CHAPTER 19

EUROPEAN ACCOUNTS

INTRODUCTION

19.01

The process of European integration made it necessary to compile a full set of accounts that reflect the European economy as a whole

and enable better analysis and policy making at the European level. European accounts cover the same set of accounts, and are based on the same concepts,

as the national accounts of the Member States.

19.02

This chapter describes the distinguishing features of European accounts, that is, the accounts of the European Union and of the euro

area. European accounts require particular attention to be given to the definition of resident units,

rest of the world

accounts and the

netting

of intra-European economic transactions (flows) and financial balance sheets (stocks).

FROM NATIONAL TO EUROPEAN ACCOUNTS

19.05

European accounts are conceptually not equal to the sum of the national accounts of the Member States after conversion to a common

currency. The accounts of resident European institutions need to be added. The scope of the concept of residence changes when one steps from the national accounts

of Member States to European accounts. The ways in which the reinvested earnings of foreign direct investment enterprises or special purpose entities are

treated are good examples in this context. In the national accounts of the Member States, a foreign direct investment enterprise may have investors which

are residents of another Member State of the European Union/the euro area. The corresponding reinvested earnings are not recorded as such in European

accounts. Besides, special purpose entities may need to be reclassified in the same institutional sector as their parent company when the latter is resident

of another Member State. Finally, cross-border economic flows and financial stocks between European countries need to be reclassified. These differences are

