CHAPTER 2

UNITS AND GROUPINGS OF UNITS

- to analyse flows and positions, it is essential to select units which make it possible to study behavioural relationships among economic agents;

- to analyse the process of production, it is essential to select units that bring out relationships of a technico-economic nature, or that reflect local activities;

- to allow regional analyses, units that reflect local kinds of activity are needed.

THE LIMITS OF THE NATIONAL ECONOMY

- the area (geographic territory) under the effective administration and economic control of a single government;

- any free zones, including bonded warehouses and factories under customs control;

- the national air-space, territorial waters and the continental shelf lying in international waters, over which the country enjoys exclusive rights;

- territorial enclaves, these being geographic territories situated in the rest of the world and used, under international treaties or agreements between states, by general government agencies of the country (such as embassies, consulates, military bases, scientific bases, etc.);

- deposits of oil, natural gas, etc. in international waters outside the continental shelf of the country, worked by units resident in the territory as defined in points (a) to (d).

- general government agencies of other countries;

- institutions and bodies of the European Union; and

- international organisations under international treaties between states.

- units that are engaged in production, finance, insurance or redistribution, in respect of all their transactions except those relating to ownership of land and buildings;

- units which are principally engaged in consumption, in respect of all their transactions except those relating to ownership of land and buildings;

- all units in their capacity as owners of land and buildings with the exception of owners of extraterritorial enclaves which are part of the economic territory of other countries or are independent states.

- activity is conducted exclusively on the economic territory of the country: units which carry out such activity are resident units of the country;

- activity is conducted for a year or more on the economic territories of several countries: only that part of the unit that has a centre of predominant economic interest in the economic territory of the country is deemed to be a resident unit of that country.

- border workers, defined as people who cross the frontier daily to work in a neighbouring country;

- seasonal workers, defined as people who leave the country for several months according to season, but less than a year, to work in another country;

- tourists, patients, students, visiting officials, businessmen, salesmen, artists and crew members who travel abroad;

- locally recruited staff working in the extraterritorial enclaves of foreign governments;

- the staff of the institutions of the European Union and of civilian or military international organisations which have their headquarters in extraterritorial enclaves;

- the official, civilian or military representatives of the government of the country (including their households) established in territorial enclaves.

THE INSTITUTIONAL UNITS

- entitled to own goods and assets in its own right; it will be able to exchange the ownership of goods and assets in transactions with other institutional units;

- able to take economic decisions and engage in economic activities for which it is responsible and accountable at law;

- able to incur liabilities on its own behalf, to take on other obligations or further commitments and to enter into contracts; and

- able to draw up a complete set of accounts, comprised of accounting records covering all its transactions carried out during the accounting period, as well as a balance sheet of assets and liabilities.

- households are deemed to enjoy autonomy of decision in respect of their principal function and are, therefore, institutional units nonetheless, even though they do not keep a complete set of accounts;

- entities which do not keep a complete set of accounts, and are not able to compile a complete set of accounts if required to do so, are not institutional units;

- entities which, while keeping a complete set of accounts, have no autonomy of decision, are part of the units which control them;

- entities do not need to publish accounts to be an institutional unit;

- entities forming part of a group of units engaged in production and keeping a complete set of accounts are deemed to be institutional units even if they have partially surrendered their autonomy of decision to the central body (the head office) responsible for the general direction of the group; the head office itself is deemed to be an institutional unit distinct from the units which it controls;

- quasi-corporations are entities which keep a complete set of accounts and have no legal status. They have an economic and financial behaviour that is different from that of their owners and similar to that of corporations. They are deemed to have autonomy of decision and are considered as distinct institutional units.

Head offices and holding companies

- A head office is a unit that exercises managerial control over its subsidiaries. Head offices are allocated to the dominant non-financial corporations sector of their subsidiaries, unless all or most of their subsidiaries are financial corporations, in which case they are treated as financial auxiliaries (S.126) in the financial corporations sector.Where there is a mixture of non-financial and financial subsidiaries, then the predominant share-by-value-added determines the sector classification. Head offices are described under international standard industrial classification of all economic activities revision (ISIC Rev. 4), Section M, class 7010 (NACE Rev. 2, M 70.10) as follows: This class includes the overseeing and managing of other units of the company or enterprise; undertaking strategic or organisational planning and decision-making role of the company or enterprise; exercising operational control and managing the day-to-day operation of their related units.

