invested funds. Such injections are not considered as government expenditure in national accounts;

- portfolio investments, in the form of purchases of quoted shares on the market made by government units such as asset-rich social security funds, or other portfolio investment operations;

- net investment in mutual funds, which are alternative investment vehicles. In particular, placements in money market mutual funds are reported here, rather than under currency and deposits, despite being close substitutes for bank deposits;

- privatisations conducted by special privatisation agencies, as such entities are classified to general government;

- distributions by public corporations to their owners in excess of their operational profit excluding holding gains/losses, recorded as financial transactions as withdrawal of equity akin to a partial liquidation of the enterprise, rather than as government revenue.

Transactions in liabilities

Other economic flows

Revaluation account

- real estate assets of government;

- equity of government;

- security liabilities.

Other changes in volume of assets account

Balance sheets

|

Net worth |

= |

Total assets |

|

| N.A. | N.A. |

minus |

Total liabilities |

Consolidation

- property income such as interest;

- current and capital transfers;

- transactions in financial assets and liabilities.

- current and capital transfers, such as central governments grants to lower levels of government;

- interest arising on intergovernmental holdings of financial assets and liabilities;

- transactions, other economic flows and stocks in financial assets and liabilities, such as loans to other governments or acquisitions of government securities by social security units.

ACCOUNTING ISSUES RELATING TO GENERAL GOVERNMENT

Tax revenue

Character of tax revenue

Tax credits

Amounts to record

Amounts uncollectible

Time of recording

Accrual recording

Accrual recording of taxes

Interest

Discounted and zero-coupon bonds

Index-linked securities

Financial derivatives

Court decisions

Military expenditure

Relations of general government with public corporations

Equity investment in public corporations and distribution of earnings

Equity investment

- a share of any dividends (or withdrawals of income from quasi-corporations) paid at the choice of the corporation but not to a fixed and predetermined income; and

- a share in the net assets of the corporation in the event of its liquidation

Capital injections

Subsidies and capital injections

- A payment to cover accumulated, exceptional or future losses, or provided for public policy purposes, is recorded as a capital transfer. Exceptional losses are large losses recorded in one accounting period in the business accounts of a corporation, which usually arise from downward revaluations of balance sheet assets, in such a way that the corporation is under threat of financial distress (negative own funds, breach of solvency, etc.).

- A payment where the government is acting as a shareholder in that it has a valid expectation of earning a sufficient rate of return, in the form of dividends or holding gains is an acquisition of equity. The corporation must enjoy a large degree of freedom in how it uses the funds provided. When private investors are part of the capital injection, and the conditions for private and government investors are similar, this is evidence that the payment is likely to be acquisition of equity.

Rules applicable to particular circumstances

Fiscal operations

Public corporations distributions

Dividends versus withdrawal of equity

- the corporation making this payment makes short-period accounts available to the public and the payment is based on at least two quarters;

- the interim payment should be in the same proportion as the dividends paid in the previous years, consistent with the usual rate of return to the shareholder and with the trend in growth of the corporation.

Taxes versus withdrawal of equity

Privatisation and nationalisation

Privatisation

Indirect privatisations

Nationalisation

Transactions with the central bank

- payments made on a regular basis, usually in the form of dividends, based on the current activity of the central bank (like managing foreign exchange reserves). These payments are recorded as dividends as long as they are not higher than a measure of net operating income, consisting of net property income, net of costs and of any transfers. Amounts in excess of this sum are to be recorded as a decrease in equity;

- exceptional payments following the sale or the revaluation of reserve assets. These payments are recorded as a withdrawal of equity. The rationale is that the value of such assets affects the value of the equity liability of the central bank and the equity assets of government. Thus, holding gains on the reserve assets of the central bank have a counterpart in the equity assets of government via the equity liability of the central bank.

Restructures, mergers, and reclassifications

Debt operations

Debt assumptions, debt cancellation and debt write-offs

Debt assumption and cancellation

- An actual pre-existing financial asset is acquired against a third party, as in the case of guaranteed export insurance. Thus, government records, as the counterpart transaction of its new liability, the acquisition of a financial asset equal to the present value of the amount expected to be received. If this amount is equal to the liability assumed, no further entries are required. If the amount expected to be recovered is less than the liability assumed, the government records a capital transfer for the difference between the liability incurred and the value of the asset acquired.