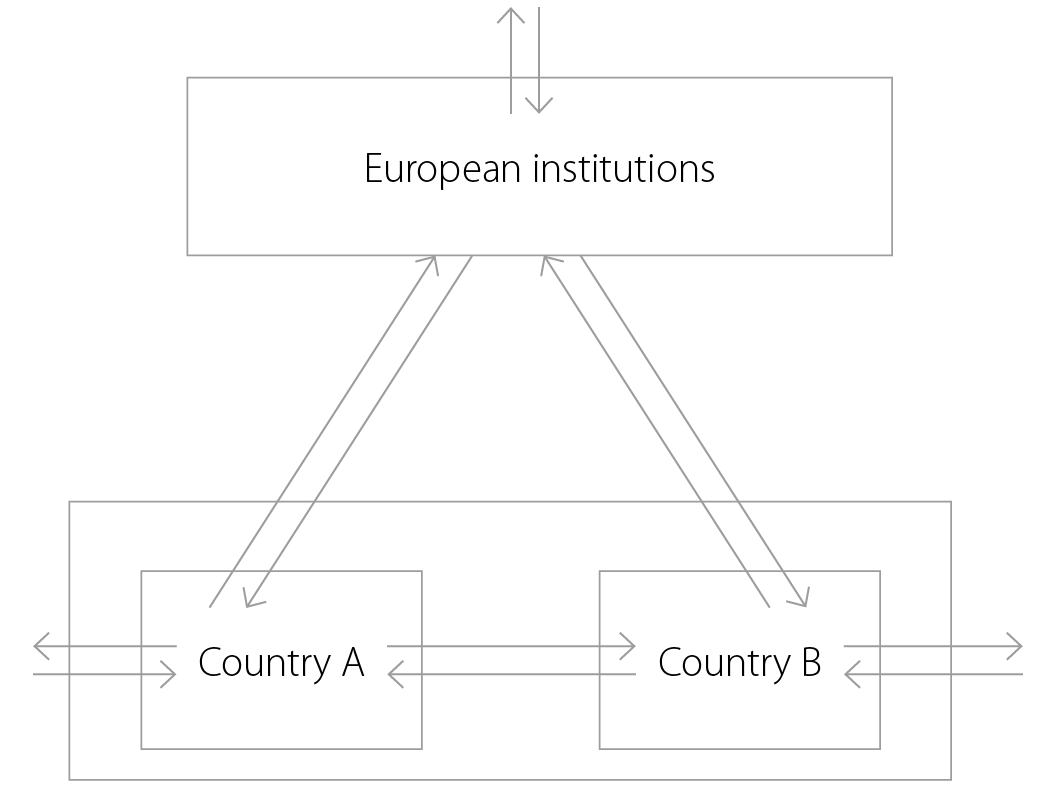

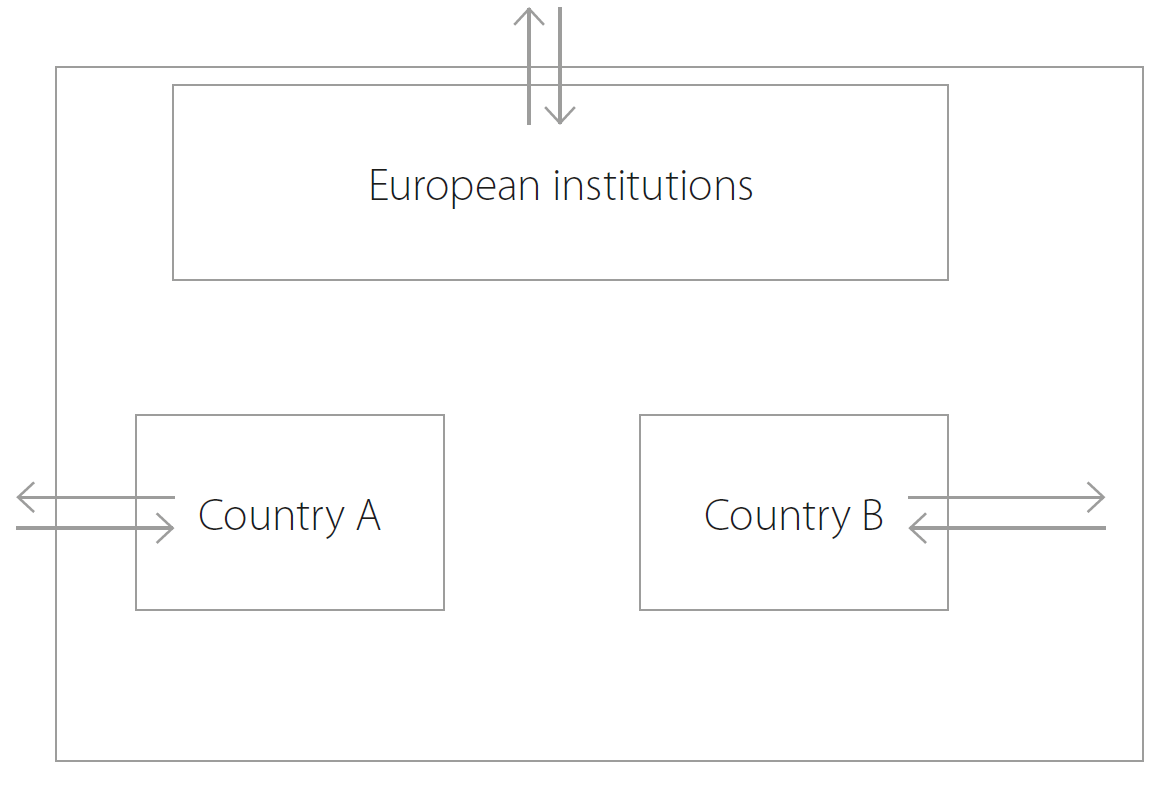

presented in diagrams 19.1 and 19.2 assuming, for the sake of simplicity, a European area composed of only two Member States: A and B. Flows and stocks

involving residents and non-residents are schematically displayed with arrows.

When the national accounts of countries A and B are aggregated, the aggregated

rest of the world

accounts record intra-flows between countries A and B, and with other countries and European institutions.

The European Union/euro area is considered as a single entity: the accounts of European institutions/the European Central Bank are

included and only transactions of resident units with third countries are recorded in the

rest of the world

accounts.

The European Union/euro area is considered as a single entity: the accounts of European institutions/the European Central Bank are

included and only transactions of resident units with third countries are recorded in the

rest of the world

accounts.