- A holding company that holds the assets of subsidiary corporations but does not undertake any management activities is a captive financial institution (S.127) and classified as a financial corporation. Holding companies are described under ISIC Rev.4, section K, class 6420 (NACE Rev. 2, K 64.20) as follows: This class includes the activities of holding companies, i.e. units that hold the assets (owning controlling-levels of equity) of a group of subsidiary corporations and whose principal activity is owning the group. The holding companies in this class do not provide any other service to the businesses in which the equity is held, i.e. they do not administer or manage other units.

Groups of corporations

Special purpose entities

- they have no employees and no non-financial assets;

- they have little physical presence beyond a 'brass plate' or sign confirming their place of registration;

- they are always related to another corporation, often as a subsidiary;

- they are resident in a different territory from the territory of residence of the related corporations. In the absence of any physical presence an enterprise's residence is determined according to the economic territory under whose laws the enterprise is incorporated or registered;

- they are managed by employees of another corporation which may or may not be a related one. The SPE pays fees for services provided to it and in turn charges its parent or other related corporation a fee to cover those costs. This is the only production the SPE is involved in, although it will often incur liabilities on behalf of its owner and will usually receive investment income and holding gains on the assets it holds.

Captive financial institutions

Artificial subsidiaries

Special purpose units of general government

- those parts of non-resident units which have a centre of predominant economic interest (being, in most cases, units which engage in economic production for a year or more) on the economic territory of the country;

- non-resident units in their capacity as owners of land and/or buildings on the economic territory of the country, but only in respect of transactions affecting such land or buildings.

-

units that have autonomy of decision and a complete set of accounts such as:

- private and public corporations;

- cooperatives or partnerships recognised as independent legal entities;

- public producers which by virtue of special legislation are recognised as independent legal entities;

- non-profit institutions recognised as independent legal entities; and

- agencies of general government;

- units which have a complete set of accounts and which are deemed to have autonomy of decision despite not having separate incorporation from their parent: quasi-corporations;

-

units which do not necessarily keep a complete set of accounts, but which are deemed to have autonomy of decision, namely:

- households;

- notional resident units.

