|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State of the Union: President Juncker stresses investment for jobs and growth and completing EMU

In his State of the Union speech delivered before the European Parliament on 9 September, Jean-Claude Juncker, President of the European Commission, focused on the challenge of the refugee crisis but also emphasised the importance of investing in jobs and growth, notably in the Single Market, and completing the Economic and Monetary Union. The President argued that the EU needs to “recreate a process of convergence, both between Member States and within societies, with productivity, job creation and social fairness at its core.” President Juncker noted that the EUR 315 billion Investment Plan for Europe had been brought to life with a new European Fund for Strategic Investments, and that the Single Market was being upgraded. He added that in the “Five Presidents’ Report” the five presidents of the leading EU institutions have agreed upon a roadmap for stabilising and consolidating the euro area by early 2017 and then achieving more fundamental reform. President Juncker affirmed that the Commission will swiftly present proposals covering a wide range of areas, but at the same time emphasised that the single currency needs constant political assessment – rather than rules and statistics alone.

State of the Union Address 2015 (Full speech)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Together with you and the Member States, we brought to life the €315 billion Investment Plan for Europe, with a new European Fund for Strategic Investments (EFSI). Less than a year after I announced this plan, we are now at a point where some of the first projects are just taking off.

|

|

Jean-Claude Juncker, President of the European Commission

|

|

|

|

|

|

|

|

|

|

EFSI poised for full launch this autumn; two EFSI deals concluded in Belgium; Investment Plan Road Show continues with visit to Malta

After initial pre-launch successes such as the conclusion of first transactions in Luxembourg and the UK over the summer, the European Fund for Strategic Investments (EFSI) is now poised for full launch in autumn 2015. The Commission announced a package of measures on 22 July that represent the final building blocks needed to kick-start investment in the real economy and keep to the ambitious implementation timetable set by Commission President Juncker. Final arrangements were also made to launch the European Investment Advisory Hub (EIAH). The EIAH will support the development and preparation of investment projects in the EU; project promoters/investors can already submit their requests. Meanwhile, on 11 September two more EFSI transactions were concluded that could support 600 SMEs in the Walloon region of Belgium by providing EUR 145 million in bank financing. Vice-President Jyrki Katainen and Commissioner Karmenu Vella, responsible for the Environment, Maritime Affairs and Fisheries, continued the road show with a visit to Valletta, Malta to promote the Investment Plan for Europe. They met with government leaders, businesses and members of Parliament, and visited a partially EU-funded technology company. Katainen will continue the road show with visits to Vilnius, Lithuania on 18 September and Slovenia on 8 October.

|

|

|

|

|

|

|

|

|

|

|

|

|

ESM stability support programme for Greece: implementation is the way forward

Following the successful negotiation and adoption in August of a three-year ESM programme for Greece, attention now turns to its implementation. The adoption of a medium-term fiscal strategy, changes in tax policy and tax administration, a comprehensive pension reform to ensure sustainability, improved performance in public administration, and major structural changes in product markets and network industries are priorities. On 19 August, the Commission signed a Memorandum of Understanding (MoU) with Greece following approval by the European Stability Mechanism’s (ESM) Board of Governors for further stability support accompanied by a third economic adjustment programme. This followed the political agreement reached on 14 August and paves the way for mobilising up to EUR 86 billion in financial assistance to Greece over three years (2015-2018). As provided for in Article 13 of the ESM Treaty, the MoU details the reform targets and commitments needed to unlock ESM financing. The disbursement of funds is linked to progress in delivery. A first disbursement of funds under the programme in the amount of EUR 13 billion was made in August, while an additional EUR 10 billion was earmarked for bank recapitalisation and resolution. On 15 July, the Commission presented a Jobs and Growth Plan for Greece of more than EUR 35 billion to help support the Greek economy by helping Greece maximise its use of EU funds until 2020. In his State of the Union address, Commission President Juncker took note of the positive developments, but added: “We are only at the beginning of a new, long journey.”

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finance ministers’ approval paves way for disbursement of EUR 500 million to Cyprus; ministers also agree to benchmark ‘tax wedge’ in the EU

During informal ECOFIN and Eurogroup meetings on 11 and 12 September, European finance ministers reviewed progress and took decisions on several key issues. Referring to the successful conclusion of the seventh review mission of Cyprus’ macroeconomic adjustment programme which took place in July, finance ministers noted that the economic recovery is stronger than expected, fiscal developments continue to exceed expectations, and progress has been made on growth-enhancing reforms. They therefore authorised the launch of relevant national procedures that will pave the way for disbursement of EUR 500 million by the ESM in October. Separately, finance ministers also agreed to benchmark the tax wedge on labour in the EU. Reducing the ‘tax wedge’ – the difference between how much workers are paid and how much they take home after taxes – is a key factor in boosting job creation. Euro area Member States’ tax burden on labour will be benchmarked against the GDP-weighted EU average, and compared with the OECD average. Finally, on the Banking Union, finance ministers noted that all Member States have made progress on implementing reforms before the 1 January 2016 deadline.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G20 Finance Ministers and Central Bank Governors discuss global economy in Ankara