Conversion of data in different currencies

19.06

In European accounts, the economic flows and the stocks of

assets

and liabilities must be expressed in one single monetary standard. For this purpose, data recorded in the different national currencies are converted into

euro by either:

- using market exchange rates (or an average thereof) prevailing during the time period for which the accounts are compiled; or

- using fixed exchange rates, over the whole time period. The fixed rate can be the one prevailing at the end of the period, in the beginning, or as an average of exchange rates over the whole time period. The exchange rate used affects the (fixed) weight of a given Member State in European aggregates; or

- calculating an index between consecutive periods as the weighted average of the growth indices of the data of each Member State expressed in national currency. Weights are constructed as the exchange-rate converted share of each Member State in the first period of comparison. After a reference period is chosen as a benchmark, the chain-linked index can be applied to this benchmark to generate levels for other periods of observation.

With method (b), the weights of Member States are not updated, which preserves the movements of European aggregates from exchange rate

fluctuations. However, European aggregates' levels may be influenced by the choice of the (fixed) exchange rates that reflect the parities of Member

States' currencies at a given moment in time.

Method (c) preserves the movements of European aggregates from exchange rate fluctuations whereas European aggregates' levels broadly

reflect the parities in force for each time period. This is at the expense of additivity and other accounting constraints. If these are required, they

must be restored as a last step.

19.07

European accounts can also be calculated by converting data recorded in the different national currencies into purchasing power

standards (PPS). Method (a), (b) or (c) set out in paragraph 19.06 can be used for this purpose replacing exchange rates by corresponding purchasing power

parities (PPPs).

European institutions

19.08 In the ESA, European institutions comprise the following entities:

- European non-financial institutions: the European Parliament, the European Council, the Council, the European Commission, the Court of Justice of the European Union and the European Court of Auditors;

- European non-financial bodies, including the entities covered by the general budget of the European Union (e.g. the Social and Economic Committee, the Committee of the Regions, European agencies etc.) and the European Development Fund; and

- European financial institutions and bodies including notably: the European Central Bank, the European Investment Bank and the European Investment Fund.

19.09

European non-financial institutions and bodies covered by the general budget of the European Union form one

institutional unit

which principally provides non-market government services for the benefit of the European Union. It is thus classified in the 'European institutions and

bodies' subsector (S.1315)

[1] of the 'general government' sector (S.13).

19.10

As long as its budget is not adopted as a part of the general budget of the European Union, the European Development Fund forms a

separate

institutional unit

classified in the 'European institutions and bodies' subsector (S.1315) of the 'general government' sector (S.13).

19.11

The European Central Bank is an institutional unit classified in the

'central bank' subsector

(S.121) of the 'financial corporations' sector (S.12).

19.12

The European Investment Bank and the European Investment Fund are separate

institutional units

classified in the

'other financial intermediaries, except insurance corporations and pension funds' subsector (S.125) of the 'financial corporations' sector (S.12).

The rest of the world account

19.15

In European accounts, the rest of the world accounts record the economic flows and the financial stocks of

assets

and liabilities between the resident units of the European Union/the euro area and non-resident units. Hence, European rest of the world accounts exclude

transactions taking place within the European Union/the euro area. The flows taking place within the EU/euro area are called 'intra-flows' and the

financial positions between residents of the EU/euro area are called 'intra-stocks'.

19.16 Imports and exports of goods include quasi-transit trade, that is:

- goods imported from third countries into a Member State of the European Union/euro area by an entity which is not considered to be an institutional unit and then dispatched to another Member State of the European Union/euro area; and

- goods arriving from a Member State of the European Union/euro area which are then exported to third countries by an entity which is not considered to be an institutional unit.

For goods in quasi-transit to be exported, transportation and distribution costs within the European Union/the euro area shall be

considered as

output

of transportation services if the carrier is resident in the European Union/the euro area and as imports of transportation services if it is not.