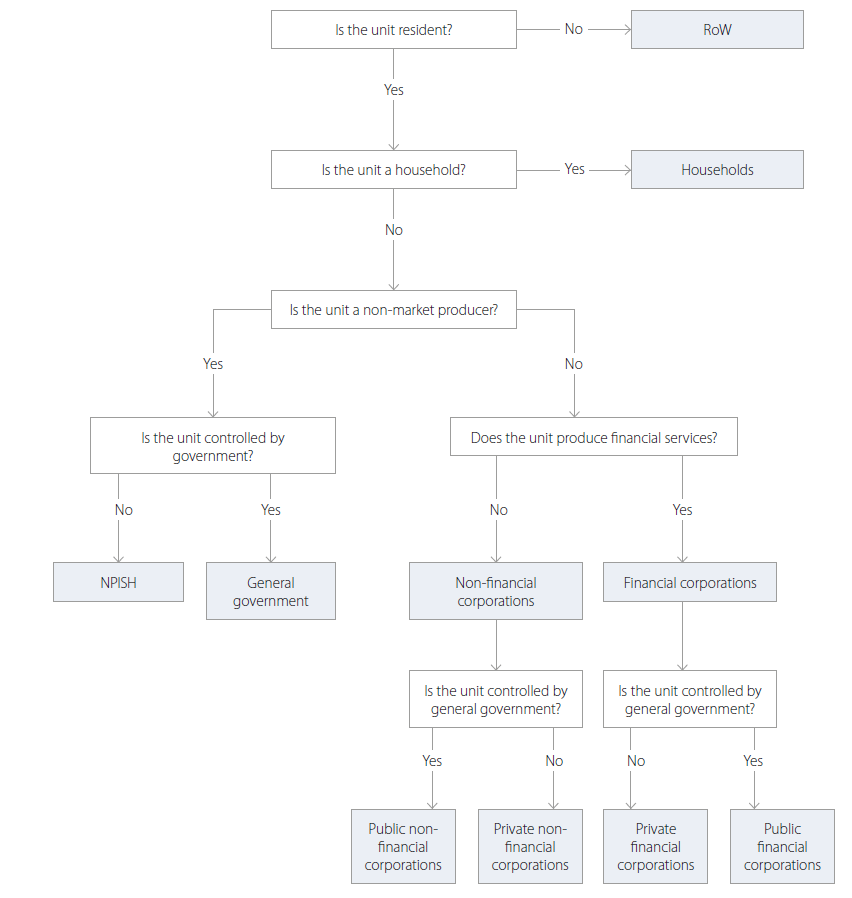

THE INSTITUTIONAL SECTORS

|

Sectors and subsectors |

N.A. |

Public |

National private |

Foreign controlled |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

|

Non-financial corporations |

S.11 |

S.11001 |

S.11002 |

S.11003 |

|||||||

|

Financial corporations |

S.12 |

N.A. | N.A. | N.A. | |||||||

|

Monetary financial institutions (MFIs) |

Central bank |

S.121 |

N.A. | N.A. | N.A. | ||||||

|

Other monetary financial institutions (OMFI) |

Deposit-taking corporations except the central bank |

S.122 |

S.12201 |

S.12202 |

S.12203 |

||||||

|

Money market funds (MMFs) |

S.123 |

S.12301 |

S.12302 |

S.12303 |

|||||||

|

Financial corporations except MFIs and Insurance corporations and pension funds (ICPFs) |

Non-MMF investment funds |

S.124 |

S.12401 |

S.12402 |

S.12403 |

||||||

|

Other financial intermediaries, except insurance corporations and pension funds |

S.125 |

S.12501 |

S.12502 |

S.12503 |

|||||||

|

Financial auxiliaries |

S.126 |

S.12601 |

S.12602 |

S.12603 |

|||||||

|

Captive financial institutions and money lenders |

S.127 |

S.12701 |

S.12702 |

S.12703 |

|||||||

|

ICPFs |

Insurance corporations (IC) |

S.128 |

S.12801 |

S.12802 |

S.12803 |

||||||

|

Pension funds (PF) |

S.129 |

S.12901 |

S.12902 |

S.12903 |

|||||||

|

General government |

S.13 |

N.A. | N.A. | N.A. | |||||||

|

Central government (excluding social security funds) |

S.1311 |

N.A. | N.A. | N.A. | |||||||

|

State government (excluding social security funds) |

S.1312 |

N.A. | N.A. | N.A. | |||||||

|

Local government (excluding social security funds) |

S.1313 |

N.A. | N.A. | N.A. | |||||||

|

Social security funds |

S.1314 |

N.A. | N.A. | N.A. | |||||||

|

Households |

S.14 |

N.A. | N.A. | N.A. | |||||||

|

Employers and own-account workers |

S.141 + S.142 |

N.A. | N.A. | N.A. | |||||||

|

Employees |

S.143 |

N.A. | N.A. | N.A. | |||||||

|

Recipients of property and transfer income |

S.144 |

N.A. | N.A. | N.A. | |||||||

|

Recipients of property income |

S.1441 |

N.A. | N.A. | N.A. | |||||||

|

Recipients of pensions |

S.1442 |

N.A. | N.A. | N.A. | |||||||

|

Recipients of other transfers |

S.1443 |

N.A. | N.A. | N.A. | |||||||

|

Non-profit institutions serving households |

S.15 |

N.A. | N.A. | N.A. | |||||||

|

Rest of the world |

S.2 |

N.A. | N.A. | N.A. | |||||||

|

Member States and institutions and bodies of the European Union |

S.21 |

N.A. | N.A. | N.A. | |||||||

|

Member States of the European Union |

S.211 |

N.A. | N.A. | N.A. | |||||||

|

Institutions and bodies of the European Union |

S.212 |

N.A. | N.A. | N.A. | |||||||

|

Non-member countries and international organisations non-resident in the European Union |

S.22 |

N.A. | N.A. | N.A. | |||||||

- government ownership of the majority of the voting interest;

- government control of the board or governing body;

- government control of the appointment and removal of key personnel;

- government control of key committees in the entity;

- government possession of a golden share;

- special regulations;

- government as a dominant customer;

- borrowing from government.