- Government simply records a claim against the benefiting corporation, which is in most cases a public corporation in difficulty. In general, because of the very hypothetical value of this claim, no such claim is recorded. Possible future repayments by the beneficiary will be recorded as revenue by the government.

Debt assumption involving a transfer of non-financial assets

Debt write-offs or write-downs

Other debt restructuring

Purchase of debt above the market value

Defeasances and bailouts

- a government may guarantee certain liabilities of the enterprise to be assisted;

- a government may provide equity financing on exceptionally favourable terms;

- a government may purchase assets from the enterprise to be assisted for prices greater than their true market value;

- a government may create a special purpose entity or other type of public body to finance and/or to manage the sales of assets or liabilities of the enterprise to be assisted.

Debt guarantees

Derivatives-type guarantees

Standardised guarantees

One-off guarantees

Securitisation

Definition

Criteria for sale recognition

Recording of flows

Other issues

Pension obligations

Lump sum payments

Public-private partnerships

Scope of PPP

Economic ownership and allocation of the asset

- construction risk, which includes costs overruns, the possibility of additional costs resulting from late delivery, not meeting specifications or building codes, and environmental and other risks requiring payments to third parties;

- availability risk, which includes the possibility of additional costs such as maintenance and financing, and the incurrence of penalties because the volume or quality of the services do not meet the standards specified in the contract;

- demand risk, which includes the possibility that demand for the services is higher or lower than expected;

- residual value and obsolescence risk, which include the risk that the asset will be less than its expected value at the end of the contract and the degree to which the government has an option to acquire the assets;

- the existence of grantor financing or granting guarantees, or of advantageous termination clauses notably on termination events at the initiative of the operator.

- the degree to which the government determines the design, quality, size, and maintenance of the assets;

- the degree to which the government is able to determine the services produced, the units to which the services are provided, and the prices of the services produced.

Accounting issues

Transactions with international and supranational organisations

-

taxes: some taxes on products, such as import duties and excises, are payable to institutions of the European Union or other supranational organisations. These form three categories:

- those payable directly, such as, in the past, the European Coal and Steel Community levy on mining and iron and steel producing entities, which are recorded directly;

- those collectible by national governments as agents on behalf of the institutions of the European Union or other supranational organisations, but where the tax is judged as payable directly by the resident producers. Examples are levies on imported agricultural products, monetary compensatory amounts levied on imports and exports, sugar production levies and the tax on isoglucose, co-responsibility taxes on milk and cereals, and custom duties levied on the basis of the integrated tariff of the European Communities. Such items are recorded directly from the producers to the supranational organisation, with government's role as an intermediary recorded as a financial transaction;

- receivables of value added tax in each Member State. They are recorded as receivable by national governments, with the amounts that Member States provide to the European Union recorded as a current transfer (D.76). The time of recording of the transfer from government is when it is to be paid;

- subsidies: any subsidies directly payable by supranational organisations to resident producers are recorded as directly payable by the supranational organisation rather than a resident government unit. Subsidies payable to resident producers and channelled through government units as intermediaries are similarly recorded directly between the principal parties, but also create entries in other accounts receivable/payable (F.89) in the government financial accounts;

- miscellaneous current transfers: contributions to the European Union budget from Member States for the third and fourth types of payment designed to give the European Union its own resources. The third resource is calculated by applying a flat rate to the Value Added Tax base of each Member State. The fourth resource is based on the gross national income of each Member State. Such payments are considered to be compulsory transfers from governments to the European Union. They are classified as miscellaneous current transfers and recorded when they are to be paid;

- current international cooperation: most other current transfers, in cash or in kind, between government and non-resident units, including international organisations, are classified as current international cooperation. This includes current aid to developing countries, wages payable to teachers, advisers and other government agents in activity abroad etc. One characteristic of current international cooperation is that it consists of transfers made on a voluntary basis;

- capital transfers: investment grants, in cash or in kind, and other capital transfers, especially as the counterpart transaction of debt cancellation or debt assumption, can be payable to or receivable from an international or supranational organisation;

- financial transactions: some financial transactions, usually loans, may be recorded when granted by international organisations such as the World Bank and International Monetary Fund. Government investments in the capital of international and supranational organisations apart from the International Monetary Fund are classified as other equity (F.519), unless there is no possibility of repayment in which case they are classified as current international cooperation.