19.17

In European accounts, merchanting

[]

includes only the purchase of goods by a resident of the European Union/the euro area from a non-resident with the subsequent resale of the same goods to

a non-resident without the goods being present in the European Union/the euro area. It is recorded first as a negative export of goods and then as a

positive export of goods, with any timing differences between the purchase and sale being recorded as changes in inventories (see paragraphs 18.41 and

18.60).

See BPM6 paragraph 10.41-10.49

Balance of Payments and International Investment Position Manual

19.18

A foreign direct investment

[]

enterprise is a resident of the European Union/the euro area where an investor which is not a resident owns 10 per cent or more of the ordinary shares or

voting power (for an incorporated enterprise) or the equivalent (for an unincorporated enterprise).

See BPM6 paragraph 6.8

Balance of Payments and International Investment Position Manual

Balancing of transactions

19.19

One method to compile the European rest of the world accounts consists of withdrawing intra-European flows, on both the resources and

uses sides, from the rest of the world accounts of the Member States. Although these mirror flows should balance in theory, they generally do not do so in

practice because of the asymmetrical recording of the same transaction in the national accounts of the counterparties.

19.20

Asymmetries create a mismatch, in European accounts, between the total economy and

rest of the world

accounts. The compilation of European accounts therefore requires reconciliation of the accounts. This is achieved by reconciliation methods such as

minimum least squares or proportional allocation. In the case of goods, intra-Union trade statistics may be used to allocate asymmetries by expenditure

category.

Price and volume measures

19.22

European non-financial accounts at the prices of the previous year can be compiled, for transactions in goods and services, using a

similar methodology as for European accounts at current prices. First, the accounts of the Member States and European institutions/the European Central

Bank, compiled at the prices of the previous year, are aggregated. Second, cross-border transactions among Member States, valued at the prices of the

previous year, are eliminated from the rest of the world accounts. Third, the resulting discrepancies between resources and uses are eliminated using the

method chosen to balance European transactions at current prices.

19.23

European accounts at the prices of the previous year allow the calculation of volume indices between the current time period and the

previous year. After a reference period is chosen as a benchmark, volume indices can be chain linked and then applied to the European accounts at current

prices of the benchmark year. This generates European accounts in volume for any period of observation. The series obtained in this way are not additive.

If additivity and other accounting constraints are required for measures in volume terms for specific purposes, these must be restored as a last step in

order to obtain additive adjusted series.

Balance sheets

19.24 In European accounts, financial balance sheets can be compiled using a similar treatment as for transactions:

- the financial balance sheets of the Member States are complemented by stocks of assets held and liabilities assumed by European institutions which are resident of the European Union/euro area;

- stocks of financial ssets of a resident of the European Union/euro area held by another resident (intra-stocks) are withdrawn from the national rest of the world accounts; and

- imbalances created by the mismatch between intra-stocks of financial assets and the corresponding liabilities are allocated to the different sectors through balancing.

'From whom-to-whom' matrices

19.26

'From whom-to-whom' matrices detail the economic transactions (respectively holdings of

financial assets) between institutional sectors. In the national accounts of the Member States, these matrices map in detail the transactions/financial assets

between sectors of origin/creditor and destination/debtor, as well as between domestic sectors and the

rest of the world.

19.27

In European accounts, 'from whom-to-whom' matrices can be compiled by aggregation of the national matrices and reclassification of

intra-European flows and stocks as resident flows and stocks. For this purpose, a distinction is then to be made in these national matrices between

transactions, and the holding of financial assets, vis-a-vis the resident units of the European Union/the euro area and the non-residents in the

rest of the world

account. Moreover, flows and stocks vis-a-vis the residents units of the European Union/the euro area need to be further distinguished by counterpart

sectors.

ANNEX 19.1

The accounts of european institutions

Resources

19.30

Customs and agricultural duties are levied at the external frontiers of the European Union under the common customs tariff. They are

classified as 'taxes and duties on imports excluding VAT' (D.212) and include collection costs.