- the appointment of officers;

- the provisions of enabling instruments;

- contractual agreements;

- the degree of financing;

- the degree of government risk exposure.

|

Type of producer |

Principal activity and function |

Sector |

|---|---|---|

|

Market producer |

Production of market goods and non-financial services |

Non-financial corporations (S.11) |

|

Market producer |

Financial intermediation including insurance Auxiliary financial activities |

Financial corporations (S.12) |

|

Public non-market producer |

Production and supply of non-market output for collective and individual consumption, and carrying out transactions intended to redistribute national income and wealth |

General government (S.13) |

|

Market producer or private producer for own final use |

Consumption Production of market output and output for own final use |

Households (S.14) As consumers As entrepreneurs |

|

Private non-market producer |

Production and supply of non-market output for individual consumption |

Non-profit institutions serving households (S.15) |

Non-financial corporations (S.11)

- private and public corporations which are market producers principally engaged in the production of goods and non-financial services;

- cooperatives and partnerships recognised as independent legal entities which are market producers principally engaged in the production of goods and non-financial services;

- public producers which are recognised as independent legal entities and which are market producers principally engaged in the production of goods and non-financial services;

- non-profit institutions or associations serving non-financial corporations, which are recognised as independent legal entities and which are market producers principally engaged in the production of goods and non-financial services;

- head offices controlling a group of corporations which are market producers, where the preponderant type of activity of the group of corporations as a whole - measured on the basis of value added - is the production of goods and non-financial services;

- SPEs whose principal activity is the provision of goods or non-financial services;

- private and public quasi-corporations which are market producers principally engaged in the production of goods and non-financial services.

- public non-financial corporations (S.11001);

- national private non-financial corporations (S.11002);

- foreign controlled non-financial corporations (S.11003).

Public non-financial corporations (S.11001)

National private non-financial corporations (S.11002)

Foreign controlled non-financial corporations (S.11003)

- all subsidiaries of non-resident corporations;

- all corporations controlled by a non-resident institutional unit that is not itself a corporation; for example, a corporation which is controlled by a foreign government. It includes corporations controlled by a group of non-resident units acting in concert;

- all branches or other unincorporated agencies of non-resident corporations or unincorporated producers which are notional resident units.

Financial corporations (S.12)

- Financial intermediation (financial intermediaries); and/or

- Auxiliary financial activities (financial auxiliaries).

Financial intermediaries

Financial auxiliaries

Financial corporations other than financial intermediaries and financial auxiliaries

Institutional units included in the financial corporations sector

- private or public corporations which are principally engaged in financial intermediation and/or in auxiliary financial activities;

- cooperatives and partnerships recognised as independent legal entities which are principally engaged in financial intermediation and/or in auxiliary financial activities;

- public producers recognised as legal entities, which are principally engaged in financial intermediation and/or in auxiliary financial activities;

- non-profit institutions recognised as legal entities which are principally engaged in financial intermediation and/or in auxiliary financial activities, or which are serving financial corporations;

- head offices when all or most of their subsidiaries are, as financial corporations, principally engaged in financial intermediation and/or financial auxiliary activities. These head offices are classified as financial auxiliaries (S.126);

- holding companies, where the main role is the holding of assets of a group of subsidiary corporations. The make-up of the group can be financial or non-financial - this does not affect the classification of holding companies as captive financial institutions (S.127);

- SPEs whose principal activity is the provision of financial services;

- unincorporated investment funds comprising investment portfolios owned by the group of participants, and whose management is undertaken, in general, by other financial corporations. Such funds are institutional units, separate from the managing financial corporation;

- unincorporated units principally engaged in financial intermediation and subject to regulation and supervision (in most cases classified as deposit-taking corporations except the central bank, insurance corporations or pension funds) are deemed to enjoy autonomy of decision and to have autonomous management independent of their owners; their economic and financial behaviour is similar to that of financial corporations. In this case they are treated as separate institutional units. Examples are branches of non-resident financial corporations.