Commissioner Moscovici attended the G20 Finance Ministers and Central Bank Governors meeting in Ankara on 4-5 September 2015. Discussions focused on the global economy; the implementation of G20 growth strategies; investment; the international financial architecture; tax transparency; financial regulation and other issues. On the global economy, Ministers and Governors welcomed the strengthening economic activity in some economies, but acknowledged that global growth falls short of expectations. Against this background, G20 members reiterated their commitment to implement their growth strategies in order to strengthen growth and enhance the resilience of the economy. The meeting was preceded by a joint G20 Labour and Finance Minister meeting, which focused on growth and employment as well as on inequalities.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commission presses Member States as VAT revenue collection fails to show significant improvement across EU

VAT revenue collection has failed to show significant improvement across EU Member States according to the latest figures released by the European Commission on 4 September. Based on VAT collection figures from 2013, the overall difference between the expected VAT revenue and the amount actually collected (the so-called ‘VAT Gap’) did not improve compared with 2012. While 15 Member States including Latvia, Malta and Slovakia saw an improvement in their figures, 11 Member States including Estonia and Poland saw deterioration. The total amount of VAT lost across the EU is estimated at EUR 168 billion, according to the report. This equates to 15.2% of revenue that is lost due to fraud and evasion, tax avoidance, bankruptcies, financial insolvencies and miscalculation in 26 Member States. In addition to detailing the VAT gap, the latest VAT Gap study also gives an indication of the effectiveness of VAT enforcement and compliance measures.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

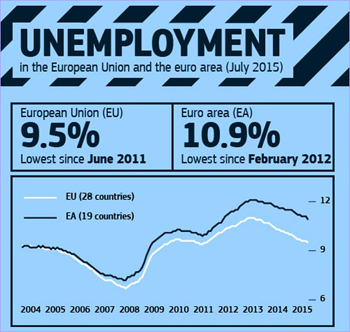

Employment up 0.3% in euro area and 0.2% in EU; Euro area unemployment rate at 10.9%, EU at 9.5%

The number of persons employed increased by 0.3% in the euro area and by 0.2% in the EU in the second quarter of 2015 compared with the previous quarter, according to national accounts estimates published on 15 September by Eurostat, the EU statistical office. In the first quarter of 2015, employment increased by 0.2% in the euro area and 0.3% in the EU28. Compared with the same quarter of the previous year, employment increased by 0.8% in the euro area and by 0.9% in the EU in the second quarter of 2015 (after +0.8% and +1.0% respectively in the first quarter of 2015). These figures are seasonally adjusted. According to data published by Eurostat on 1 September, the euro area seasonally-adjusted unemployment rate was 10.9% in July 2015, down from 11.1% in June 2015, and from 11.6% in July 2014. This is the lowest rate recorded in the euro area since February 2012. The EU unemployment rate was 9.5% in July 2015, down from 9.6% in June 2015, and from 10.2% in July 2014. This is the lowest rate recorded in the EU since June 2011.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

GDP up by 0.4% in both euro area and EU

Seasonally adjusted GDP rose by 0.4% in both the euro area and the EU during the second quarter of 2015, compared with the previous quarter, according to a second estimate published by Eurostat, the EU statistical office. In the first quarter of 2015, GDP grew by 0.5% in both areas. Compared with the same quarter of the previous year, seasonally adjusted GDP rose by 1.5% in the euro area and by 1.9% in the EU in the second quarter of 2015, after growing by +1.2% and +1.7% respectively in the previous quarter. GDP increased in all Member States for which data are available for the second quarter of 2015, except in France where it remained stable. The highest growth compared with the previous quarter was recorded in Latvia (+1.2%), Malta (+1.1%), the Czech Republic, Spain and Sweden (all +1.0%), followed by Greece and Poland (both +0.9%), Slovakia (+0.8%), Estonia, Croatia, Lithuania, Slovenia and the United Kingdom (all +0.7%). The lowest growth rates were registered in the Netherlands, Austria and Romania (all +0.1%).

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Why do some bailed-out countries fare better than others? “Real Economy” episode on Euronews explores debt sustainability

Debt sustainability has become a critical issue for both governments and international investors during the past half-decade, and particularly for EU Member States like Greece and Portugal that have been bailed-out. In this edition of "Real Economy", Euronews explores the nuts and bolts of debt sustainability and finds out how and why some countries score better than others. The programme examines the contrasting fortunes of two EU economies – Latvia and Portugal. In the programme, Sony Kapoor, Director of the international think tank "Re-Define", explains why it is important to understand the distinction between how government books are balanced versus those of a household. Personal or business loans or government borrowing can be sustainable and stimulate the economy, as long as the money can be paid back. If not, debt servicing and confidence may reach untenable levels. “Real Economy” aims to bring the complexities of economic matters in the EU closer to Euronews’ daily audience of 6.5 million viewers. Besides watching it on TV, viewers can also follow it online – live or on demand.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unemployment in the European Union and the euro area

|

|

|

|

|

|

|

|

|

The latest Eurostat data show a decline in unemployment in the European Union and the euro area.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Directorate-General for Economic and Financial Affairs

|

|

|

|