19.31

Production charges are levied on the sugar, isoglucose and inulin syrup quotas held by the producers. They are classified as

'taxes on products, except VAT and import taxes'

(D.214) and include collection costs.

19.32

A fixed share of the amounts collected under points (a) and (b) of paragraph 19.A1.01 is retained by Member States as collection

costs. This share was 25 % in 2009. In the accounts of European institutions, these collection costs are recorded, on the uses side, as '

intermediate consumption' (P.2) of the 'European institutions and bodies' subsector (S.1315). On the resources side, they are recorded as 'imports of

services' (P.72) in the rest of the world accounts (S.211).

19.33

The value added tax resource is calculated by applying a fixed percentage rate, known as the VAT rate of call, to the harmonised VAT

assessment base of each Member State. The VAT base is capped in relation to gross national income. The capping of the VAT base means that, if the VAT base

of a Member State exceeds a given percentage of this Member State's GNI assessment base, then the VAT rate of call is not applied to the VAT base but

to the latter percentage of the GNI assessment base. The

value added

tax resource includes payments for the current year as well as balances from previous years, corresponding to revisions of past VAT bases, when they are

due to be paid. The value added tax resource is classified as 'VAT- and GNI-based EU own resources' (D.76).

19.34

The gross national income resource is a residual contribution to the budget of the European institutions which is assessed on the

levels of gross national income of each Member State. It is classified as 'VAT- and GNI-based EU own resources' (D.76) and includes reimbursements as well as the balancing payments for previous years. The correction of budgetary imbalances paid by the other

Member States to the countries concerned is also recorded under D.76, as resources and uses of the rest of the world (S.211).

19.35

The contributions of Member States to the European Development Fund are classified as

'current international cooperation' (D.74).

19.36

The Member States subscriptions to the paid-in capital of the European Investment Bank, the European Investment Fund and the European

Central Bank are recorded in the financial accounts as

'other equity' (F.519). They are recorded as changes in assets of the rest of the world (S.211) and changes in liabilities of the

'other financial intermediaries, except insurance corporations and pension funds' (S.125)/'central bank' (S.121) subsectors.

19.37

Interests payable on loans granted by the European Investment Bank, after deduction of financial intermediation services indirectly

measured (FISIM), are classified as 'interest' (D.41). In the accounts of European institutions, they are recorded as uses of the

rest of the world

(S.2) and resources of the

'other financial intermediaries, except insurance corporations and pension funds' (S.125).

19.38

Interests payable on loans granted by the European Central Bank are classified as 'interest' (D.41). In the accounts of European institutions, they are recorded as uses of the rest of the world (S.2111) and resources of the 'central bank' (S.121) subsector.

Uses

19.39 Payments made by European non-financial institutions and bodies consist of the following:

- transactions related to their activities as non-market producers, mainly: ' intermediate consumption' (P.2), ' gross fixed capital formation' (P.51) and 'compensation of employees' (D.1);

- distributive transactions related to the transfers from European institutions to Member States. They take mainly the form of 'subsidies on products' (D.31), 'other subsidies on production' (D.39), 'current international cooperation' (D.74), "other miscellaneous current transfers' (D.759), 'investment grants' (D.92) and 'other capital transfers' (D.99); and

- payments of the European Development Fund to third countries which are classified as 'current international cooperation' (D.74).

19.41

Payments made by European non-financial institutions and bodies are generally recorded on the basis of the expenditure statements

provided by the Member States. Advance and ex-post payments are recorded in the financial accounts of the European institutions as 'other accounts receivable/payable, excluding trade credits and advances' (F.89).

19.42 Payments made by European financial institutions and bodies consist of the following:

- transactions related to their activities as market producers of financial services, mainly: 'intermediate consumption' (P.2), ' gross fixed capital formation' (P.51) and 'compensation of employees' (D.1);

- interest payments (D.41).