Subsectors of financial corporations

- central bank (S.121);

- deposit-taking corporations except the central bank (S.122);

- Money market funds (MMF) (S.123);

- non-MMF investment funds (S.124);

- other financial intermediaries, except insurance corporations and pension funds (S.125)

- financial auxiliaries (S.126);

- captive financial institutions and money lenders (S.127);

- insurance corporations (S.128); and

- pension funds (S.129).

Combining subsectors of financial corporations

Subdividing subsectors of financial corporations into public, national private and foreign controlled financial corporations

- public financial corporations;

- national private financial corporations; and

- foreign controlled financial corporations.

|

Sectors and subsectors |

Public |

National private |

Foreign controlled |

|||

|---|---|---|---|---|---|---|

|

Financial corporations |

S.12 |

N.A. | N.A. | N.A. | ||

|

Monetary financial institutions (MFI) |

Central bank |

S.121 |

N.A. | N.A. | N.A. | |

|

Other monetary financial institutions (OMFI) |

Deposit-taking corporations except the central bank |

S.122 |

S.12201 |

S.12202 |

S.12203 |

|

|

MMF |

S.123 |

S.12301 |

S.12302 |

S.12303 |

||

|

Financial corporations except MFI and ICPF |

Non-MMF investment funds |

S.124 |

S.12401 |

S.12402 |

S.12403 |

|

|

Other financial intermediaries, except insurance corporations and pension funds |

S.125 |

S.12501 |

S.12502 |

S.12503 |

||

|

Financial auxiliaries |

S.126 |

S.12601 |

S.12602 |

S.12603 |

||

|

Captive financial institutions and money lenders |

S.127 |

S.12701 |

S.12702 |

S.12703 |

||

|

Insurance corporations and pension funds (ICPFs) |

Insurance corporations (IC) |

S.128 |

S.12801 |

S.12802 |

S.12803 |

|

|

Pension funds (PF) |

S.129 |

S.12901 |

S.12902 |

S.12903 |

||

Central bank (S.121)

- the national central bank, including when it is part of a European system of central banks;

- central monetary agencies of essentially public origin (e.g. agencies managing foreign exchange or issuing currency) which keep a complete set of accounts and enjoy autonomy of decision in relation to central government. When these activities are performed either within central government or within the central bank, no separate institutional units exist.

Deposit-taking corporations except the central bank (S.122)

- commercial banks, 'universal' banks, 'all-purpose' banks;

- savings banks (including trustee savings banks and savings banks and loan associations);

- post office giro institutions, post banks, giro banks;

- rural credit banks, agricultural credit banks;

- cooperative credit banks, credit unions;

- specialised banks (e.g. merchant banks, issuing houses, private banks); and

- electronic money institutions principally engaged in financial intermediation.

- corporations engaged in granting mortgages (including building societies, mortgage banks and mortgage credit institutions);

- municipal credit institutions.

- head offices which oversee and manage other units of a group consisting predominantly of deposit-taking corporations except the central bank, but which are not deposit-taking corporations. Such head offices are classified in subsector S.126;

- non-profit institutions recognised as independent legal entities serving deposit-taking corporations, but not engaged in financial intermediation. They are classified in subsector S.126; and

- electronic money institutions not principally engaged in financial intermediation.

MMF (S.123)

- head offices which oversee and manage a group consisting predominantly of MMFs, but which are not MMFs themselves. They are classified in subsector S.126;

- non-profit institutions recognised as independent legal entities serving MMFs, but not engaged in financial intermediation. They are classified in subsector S.126.

Non-MMF investment funds (S.124)

- open-ended investment funds whose investment fund shares or units are, at the request of the holders, repurchased or redeemed directly or indirectly out of the undertaking's assets;

- closed-ended investment funds with a fixed share capital, where investors entering or leaving the fund must buy or sell existing shares;

- real estate investment funds;

- investment funds investing in other funds ('funds of funds');

- hedge funds covering a range of collective investment schemes, involving high minimum investments, light regulation, and a range of investment strategies.