Development assistance

THE PUBLIC SECTOR

|

Non-financial corporations |

Financial corporations |

General government |

NPISHs |

Households |

|---|---|---|---|---|

|

Public |

Public |

Public |

Private |

Private |

|

Private |

Private |

N.A. |

|

General government |

Public corporations |

|||||

|---|---|---|---|---|---|---|

|

Central government |

State government |

Local government |

Social security |

Public non-financial corporations |

Public financial corporations |

|

|

Central bank |

Other public financial corporations |

|||||

Public sector control

- rights to appoint, veto or remove a majority of officers, board of directors etc. The rights to appoint, remove, approve or veto a majority of the governing board of an entity are sufficient to determine control. Such rights may be directly held by one public sector unit, or indirectly by public sector units in aggregate. If the first set of appointments are controlled by the public sector but subsequent replacements are not subject to these controls, then the entity remains in the public sector until the time when the majority of the directors are not controlled appointments;

- rights to appoint, veto or remove key personnel. If the control of general policy is effectively determined by influential members of the board, such as the chief executive, chairperson and finance director, then the powers to appoint, veto or remove those personnel are given greater prominence;

- rights to appoint, veto or remove a majority of appointments for key committees of the entity. If key factors of the general policy, such as remuneration of senior staff, pay and business strategy, are delegated to subcommittees, then the rights to appoint, remove or veto of directors on these subcommittees is a determinant of control;

- ownership of the majority of the voting interest. This will normally determine control when decisions are made on a one-share, one-vote basis. The shares may be held directly or indirectly, with shares owned by all public sector units aggregated. If decisions are not made on a one-share, one-vote basis the situation should be analysed to see if the public sector has a majority vote;

- rights under special shares and options. These golden or special shares were once common in privatised corporations and also feature in some special purpose entities. In some cases they give public sector entities some residual rights to protect interests; such rights may be permanent or time-limited. The existence of such shares is not by itself an indicator of control, but needs to be carefully analysed, in particular the circumstances where the powers may be invoked. If the powers influence the current general policy of the entity they will be important to the classification decisions. In other cases they will be reserve powers that may confer rights to control general policy in times of emergency etc, these are judged as irrelevant if they do not influence existing policy, although in the event that they are utilised they will usually trigger immediate reclassification. The existence of a share purchase option to public sector entities in certain circumstances is a similar situation, and a judgement is necessary on whether the powers to implement the option influence the general policy of the entity;

- rights to control via contractual agreements. If all the sales of an entity are to a single public sector entity, or a collection of public sector entities, there is scope for dominant influence that can be judged as control. The presence of other customers, or the potential to have other customers, is an indicator that the entity is not controlled by public sector units. If the entity is restricted from dealing with non-public sector customers due to public sector influence, then this is an indicator of public sector control;

- rights to control from agreements/permission to borrow. Lenders often impose controls as conditions of making loans. If the public sector imposes controls through lending, or to protect its risk exposure from a guarantee, which are tougher than a private sector entity would typically face from a bank, this is an indicator of control. If an entity requires permission from the public sector to borrow, then this is an indicator of control;

- control via excessive regulation. When regulation is so tight that it effectively dictates the general policy of the business, it is a form of control. Public authorities can in some cases have powerful regulatory involvement, particularly in areas such as monopolies and privatised utilities where there is a public service element. It is possible for regulatory involvement to exist in important areas, such as price setting, without an entity ceding control of general policy. Choosing to enter into or operate in a highly regulated environment is similarly an indicator the entity is not subject to control;

- others. Control may also be obtained from statutory powers or rights contained in an entity's constitution, for example to limit the activities, objectives and operating aspects, approve budgets or prevent the entity changing its constitution, dissolving itself, approving dividends, or terminating its relationship with the public sector. An entity that is fully, or close to fully, financed by the public sector is considered to be controlled if the controls on that funding stream are restrictive enough to dictate the general policy in that area.

Central banks

Public quasi-corporations

Special purpose entities and non-residents

Joint ventures