19.43

The accounts of European institutions record the payments made by European financial institutions and bodies as uses of the

'other financial intermediaries, except insurance corporations and pension funds' (S.125) subsector and resources of the rest of the world (S.211 or S.22).

Consolidation

19.44

In European accounts, flows between Member States and European institutions are normally not consolidated, among resources and uses,

within the 'general government' sector (S.13). However, in the case of

'current international cooperation'

(D.74), the payments of Member States to the European institutions to finance, e.g. the European Development Fund, are consolidated and recorded, in

European accounts, as uses of national 'central government (excluding social security)' (S.1311) and resources of the rest of the world (S.22).

List of abbreviations and acronyms

ABO

accrued benefit obligation

ABS

asset-backed security

BPM6

Balance of payments manual, sixth edition

CCP

central counterparty clearing house

CDS

credit default swap

CIF

cost, insurance and freight

COFOG

Classification of the Functions of Government

COICOP

Classification of Individual Consumption by Purpose

COPNI

Classification of the Purposes of Non-Profit Institutions Serving Households

COPP

Classification of Outlays of Producers by Purpose

CPA

Classification of Products by Activity

EAA

economic accounts for agriculture

EAFRD

European Agricultural Fund for Rural Development

EAGF

European Agricultural Guarantee Fund

EC

European Commission

ECB

European Central Bank

EMU

economic and monetary union

ESA

European System of Accounts

ESO

employee stock option

ESSPROS

European System of Integrated Social Protection Statistics

EU

European Union

EURIBOR

European interbank offered rate

EUROSTAT

the statistical office of the European Union

FDI

foreign direct investment

FISIM

financial intermediation services indirectly measured

FOB

free on board

FRA

forward rate agreement

FVC

financial vehicle corporation

GAB

general arrangements to borrow

GDP

gross domestic product

GFS

government finance statistics

GNI

gross national income

GVA

gross value added

IAS

international accounting standards

IASB

International Accounting Standards Board

IASC

International Accounting Standards Committee

IC

insurance corporations

ICLS

International Conference of Labour Statisticians

ICPF

insurance corporations and pension funds

ICT

information, communications and telecommunications

IFRS

International Financial Reporting Standards

IIP

international investment position

ILO

International Labour Organisation

IMF

International Monetary Fund

IMTS

international merchandise trade statistics

IMTS

international merchandise trade statistics

INTRASTAT

statistical collection system

I-O

input-output

IPO

initial public offering

IPSASB

International Public Sector Accounting Standards Board

ISIC

International Standard Industrial Classification of all Economic Activities

ISIN

international securities identification number

KAU

kind-of-activity unit

KLEMS

capital, labour, energy, materials and services

LIBOR

London interbank offered rate

MFI

monetary financial institution

MMF

money market fund

MSITS

Manual on statistics of international trade in services

N.E.C.

not elsewhere classified

NAB

new arrangements to borrow

NACE

general industrial classification of economic activities within the European Union

NDP

net domestic product

NOS

net operating surplus

NPI

non-profit institution

NPISH

non-profit institution serving households

NUTS

nomenclature of territorial units for statistics

OECD

Organisation for Economic Cooperation and Development

OMFI

other monetary financial institution

OTC

over the counter

PAYE

pay as you earn

PBO

projected benefit obligation

PF

pension funds

PIM

perpetual inventory method

PPP

purchasing power parity

PPP

public-private partnership

PPS

purchasing power standard

PRGF

Poverty Reduction and Growth Facility

R&D

research and development

ROW

rest of the world

SAM

social accounting matrix

SDR

special drawing right

SEEA

System of Environmental-Economic Accounts

SNA

System of National Accounts

SOCX

Social Expenditure Database

SPE

special-purpose entity

SPV

special-purpose vehicle

STRIPS

Separate Trading of Registered Interest and Principal Securities

UCITS

undertakings for collective investment in transferable securities

UN

United Nations

VAT

value added tax