- pension funds which are part of the pension funds subsector;

- special purpose government funds, called sovereign wealth funds. A special purpose government fund is classified as captive financial institution if it is a financial corporation. The classification of a 'special purpose government fund' either as part of general government sector or as part of the financial corporation sector shall be determined according to the criteria concerning special purpose units of general government set out in paragraph 2.27;

- head offices which oversee and manage a group consisting predominantly of non-MMF investment funds, but which are not investment funds themselves. They are classified in subsector S.126;

- non-profit institutions recognised as independent legal entities serving non-MMF investment funds, but not engaged in financial intermediation. They are classified in subsector S.126.

Other financial intermediaries, except insurance corporations and pension funds (S.125)

|

Other financial intermediaries, except insurance corporations and pension funds |

|

Financial vehicle corporations engaged in securitisation transactions (FVC); |

|

Security and derivative dealers; |

|

Financial corporations engaged in lending; and |

|

Specialised financial corporations |

Financial vehicle corporations engaged in securitisation transactions (FVC)

Security and derivative dealers, financial corporations engaged in lending and specialised financial corporations

- financial leasing;

- hire purchase and the provision of personal or commercial finance; or

- factoring.

- venture and development capital companies;

- export/import financing companies; or

- financial intermediaries which acquire deposits and/or close substitutes for deposits, or incur loans vis-a-vis monetary financial institutions only; these financial intermediaries cover also central counterparty clearing houses (CCPs) carrying out inter-MFI repurchase agreement transactions.

Financial auxiliaries (S.126)

- insurance brokers, salvage and average administrators, insurance and pension consultants, etc.;

- loan brokers, securities brokers, investment advisers, etc.;

- flotation corporations that manage the issue of securities;

- corporations whose principal function is to guarantee, by endorsement, bills and similar instruments;

- corporations which arrange derivative and hedging instruments, such as swaps, options and futures (without issuing them);

- corporations providing infrastructure for financial markets;

- central supervisory authorities of financial intermediaries and financial markets when they are separate institutional units;

- managers of pension funds, mutual funds, etc.;

- corporations providing stock exchange and insurance exchange;

- non-profit institutions recognised as independent legal entities serving financial corporations, but not engaged in financial intermediation (see point (d) of paragraph 2.46);

- payment institutions (facilitating payments between buyer and seller).

Captive financial institutions and money lenders (S.127))

- units as legal entities such as trusts, estates, agencies accounts or 'brass plate' companies;

- holding companies that hold controlling-levels of equity of a group of subsidiary corporations and whose principal activity is owning the group without providing any other service to the businesses in which the equity is held, that is, they do not administer or manage other units;

- SPEs that qualify as institutional units and raise funds in open markets to be used by their parent corporation;

- units which provide financial services exclusively with own funds, or funds provided by a sponsor, to a range of clients and incur the financial risk of the debtor defaulting. Examples are money lenders, corporations engaged in lending to students or for foreign trade from funds received from a sponsor such as a government unit or a non-profit institution, and pawnshops that predominantly engage in lending;

- special purpose government funds, usually called sovereign wealth funds, if classified as financial corporations.

Insurance corporations (S.128)

- life and non-life insurance to individual units or groups of units;

- reinsurance to other insurance corporations.

- fire (e.g. commercial and private property);

- liability (casualty);

- motor (own damage and third party liability);

- marine, aviation and transport (including energy risks);

- accident and health; or

- financial insurance (provision of guarantees or surety bonds).

|

Type of insurance |

Sector/subsector |

||

|---|---|---|---|

|

Direct insurance |

Life insurance Policyholder makes regular or one-off payments to an insurer in return for which the insurer guarantees to provide the policyholder with an agreed sum, or an annuity, at a given date or earlier. |

Insurance corporations |

|

|

Non-life insurance Insurance to cover risks like accidents, sickness, fire, credit, etc. |

Insurance corporations |

||

|

Reinsurance |

Insurance bought by an insurer to protect himself against an unexpectedly large number of claims or exceptionally heavy claims. |

Insurance corporations |

|

|

Social insurance |

Social security The participants are obliged by general government to insure against certain social risks. |

Social security pensions |

Social security funds |

|

Other social security |

|||

|

Employment related social insurance other than social security Employers can make it a condition of employment that employees insure against certain social risks. |

Employment related pensions |

Sector of employer, insurance corporations and pension funds or non-profit institutions serving households |

|

|

Other employment related social insurance |

|||

- institutional units which fulfil each of the two criteria listed in paragraph 2.117. They are classified in sub-sector S.1314;

- head offices which oversee and manage a group consisting predominantly of insurance corporations, but which are not insurance corporations themselves. They are classified in sub-sector S.126;

- non-profit institutions recognised as independent legal entities serving insurance corporations, but not engaged in financial intermediation. They are classified in subsector S.126.

Pension funds (S.129)

- paid after the death of the insured to the widow(er) and children;

- paid after retirement; or

- paid after the insured becomes disabled.

- institutional units which fulfil each of the two criteria listed in paragraph 2.117. They are classified in subsector S.1314;

- head offices which oversee and manage a group consisting predominantly of pension funds, but which are not pension funds themselves. They are classified in subsector S.126;

- non-profit institutions recognised as independent legal entities serving pension funds, but not engaged in financial intermediation. They are classified in subsector S.126.

General government (S.13)

- general government units which exist through a legal process to have judicial authority over other units in the economic territory, and administer and finance a group of activities, principally providing non-market goods and services, intended for the benefit of the community;

- a corporation or quasi-corporation which is a government unit, if its output is mainly non-market and a government unit controls it;

- non-profit institutions recognised as independent legal entities which are non-market producers and which are controlled by general government;

- autonomous pension funds, where there is a legal obligation to contribute, and where general government manages the funds with respect to the settlement and approval of contributions and benefits.

- central government (excluding social security funds) (S.1311);

- state government (excluding social security funds) (S.1312);

- local government (excluding social security funds) (S.1313);

- social security funds (S.1314).

Central government (excluding social security funds) (S.1311)

State government (excluding social security funds) (S.1312)

Local government (excluding social security funds) (S.1313)

Social security funds (S.1314)

- by law or by regulation certain groups of the population are obliged to participate in the scheme or to pay contributions; and

- general government is responsible for the management of the institution in respect of the settlement or approval of the contributions and benefits independently from its role as supervisory body or employer.

Households (S.14)

- the compensation of employees;

- property income;

- transfers from other sectors;

- receipts from the disposal of market products; and

- imputed receipts from the output of products for own final consumption.

- individuals or groups of individuals whose principal function is consumption;

- persons living permanently in institutions who have little or no autonomy of action or decision in economic matters (e.g. members of religious orders living in monasteries, long-term patients in hospitals, prisoners serving long sentences, old persons living permanently in retirement homes). Such people are treated as a single institutional unit: a single household;

- individuals or groups of individuals whose principal function is consumption and that produce goods and non-financial services for exclusively own final use; only two categories of services produced for own final consumption are included within the system: services of owner-occupied dwellings and domestic services produced by paid employees;

- sole proprietorships and partnerships without legal status, other than those treated as quasi-corporations, and which are market producers; and

- non-profit institutions serving households, which do not have independent legal status, or those which do but which are of only minor importance.

- employers (S.141) and own-account workers (S.142);

- employees (S.143);

- recipients of property income (S.1441);

- recipients of pensions (S.1442);

- recipients of other transfers (S.1443).

Employers and own-account workers (S.141 and S.142)

Employees (S.143)

Recipients of property income (S.1441)

Recipients of pensions (S.1442)

Recipients of other transfers (S.1443)

Non-profit institutions serving households (S.15)

- trade unions, professional or learned societies, consumers' associations, political parties, churches or religious societies (including those financed but not controlled by governments), and social, cultural, recreational and sports clubs; and

- charities, relief and aid organisations financed by voluntary transfers in cash or in kind from other institutional units.

Rest of the world (S.2)

- the services of transport (up to the border of the exporting country) provided by resident units in respect of imported goods are shown in the rest of the world accounts with FOB imports, even though they are produced by resident units;

- transactions in foreign assets between residents belonging to different sectors in the domestic economy are shown in the detailed financial accounts for the rest of the world. These transactions do not affect the country's financial position vis-a-vis the rest of the world; they affect the financial relationships of individual sectors with the rest of the world;

- transactions in the country's liabilities between non-residents belonging to different geographical zones are shown in the geographical breakdown of the rest of the world accounts. Although these transactions do not affect the country's overall liability to the rest of the world, they affect its liabilities to different parts of the world.

-

Member States and institutions and bodies of the European Union (S.21):

- Member States of the European Union (S.211);

- Institutions and bodies of the European Union (S.212);

- non-member countries and international organisations non-resident of EU (S.22).

Sector classification of producer units for main standard legal forms of ownership

- those principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and auxiliary financial activities: in sector S.12 (financial corporations).

- those principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and auxiliary financial activities: in sector S.12 (financial corporations).

- those principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and auxiliary financial activities: in sector S.12 (financial corporations).

-

If they are quasi-corporations:

- those principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and financial auxiliary activities: in sector S.12 (financial corporations).

- If they are not quasi-corporations: in sector S.13 (general government), as they remain an integral part of the units which control them.

- those which are market producers and principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and auxiliary financial activities: in sector S.12 (financial corporations);

-

those which are

non-market producers:

- in sector S.13 (general government), if they are public producers controlled by general government;

- in sector S.15 (non-profit institutions serving households), if they are private producers.

-

If they are quasi-corporations:

- those principally engaged in the production of goods and non-financial services: in sector S.11 (non-financial corporations);

- those principally engaged in financial intermediation and financial auxiliary activities: in sector S.12 (financial corporations).

- If they are not quasi-corporations, they are classified in sector S.14 (households).

- in sector S.11 (non-financial corporations), if the preponderant type of activity of the group of corporations which are market producers as a whole is the production of goods and non-financial services (see point (e) of paragraph 2.46);

- in sector S.12 (financial corporations), if the preponderant type of activity of the group of corporations as a whole is financial intermediation (see point (e) of paragraph 2.65).

|

Type of producer Standard legal description |

Market producers (goods and non -financial services) |

Market producers (financial intermediation) |

Non-market producers |

||

|---|---|---|---|---|---|

|

Public producers |

Private producers |

||||

|

Private and public corporations |

S.11 non-financial corporations |

S.12 financial corporations |

|

|

|

|

Cooperatives and partnerships recognised as independent legal entities |

S.11 non-financial corporations |

S.12 financial corporations |

|

|

|

|

Public producers which by virtue of special legislation are recognised as independent legal entities |

S.11 non-financial corporations |

S.12 financial corporations |

|

|

|

|

Public producers not recognised as independent legal entities |

Those with the characteristics of quasi-corporations |

S.11 non-financial corporations |

S.12 financial corporations |

|

|

|

The rest |

|

|

S.13 general government |

|

|

|

Non-profit institutions recognised as independent legal entities |

S.11 non-financial corporations |

S.12 financial corporations |

S.13 general government |

S.15 non-profit institutions serving households |

|

|

Partnerships not recognised as independent legal entities Sole proprietorships |

Those with the characteristics of quasi-corporations |

S.11 non-financial corporations |

S.12 financial corporations |

|

|

|

The rest |

S.14 households |

S.14 households |

|

|

|

|

Head offices whose preponderant type of activity of the group of corporations controlled by them is the production of: |

goods and non-financial services |

S.11 non-financial corporations |

|

|

|

|

financial services |

|

S.12 financial corporations |

|

|

|

LOCAL KIND-OF-ACTIVITY UNITS AND INDUSTRIES

The local kind-of-activity unit

Industries

- industries producing market goods and services (market industries) and goods and services for own final use. Services for own final use are housing services produced by owner-occupiers, and domestic services produced by employing paid staff;

- industries producing non-market goods and services of general government: non-market industries of general government;

- industries producing non-market goods and services of non-profit institutions serving households: non-market industries of non-profit institutions serving households.

Classification of industries

UNITS OF HOMOGENEOUS PRODUCTION AND HOMOGENEOUS BRANCHES

The unit of homogeneous production

The homogeneous branch